Oregon Last Will and Testament with All Property to Trust called a Pour Over Will

Description

Key Concepts & Definitions

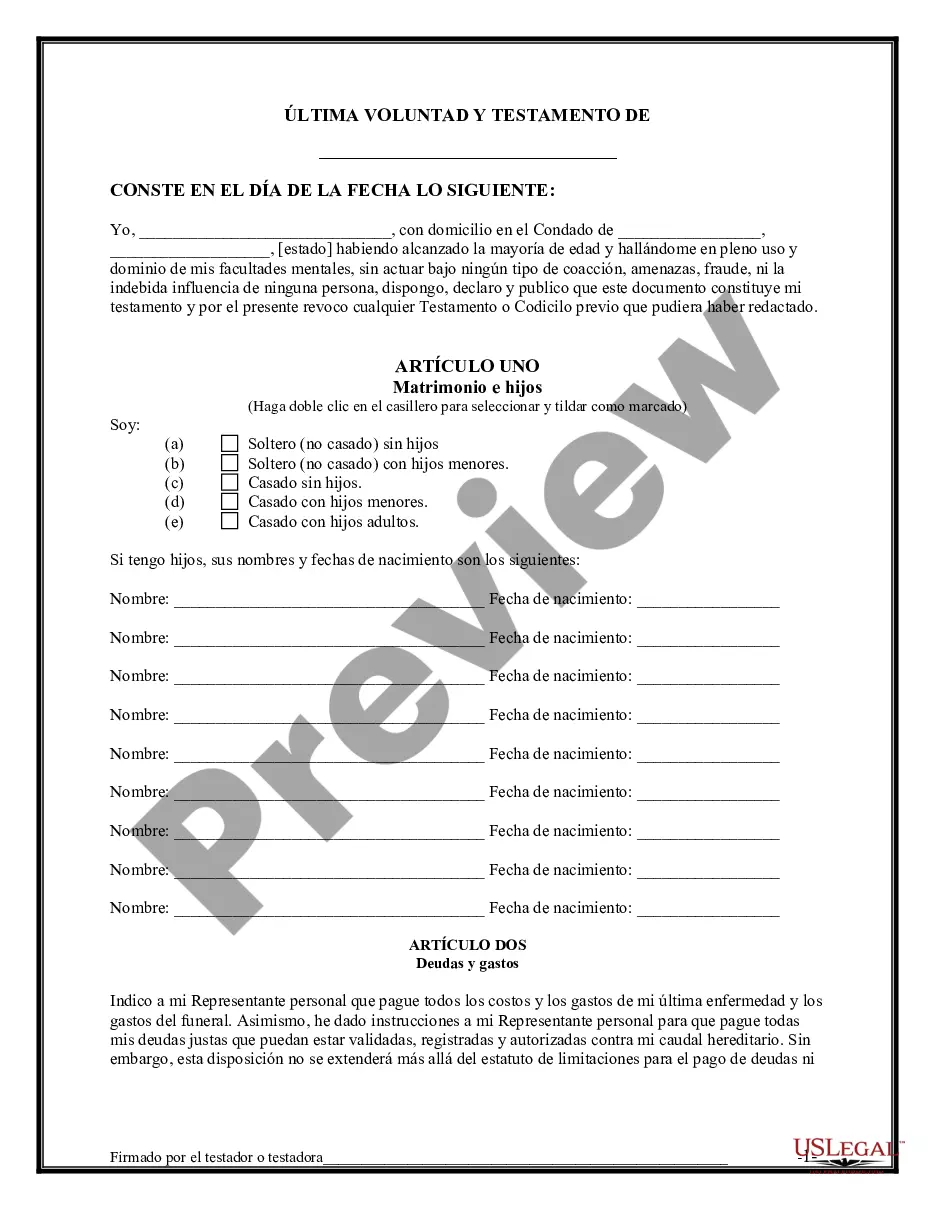

Last will and testament with all property to trust refers to a legal document where an individual (the testator) specifies that all or a portion of their property should be transferred into a trust upon their death. This type of will typically works in conjunction with trusts estates law, which governs the creation and managing of trusts for asset protection planning and estate planning purposes.

Step-by-Step Guide to Creating a Will with All Property to Trust

- Consult with an Estate Planning Attorney: Discuss your estate goals with a professional specializing in estate planning services to ensure legal compliance and tailor a plan that suits your needs.

- Decide on the Type of Trust: Choose between revocable vs irrevocable trusts based on your asset protection and estate planning goals.

- Detail Your Assets: List all your assets and determine which ones will be placed in the trust.

- Designate Beneficiaries: Specify who will benefit from the trust after your death. Consider benefits for veterans if applicable.

- Sign and Notarize: Finalize your will and have it signed in the presence of witnesses and notarized to make it legally binding.

Risk Analysis

- Legal Disputes: Inadequate documentation or failure to comply with legal norms might lead to disputes during the probate process.

- Financial Mismanagement: If the trust is not managed well, it could lead to financial losses for the beneficiaries.

- Changing Laws: Trusts and estate laws can evolve, impacting how your assets are handled post-mortem, necessitating regular reviews and updates of your estate plan.

Common Mistakes & How to Avoid Them

- Not Updating the Will: Regularly update your will to reflect changes in assets, beneficiaries, or personal circumstances to avoid conflicts.

- Choosing the Wrong Type of Trust: Understand the difference between revocable and irrevocable trusts or consult estate planning services to choose the best option for your situation.

- Omitting Details: Ensure all details are covered, including provisions for medical care planning and any specific benefits for veterans.

FAQ

What is the probate process? The probate process is the legal procedure through which a deceased person's will is validated, and their assets are distributed under court supervision.

Can I set up a payment plan for estate planning services? Yes, many attorneys offer a payment plan available to cover the costs of their services, making them more accessible.

What is asset protection planning? Asset protection planning involves strategies to protect ones assets from creditors or lawsuits, often through the creation of trusts.

How to fill out Oregon Last Will And Testament With All Property To Trust Called A Pour Over Will?

Creating papers isn't the most uncomplicated process, especially for those who rarely deal with legal paperwork. That's why we advise utilizing correct Oregon Legal Last Will and Testament Form with All Property to Trust called a Pour Over Will templates created by professional attorneys. It allows you to eliminate troubles when in court or working with official institutions. Find the files you want on our website for top-quality forms and accurate descriptions.

If you’re a user having a US Legal Forms subscription, just log in your account. As soon as you are in, the Download button will automatically appear on the template web page. After downloading the sample, it’ll be stored in the My Forms menu.

Customers without a subscription can easily get an account. Use this simple step-by-step guide to get the Oregon Legal Last Will and Testament Form with All Property to Trust called a Pour Over Will:

- Be sure that the sample you found is eligible for use in the state it is required in.

- Confirm the file. Make use of the Preview option or read its description (if available).

- Buy Now if this sample is the thing you need or return to the Search field to find another one.

- Choose a convenient subscription and create your account.

- Use your PayPal or credit card to pay for the service.

- Download your file in a wanted format.

After finishing these easy steps, you can fill out the form in an appropriate editor. Check the completed data and consider requesting a legal professional to review your Oregon Legal Last Will and Testament Form with All Property to Trust called a Pour Over Will for correctness. With US Legal Forms, everything becomes easier. Try it out now!

Form popularity

FAQ

Combining a Will and Trust Together: Should You Use Both? The use of a living trust and a will together as part of your estate planning is acceptable under California law. The benefit of this approach is that you can address separate issues on each document.

No a will does not override a deed. A will only acts on death. The deed must be signed during the life of the owner. The only assets that pass through the will are assets that are in the name of the decedent only.

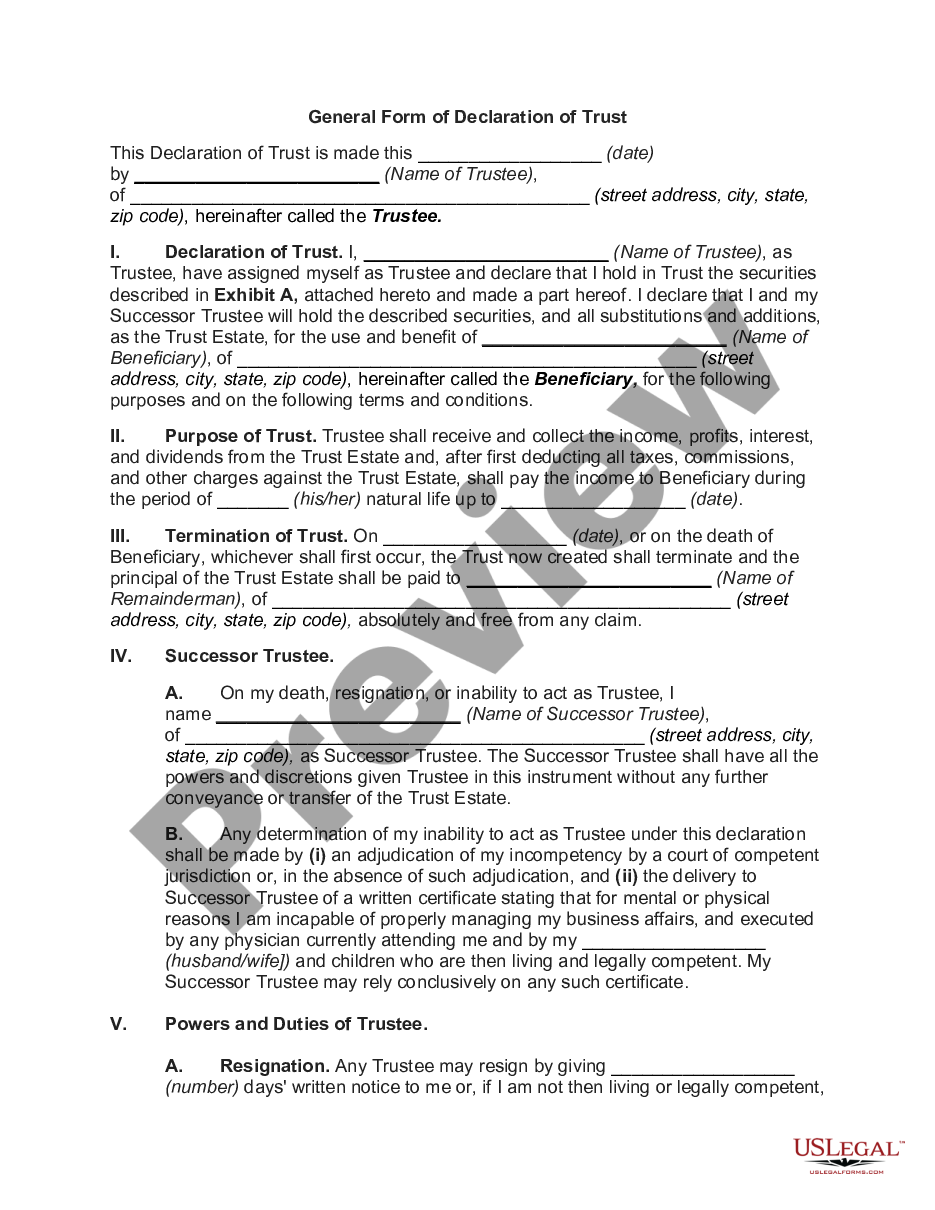

Important: Although a revocable trust supersedes a will, the trust only controls those assets that have been placed into it. Therefore, if a revocable trust is formed, but assets are not moved into it, the trust provisions have no effect on those assets, at the time of the grantor's death.

While a will determines how your assets will be distributed after you die, a trust becomes the legal owner of your assets the moment the trust is created.

An estate plan that includes a trust costs $1,000 to $3,000, versus $300 or less for a simple will. What a living-trust promoter may not tell you: You don't need a trust to protect assets from probate. You can arrange for most of your valuable assets to go to your heirs outside of probate.

A revocable trust becomes irrevocable at the death of the person that created the trust.The Trust becomes its own entity and needs a tax identification number for filing of returns. 2. The Grantor (also called the Trustor) of the Trust becomes incapacitated.

One main difference between a will and a trust is that a will goes into effect only after you die, while a trust takes effect as soon as you create it. A will is a document that directs who will receive your property at your death and it appoints a legal representative to carry out your wishes.

When people make revocable living trusts to avoid probate, it's common for them to also make what's called a "pour-over will." The will directs that if any property passes through the will at the person's death, it should be transferred to (poured into) the trust, and then distributed to the beneficiaries of the trust.

Make a List of All Your Assets. Be sure to include make a list of your assets that includes everything you own. Find the Paperwork for Your Assets. Choose Beneficiaries. Choose a Successor Trustee. Choose a Guardian for Your Minor Children.