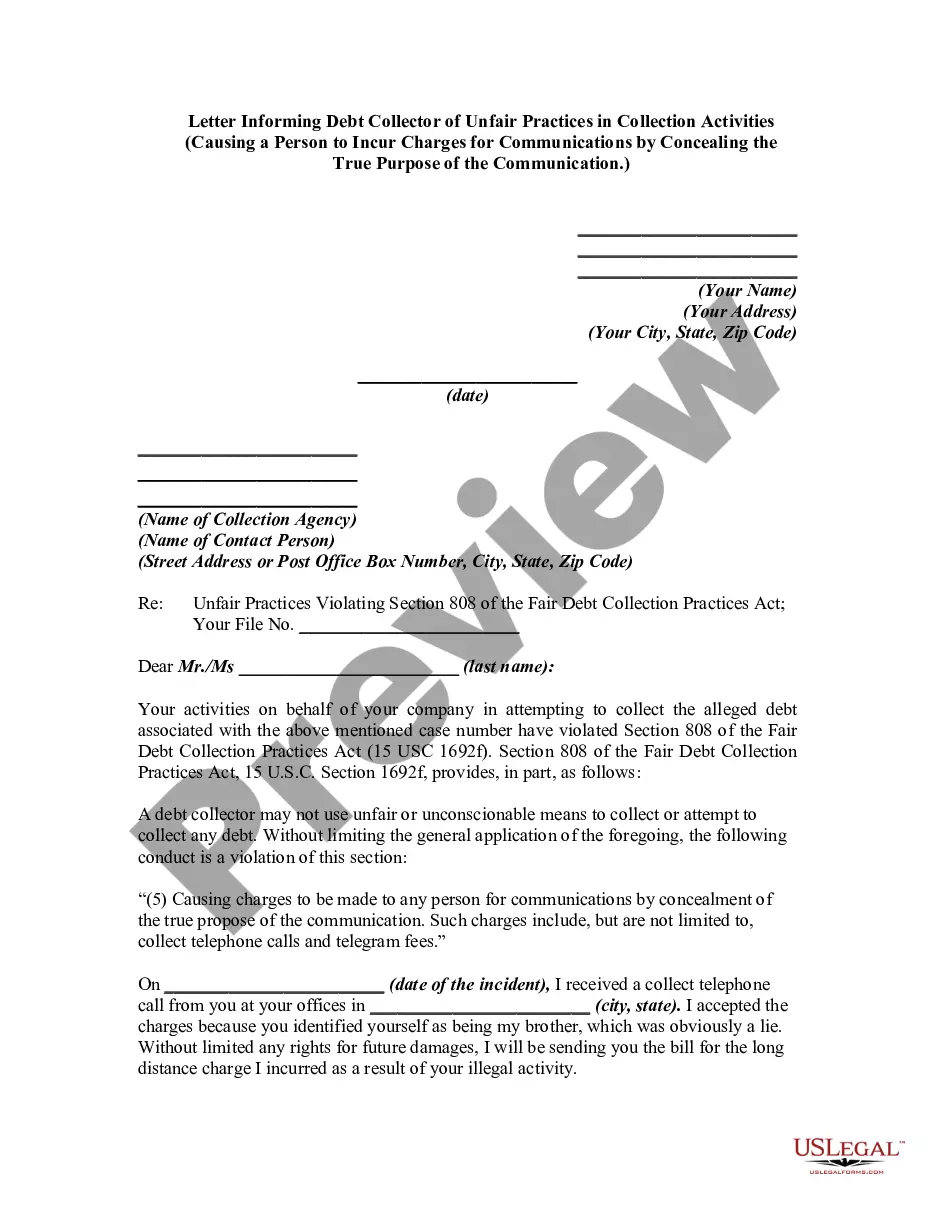

A debt collector may not use unfair or unconscionable means to collect a debt. This includes causing a person to incur charges for communications by concealing the true propose of the communication.

Oregon Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication

Category:

State:

Multi-State

Control #:

US-DCPA-44

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Causing A Consumer To Incur Charges For Communications By Concealing The Purpose Of The Communication?

Are you currently facing a scenario where you will require documentation for either organizational or personal reasons almost every day.

There is a range of legal document templates available online, but finding reliable forms is not straightforward.

US Legal Forms offers thousands of document templates, such as the Oregon Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication, crafted to comply with state and federal regulations.

Select the pricing plan you prefer, complete the necessary information to create your account, and pay for your order using PayPal or a credit card.

Choose a convenient file format and download your copy. Retrieve all the document templates you have purchased from the My documents menu. You can obtain another copy of the Oregon Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication any time you need. Click on the required document to download or print the template. Use US Legal Forms, the most extensive collection of legal documents, to save time and avoid mistakes. The service offers well-crafted legal document templates that can be utilized for various purposes. Create your account on US Legal Forms and start simplifying your life.

- If you are already familiar with the US Legal Forms website and have an account, just Log In.

- Then, you can download the Oregon Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication template.

- If you don't have an account and wish to start using US Legal Forms, follow these instructions.

- Locate the document you need and ensure it is for the correct city/county.

- Utilize the Review button to inspect the form.

- Verify the details to make certain you have selected the appropriate document.

- If the document isn't what you're looking for, use the Search field to find the form that suits your requirements.

- When you discover the right document, click on Get now.

Form popularity

FAQ

Ask CFPBWho you're talking to (get the person's name)The name of the debt collection company they work for.The company's address and phone number.The name of the original creditor.The amount owed.How you can dispute the debt or ensure that the debt is yours.

If the FDCPA is violated, the debtor can sue the debt collection company as well as the individual debt collector for damages and attorney fees.

No harassment The Fair Debt Collection Practices Act (FDCPA) says debt collectors can't harass, oppress, or abuse you or anyone else they contact. Some examples of harassment are: Repetitious phone calls that are intended to annoy, abuse, or harass you or any person answering the phone. Obscene or profane language.

The definition of debt collection harassment is to intimidate, abuse, coerce, bully or browbeat consumers into paying off debt. This happens most often over the phone, but harassment could come in the form of emails, texts, direct mail or talking to friends or neighbors about your debt.

Once you dispute the debt, the debt collector must stop all debt collection activities until it sends you verification of the debt. You can also use the sample dispute letter to discover the name and address of the original creditor. As with all dispute letters, you should keep a copy of the letter for your records.

If, within the 30-day period, the consumer disputes in writing any portion of the debt or requests the name and address of the original creditor, the collector must stop all collection efforts until he or she mails the consumer a copy of a judgment or verification of the debt, or the name and address of the original

Within five days after a debt collector first contacts you, it must send you a written notice, called a "validation notice," that tells you (1) the amount it thinks you owe, (2) the name of the creditor, and (3) how to dispute the debt in writing.

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.

It is well known that a debt collector is only entitled to charge fees that are prescribed by the Debt Collectors Act. The debt collector, and the creditor for that matter, has no discretion whatsoever as to whether they may charge anything else besides the prescribed fees.