Pennsylvania Estate information Sheet

Understanding this form

The Estate Information Sheet is a crucial legal document used in the probate process. It collects essential information about the decedent and the estate, facilitating the evaluation and processing of estate tax returns. This form differs from other probate forms by specifically focusing on tax-related information and the appointed personal representative's details, ensuring compliance with state regulations regarding estate administration.

Key parts of this document

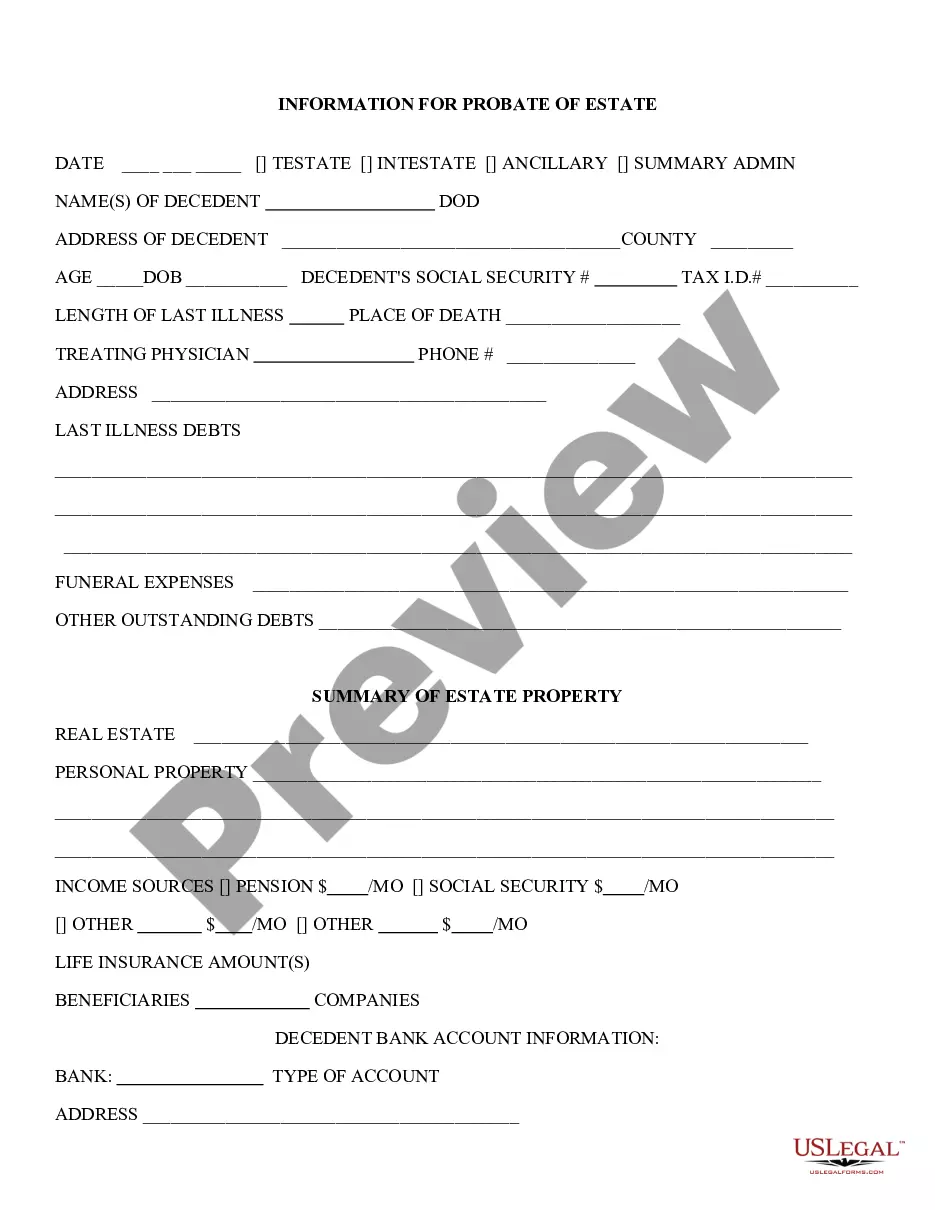

- Decedent Information: Includes the decedent's name, Social Security number, date of death, and date of birth.

- Type of Filing: Specifies the nature of the return being filed, whether it's a probate return, for joint assets, estate tax only, or for litigation purposes.

- Letters Granted: Indicates the type of legal proceedings at the Register of Wills Office, such as testamentary or administration letters.

- Attorney/Correspondent Information: Contains details of the attorney or correspondent who will receive all tax information.

- Personal Representative Information: Captures the contact information and Social Security numbers of the executor or administrator of the estate.

When to use this document

This form is utilized when initiating the probate process after someone's death. It is specifically required when filing for estate taxes, claiming joint assets, or in contexts involving contested estate matters. Use this form to properly document all necessary details for legal and tax purposes, ensuring that the decedent's estate is handled according to state laws.

Who this form is for

- Personal representatives responsible for managing the estate of a deceased individual.

- Attorneys representing estates in the probate process.

- Individuals filing estate tax returns on behalf of a decedent's estate.

Completing this form step by step

- Enter the decedent's full name, Social Security number, date of death, and date of birth accurately.

- Select the type of filing by marking the appropriate checkbox.

- Indicate the letters granted by marking the correct option regarding the nature of the proceedings.

- Provide the name and contact information of the attorney or correspondent handling estate correspondence.

- List the personal representative's details, including the executor or administrator, along with their Social Security number and contact information.

Notarization requirements for this form

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Neglecting to provide accurate decedent information, which can cause processing delays.

- Failing to mark the appropriate checkboxes for type of filing and letters granted.

- Omitting the Social Security numbers of personal representatives.

- Not entering the attorney's information completely, leading to communication issues with the tax department.

Why use this form online

- Convenience: Download the form instantly from home without visiting an office.

- Editable: Customize the form to meet specific needs before printing.

- Reliable: Access professionally drafted templates created by licensed attorneys.

Looking for another form?

Form popularity

FAQ

Pennsylvania inheritance tax rates A 4.5% tax rate applies to assets that go to lineal heirs. These include children, stepchildren and grandchildren. A 12% tax rate applies to collateral beneficiaries such as siblings. A 15% tax rate applies to other heirs such as nieces and nephews.

Ing to the Internal Revenue Service (IRS), federal estate tax returns are only required for estates with values exceeding $12.06 million in 2022 (rising to $12.92 million in 2023). If the estate passes to the spouse of the deceased person, no estate tax is assessed.318 Taxes for 2022 are paid in 2023.

Property owned jointly between spouses is exempt from inheritance tax. Effective for estates of decedents dying after June 30, 2012, certain farm land and other agricultural property are exempt from Pennsylvania inheritance tax, provided the property is transferred to eligible recipients.

Pennsylvania Inheritance Tax and Gift Tax No tax is applied to transfers to a surviving spouse or to a parent from a child under the age of 21. There is a 4.5% tax applied to transfers to direct descendants and other lineal heirs like grandchildren.

In Pennsylvania, it is only necessary to probate if the decedent owned assets, whether financial or real estate holdings, solely in their name which did not already have a beneficiary designated. Such assets are called probate assets, and in order to convey ownership of them it is necessary to probate.

All real property and all tangible personal property of a resident decedent, including but not limited to cash, automobiles, furniture, antiques, jewelry, etc., located in Pennsylvania at the time of the decedent's death is taxable.

Pennsylvania treats a son-in-law or daughter-in-law as if they are a child for purposes of the inheritance tax. As a result, there is a flat 4.5% PA inheritance tax on assets that pass to the wife or widow and husband or widower of the decedent's child.

The tax rate for Pennsylvania Inheritance Tax is 4.5% for transfers to direct descendants (lineal heirs), 12% for transfers to siblings, and 15% for transfers to other heirs (except charitable organizations, exempt institutions, and government entities that are exempt from tax).