The Fair Credit Reporting Act (FCRA) is designed to help ensure that credit bureaus furnish correct and complete information to businesses to use when evaluating your application. Your rights include:

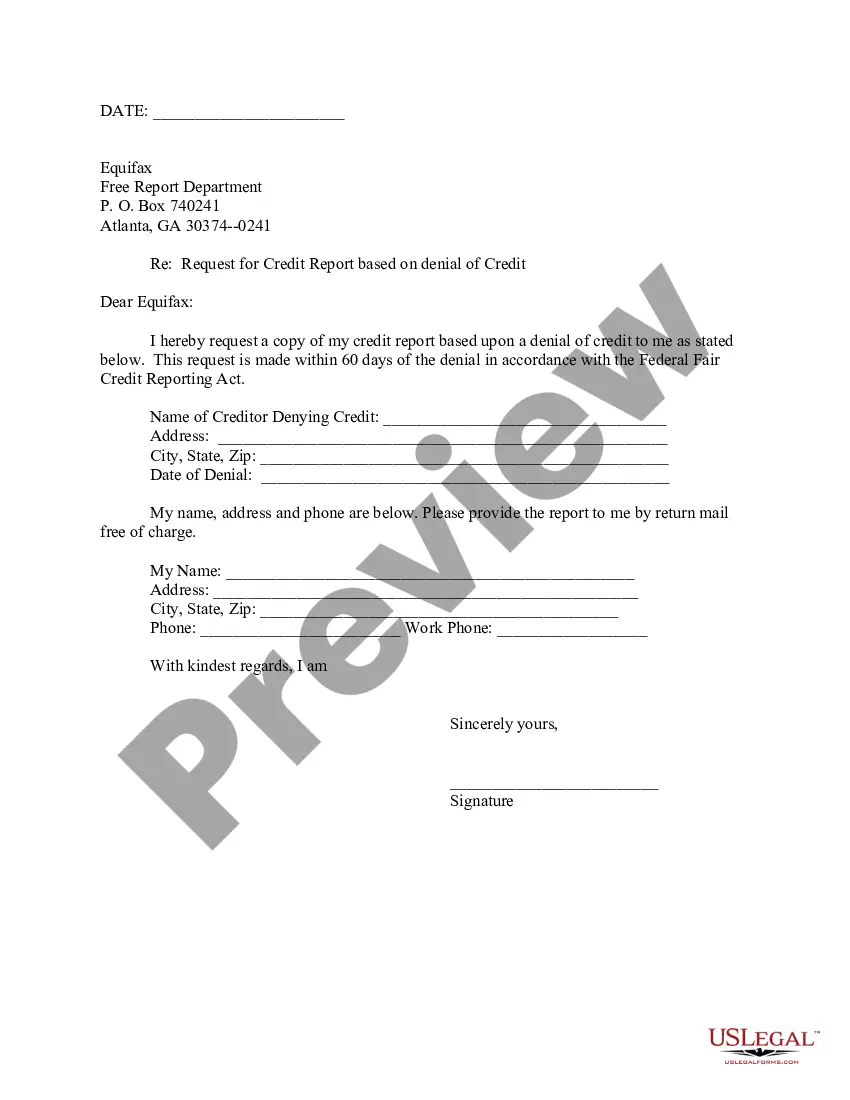

The right to receive a copy of your credit report. The copy of your report must contain all of the information in your file at the time of your request.

The right to know the name of anyone who received your credit report in the last year for most purposes or in the last two years for employment purposes.

Any company that denies your application must supply the name and address of the credit bureau they contacted, provided the denial was based on information given by the credit bureau.

The right to a free copy of your credit report when your application is denied because of information supplied by the credit bureau. Your request must be made within 60 days of receiving your denial notice.

If you contest the completeness or accuracy of information in your report, you should file a dispute with the credit bureau and with the company that furnished the information to the bureau. Both the credit bureau and the furnisher of information are legally obligated to investigate your dispute.

A right to add a summary explanation to your credit report if your dispute is not resolved to your satisfaction.

Pennsylvania Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency

Description

How to fill out Request For Disclosure Of Reasons For Denial Of Credit Application Where Action Was Based On Information Not Obtained By Reporting Agency?

US Legal Forms - among the largest libraries of authorized types in the United States - gives a wide range of authorized file web templates you can acquire or print out. While using web site, you can find a large number of types for enterprise and individual uses, sorted by groups, states, or search phrases.You will discover the latest versions of types much like the Pennsylvania Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency in seconds.

If you have a subscription, log in and acquire Pennsylvania Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency in the US Legal Forms collection. The Acquire button will appear on each form you see. You have accessibility to all formerly downloaded types from the My Forms tab of your respective accounts.

In order to use US Legal Forms for the first time, allow me to share straightforward instructions to help you started out:

- Ensure you have selected the proper form for the metropolis/region. Go through the Review button to analyze the form`s content. See the form description to actually have chosen the proper form.

- If the form doesn`t match your demands, take advantage of the Lookup industry towards the top of the display screen to get the one that does.

- In case you are pleased with the shape, verify your decision by clicking on the Acquire now button. Then, pick the pricing program you prefer and give your qualifications to sign up to have an accounts.

- Approach the deal. Make use of Visa or Mastercard or PayPal accounts to complete the deal.

- Find the structure and acquire the shape on your device.

- Make adjustments. Fill out, edit and print out and sign the downloaded Pennsylvania Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency.

Each and every web template you included with your bank account does not have an expiration time and is your own property eternally. So, if you want to acquire or print out yet another backup, just visit the My Forms area and then click around the form you require.

Get access to the Pennsylvania Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency with US Legal Forms, probably the most substantial collection of authorized file web templates. Use a large number of professional and state-certain web templates that meet up with your organization or individual needs and demands.

Form popularity

FAQ

A written statement of actual and specific reasons for the adverse action or, if not providing the specific reason within the written notice, a statement that the applicant has a right to receive the specific reason for adverse action if requested within 60 days of the notification.

The FCRA gives you the right to be told if information in your credit file is used against you to deny your application for credit, employment or insurance.

Numerous options exist on adverse action notices for reasons for the action taken. In providing documentation to the applicant, provide the reasons in the order of prominence to the action taken. Provide all the main reasons for the action; however, providing more than four reasons should generally be avoided.

In most cases, you'll receive an adverse action letter in the mail soon after your application is denied. Creditors, such as mortgage and auto lenders, personal lenders, and credit card companies are obviously allowed to deny you credit based on the information in your credit report.

A creditor must disclose the principal reasons for denying an application or taking other adverse action. The regulation does not mandate that a specific number of reasons be disclosed, but disclosure of more than four reasons is not likely to be helpful to the applicant.

Regulation B A written statement of actual and specific reasons for the adverse action or, if not providing the specific reason within the written notice, a statement that the applicant has a right to receive the specific reason for adverse action if requested within 60 days of the notification.

The FCRA also requires a creditor to disclose, as applicable, a credit score it used in taking adverse action along with related information, including up to four key factors that adversely affected the consumer's credit score (or up to five factors if the number of inquiries made with respect to that consumer report ...

An adverse action notice is intended to inform borrowers of the reasons why their loan application was rejected. It contains information regarding the causes of rejection as well as the processes in place to address disputes.