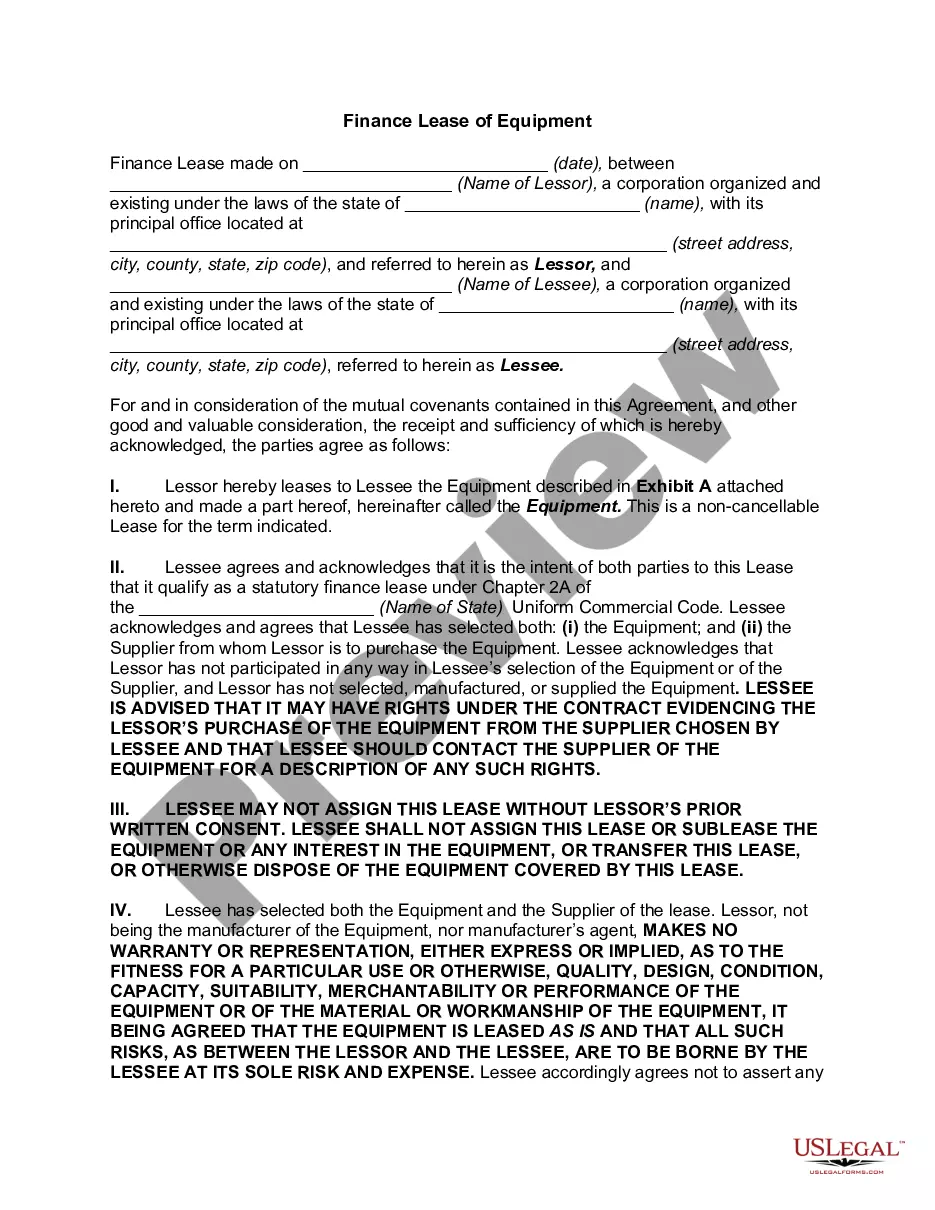

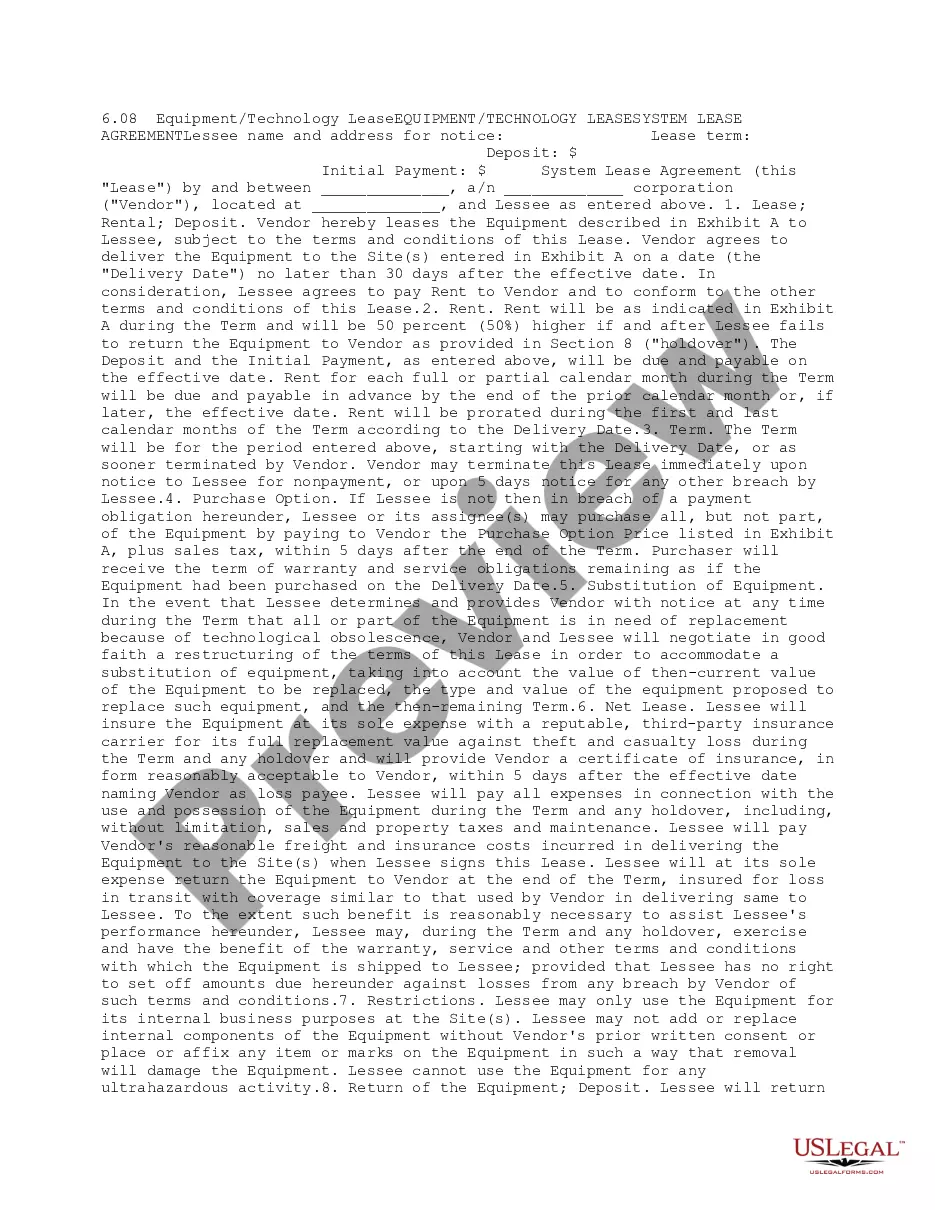

The rate of technology change is increasing, with an emphasis on client/server

technology, faster system development, and shorter life cycles. This has led to spiraling information technology (IT) budgets, driving the need for a re-evaluation of IT management issues. Organizations must find new ways to accommodate technological change. Leasing has recently emerged as a feasible, cost-effective alternative to purchasing equipment, particularly in the desktop and laptop areas.

Pennsylvania Guidelines for Lease vs. Purchase of Information Technology

Instant download

Description

Free preview

How to fill out Guidelines For Lease Vs. Purchase Of Information Technology?

Are you presently in a role where you need documentation for both business or personal reasons on a daily basis.

There are numerous legal document templates accessible online, but finding ones you can depend on is challenging.

US Legal Forms provides thousands of form templates, including the Pennsylvania Guidelines for Lease vs. Purchase of Information Technology, crafted to comply with state and federal regulations.

Once you find the appropriate form, simply click Purchase now.

Select the payment plan you desire, fill in the required information to create your account, and finalize the order using your PayPal or credit card.

- If you are already familiar with the US Legal Forms site and have an account, simply Log In.

- Then, you can download the Pennsylvania Guidelines for Lease vs. Purchase of Information Technology template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Find the form you require and ensure it is for the correct city/region.

- Use the Preview button to examine the form.

- Check the description to confirm that you have selected the right form.

- If the form is not what you need, use the Search section to locate a form that fits your needs.

Form popularity

FAQ

The Pennsylvania Business Entity Registration Form (PA-100) must be completed by Business Entities to register for certain taxes and services administered by the PA Department of Revenue and the Department of Labor & Industry.

Yes. The Sales Tax regulation on computer services is found in the PA Code.

Major items exempt from the tax include food (not ready-to-eat); candy and gum; most clothing; textbooks; computer services; pharmaceutical drugs; sales for resale; and residential heating fuels such as oil, electricity, gas, coal and firewood. The Pennsylvania sales tax rate is 6 percent.

In addition to specific tax account numbers, the department also issues a 10-digit Revenue Identification Number (Revenue ID) to all businesses that have any tax filing obligation with Pennsylvania. The Revenue ID number is referenced on all correspondence issued by the department.

Sales of custom software - delivered on tangible media are exempt from the sales tax in Pennsylvania. Sales of custom software - downloaded are exempt from the sales tax in Pennsylvania.

The Pennsylvania Department of Revenue ruled that cloud computing software is subject to Pennsylvania sales and use tax when used by people in-state (SUT-12-001).

California: SaaS is not a taxable service. However, software or information that is delivered electronically is exempt. The ability to access software from a remote network or location is exempt. Under California sales and use tax law, there must be a transfer of TPP, in order to have a taxable event.

If you're selling goods or services in Pennsylvania, you probably need a sales tax license. Pennsylvania also applies a sales and use tax on digital goods, so even if you're only selling online, you likely need a Pennsylvania sales and use tax license, sometimes also called a seller's permit.

The rental, lease or license to use or consume tangible personal property is subject to tax.

Cloud computing in the form of SaaS is subject to the state's sales and use tax if the user is located in Pennsylvania. The taxability of remote access to software in Pennsylvania depends on the location of the user. If the user is accessing the software from within the state, the transaction is subject to tax.