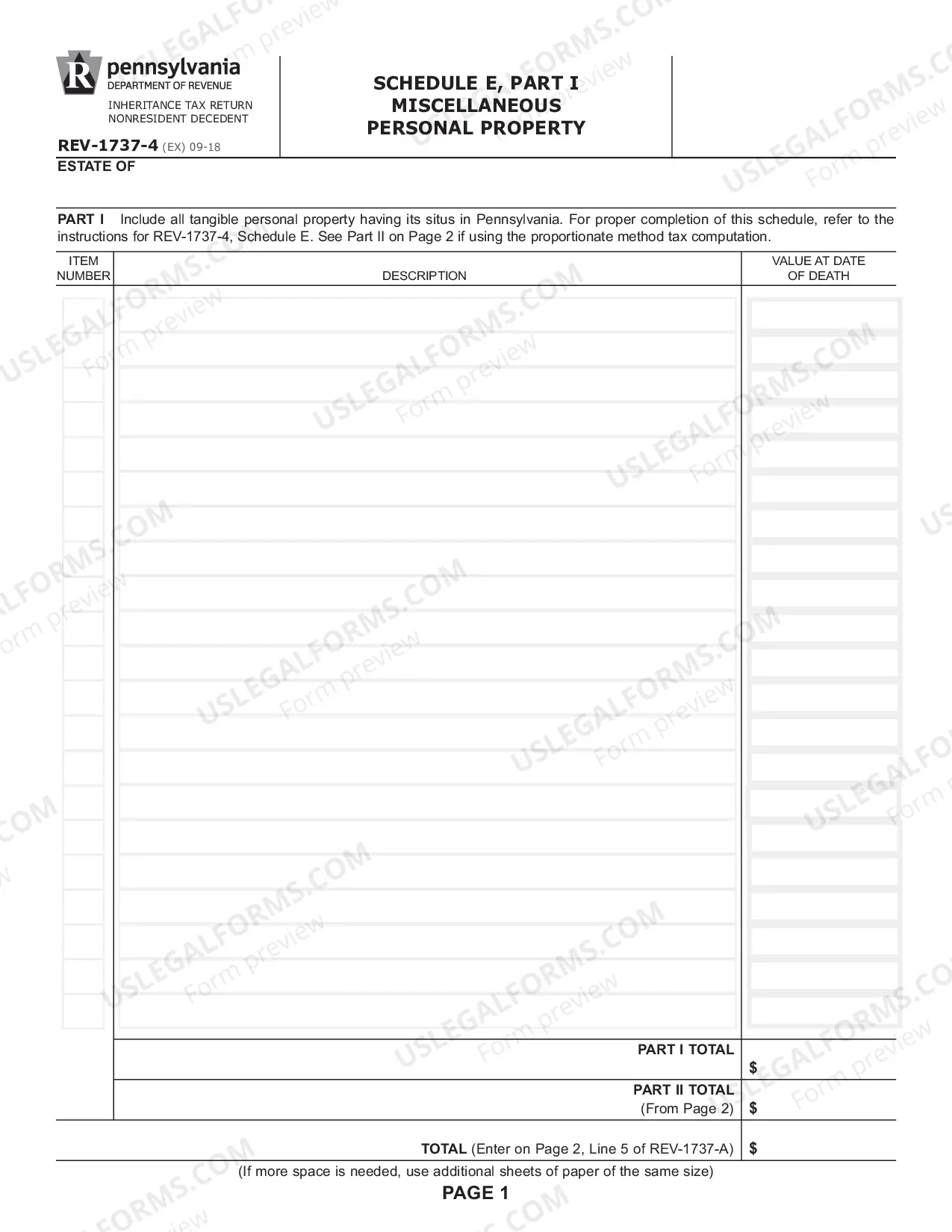

The Pennsylvania REV-346 -- Estate Information Sheet is a form used to collect information about an estate in Pennsylvania. It is required to be completed and filed with the Register of Wills in Pennsylvania when someone dies. There are three different types of Pennsylvania REV-346 -- Estate Information Sheet: the short form, the long form, and the supplemental form. The short form is the most commonly used and is used for estates that do not have a taxable estate. It requires the following information: the personal representative's name, address, and contact information; the decedent's name, address, and cause of death; and the name and address of any attorney representing the estate. The long form is used for estates with a taxable estate. It requires the same information as the short form as well as additional information such as the decedent's marital status, the date of death, the surviving spouse's name, the value of the estate, and any assets subject to federal or state estate tax. The supplemental form is used to supplement the information included on the short or long form. It requires information such as the decedent's Social Security number, the date of the decedent's marriage, and the date of any divorce. It also requires information about any trusts established by the decedent. In summary, the Pennsylvania REV-346 -- Estate Information Sheet is a form used to collect information about an estate in Pennsylvania. There are three different types of this form: the short form, the long form, and the supplemental form. Each form collects different types of information depending on the size and complexity of the estate.

Pennsylvania REV-346 -- Estate Information Sheet

Description

How to fill out Pennsylvania REV-346 -- Estate Information Sheet?

US Legal Forms is the most easy and affordable way to locate appropriate legal templates. It’s the most extensive web-based library of business and personal legal documentation drafted and checked by legal professionals. Here, you can find printable and fillable blanks that comply with federal and local laws - just like your Pennsylvania REV-346 -- Estate Information Sheet.

Getting your template takes only a few simple steps. Users that already have an account with a valid subscription only need to log in to the website and download the document on their device. Afterwards, they can find it in their profile in the My Forms tab.

And here’s how you can get a properly drafted Pennsylvania REV-346 -- Estate Information Sheet if you are using US Legal Forms for the first time:

- Read the form description or preview the document to ensure you’ve found the one corresponding to your demands, or locate another one utilizing the search tab above.

- Click Buy now when you’re certain about its compatibility with all the requirements, and judge the subscription plan you like most.

- Register for an account with our service, sign in, and pay for your subscription using PayPal or you credit card.

- Choose the preferred file format for your Pennsylvania REV-346 -- Estate Information Sheet and download it on your device with the appropriate button.

Once you save a template, you can reaccess it whenever you want - just find it in your profile, re-download it for printing and manual fill-out or import it to an online editor to fill it out and sign more efficiently.

Take advantage of US Legal Forms, your trustworthy assistant in obtaining the required formal documentation. Try it out!

Form popularity

FAQ

The tax is paid on any assets the decedent controlled, such as real estate, bank accounts, car titles, and revocable trusts. Generally, a decedent (while alive) does not control an irrevocable trust ? so there's no inheritance tax on an irrevocable trust.

The tax rate for Pennsylvania Inheritance Tax is 4.5% for transfers to direct descendants (lineal heirs), 12% for transfers to siblings, and 15% for transfers to other heirs (except charitable organizations, exempt institutions, and government entities that are exempt from tax).

Property owned jointly between spouses is exempt from inheritance tax.

How To Avoid Inheritance Tax. One way to avoid inheritance tax in PA is to make an asset joint. For example, if you have $30,000 in your name alone, and through your will, you give it to a friend of yours, it would be taxed at 15% or they would owe $4,500 in taxes.

Assets Owned In a Revocable Trust: Generally, if someone dies owning assets in a revocable trust over which he or she had access and control those assets, those assets will be 100% taxable for Pennsylvania inheritance tax purposes.

However, creditors have at least 1 year from the date of death to make any claims, even if the debt would otherwise expire during that 1-year period (see 20 PA Cons Stat § 3383). Once a creditor makes a claim to the executor, the statute of limitations is suspended, and the debt does not expire.

Pennsylvania Inheritance Tax and Gift Tax No tax is applied to transfers to a surviving spouse or to a parent from a child under the age of 21. There is a 4.5% tax applied to transfers to direct descendants and other lineal heirs like grandchildren.

Property owned jointly between spouses is exempt from inheritance tax. Effective for estates of decedents dying after June 30, 2012, certain farm land and other agricultural property are exempt from Pennsylvania inheritance tax, provided the property is transferred to eligible recipients.