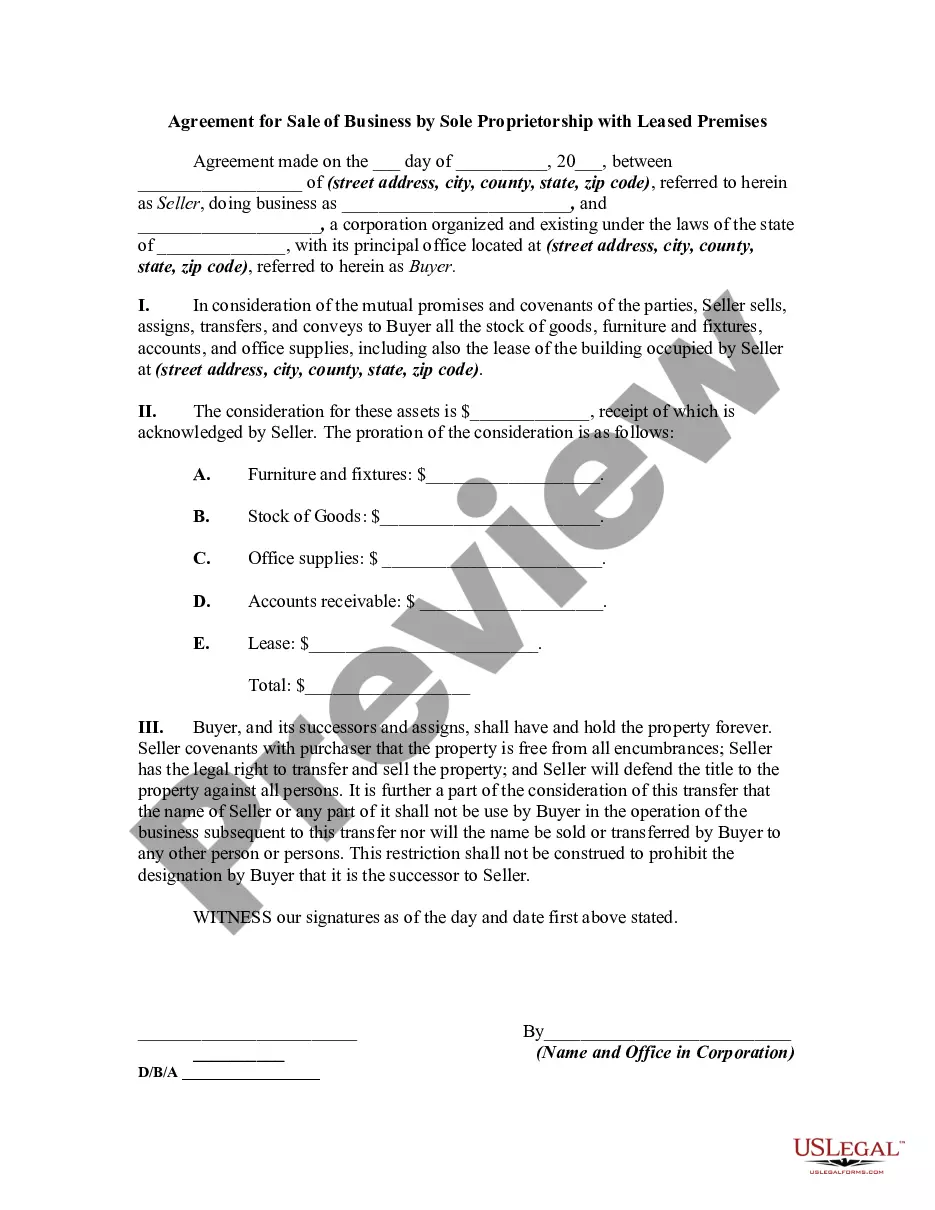

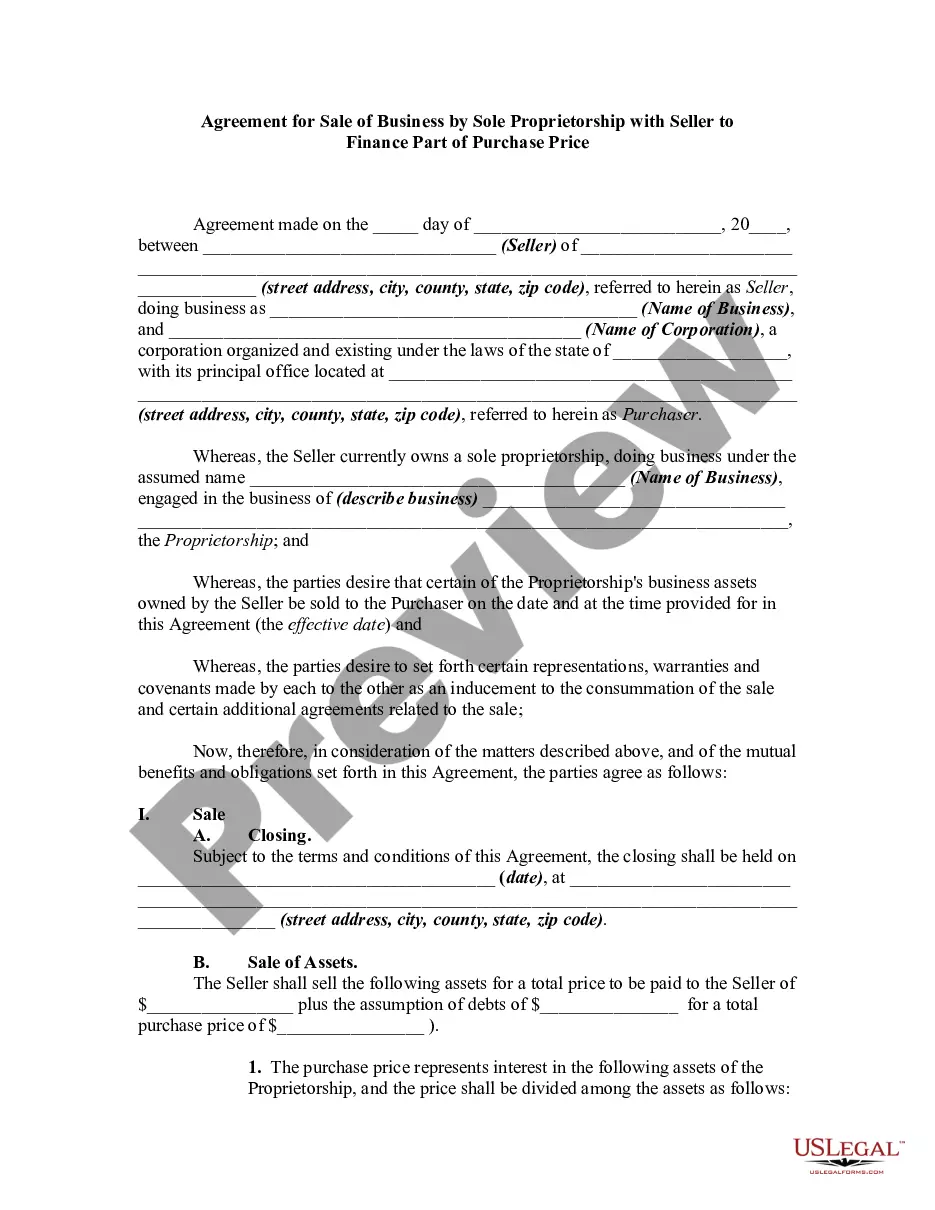

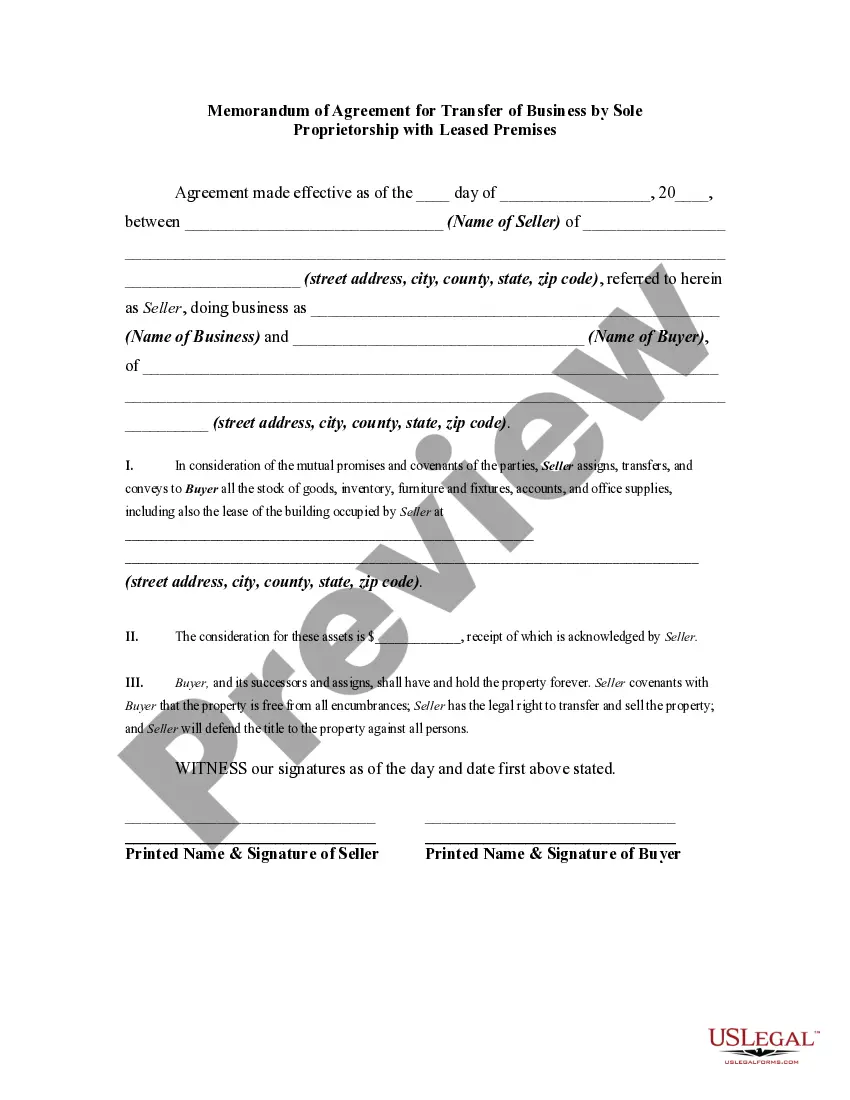

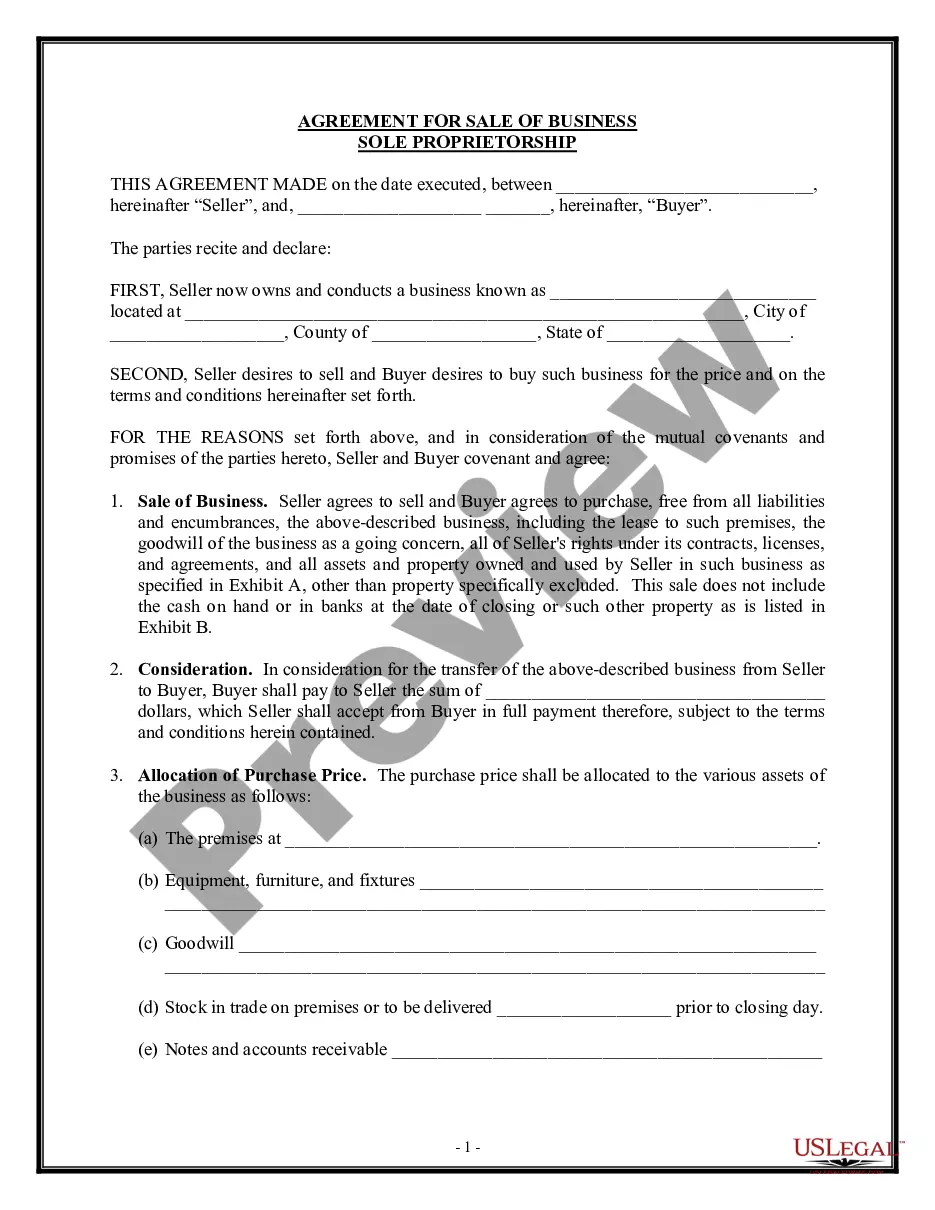

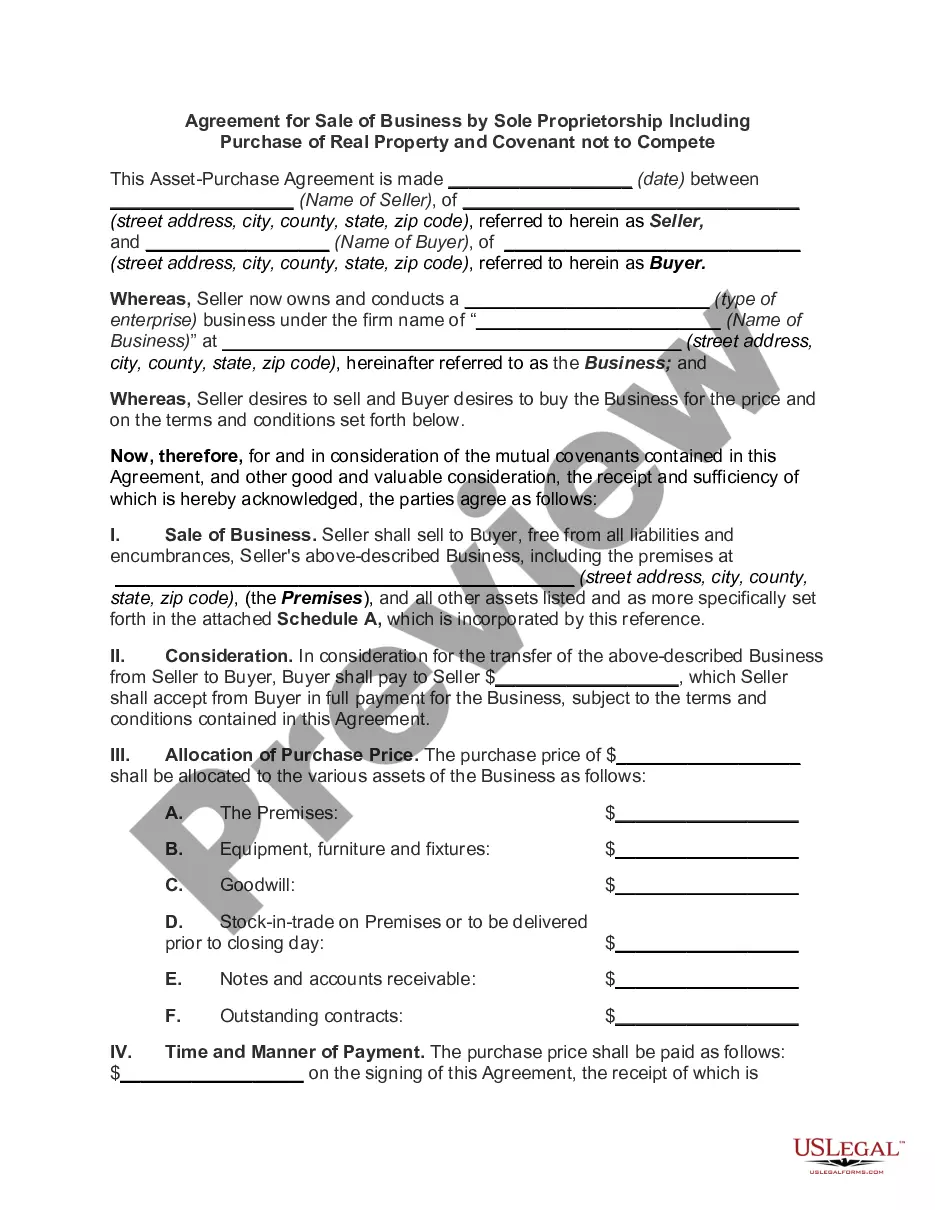

This form involves the sale of a small business where the real estate on which the Business is located is leased from a third party. This form assumes that the Seller has received the right to assign the lease from the lessor/owner.

Pennsylvania Agreement for Sale of Business by Sole Proprietorship with Leased Premises

Instant download

Description

Free preview

How to fill out Agreement For Sale Of Business By Sole Proprietorship With Leased Premises?

Finding the right legal file format can be a have difficulties. Obviously, there are a lot of layouts accessible on the Internet, but how can you find the legal form you need? Utilize the US Legal Forms site. The assistance provides thousands of layouts, including the Pennsylvania Agreement for Sale of Business by Sole Proprietorship with Leased Premises, that you can use for enterprise and private requires. All of the forms are checked out by professionals and meet up with federal and state requirements.

Should you be presently registered, log in to your accounts and click the Acquire option to have the Pennsylvania Agreement for Sale of Business by Sole Proprietorship with Leased Premises. Utilize your accounts to appear from the legal forms you have bought previously. Go to the My Forms tab of your respective accounts and acquire one more version in the file you need.

Should you be a fresh customer of US Legal Forms, listed here are simple directions that you should follow:

- Initial, be sure you have selected the correct form for the area/county. It is possible to examine the form using the Preview option and browse the form description to ensure it is the right one for you.

- When the form will not meet up with your expectations, make use of the Seach area to discover the right form.

- Once you are positive that the form is proper, click the Get now option to have the form.

- Choose the rates program you want and enter in the needed details. Design your accounts and purchase an order using your PayPal accounts or charge card.

- Choose the file format and download the legal file format to your product.

- Complete, edit and printing and sign the acquired Pennsylvania Agreement for Sale of Business by Sole Proprietorship with Leased Premises.

US Legal Forms may be the largest local library of legal forms for which you can see different file layouts. Utilize the service to download professionally-created papers that follow state requirements.

Form popularity

FAQ

Increased paperwork compared to a sole proprietor including any industry-specific licensing. Annual state filings required. Additional taxes such as a state business tax or unemployment taxes. Costs for forming and completing a tax return for an LLC are higher than those of forming a sole proprietor.

As there is no separate entity under the law for a sole proprietorship business, contracts are normally signed by owner under his or her personal name. Even if the business uses a fictitious name, the owner will usually have his or her name written down in the checks issued by the clients.

A sole proprietorship is a non-registered, unincorporated business run solely by one individual proprietor with no distinction between the business and the owner. The owner of a sole proprietorship is entitled to all profits but is also responsible for the business's debts, losses, and liabilities.

Disadvantages of a partnership include that: the liability of the partners for the debts of the business is unlimited. each partner is 'jointly and severally' liable for the partnership's debts; that is, each partner is liable for their share of the partnership debts as well as being liable for all the debts.

Disadvantages of sole trading include that: you have unlimited liability for debts as there's no legal distinction between private and business assets. your capacity to raise capital is limited. all the responsibility for making day-to-day business decisions is yours.

Overview. A sole proprietorship cannot be sold as a single entity like a corporation. Instead, when a sole proprietor sells the business, the sale is treated as the sale of the separate and identifiable assets of the business. The sale of a disregarded entity is also treated as the sale of the entity's assets.

Among one of the biggest disadvantages of a sole proprietorship is unlimited liability. This liability not only spans the business but the business owner's personal assets. Debt collectors can access your savings, property, cars, and more to see a debt repaid.

Liability: One of the major disadvantages of a sole proprietorship is that you will be personally liable for all obligations of the business. There is no separation between the assets of the owner and the assets of the business.