Oklahoma Business Deductibility Checklist

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Business Deductibility Checklist?

US Legal Forms - one of the top collections of legal documents in the United States - provides a range of legal form templates that you can download or print.

By using the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can find the latest versions of forms such as the Oklahoma Business Deductibility Checklist in moments.

If you have a membership, Log In and download the Oklahoma Business Deductibility Checklist from the US Legal Forms catalog. The Download button will appear on every form you view. You can access all previously saved forms in the My documents section of your account.

Complete the purchase. Use your credit card or PayPal account to finalize the transaction.

Choose the format and download the form to your device. Edit. Fill in, modify, print, and sign the saved Oklahoma Business Deductibility Checklist. Each template you add to your account has no expiration date and is permanently yours. So, if you wish to download or print another copy, simply go to the My documents section and click on the form you need. Access the Oklahoma Business Deductibility Checklist with US Legal Forms, the most extensive collection of legal document templates. Utilize thousands of professional and state-specific templates that cater to your business or personal needs and requirements.

- Ensure that you have selected the appropriate form for your city/state.

- Click the Preview button to review the contents of the form.

- Check the form details to make sure you have selected the correct one.

- If the form does not meet your requirements, use the Search bar at the top of the screen to find one that does.

- When satisfied with the form, confirm your selection by clicking the Purchase now button.

- Then, choose the pricing plan you prefer and provide your details to register for an account.

Form popularity

FAQ

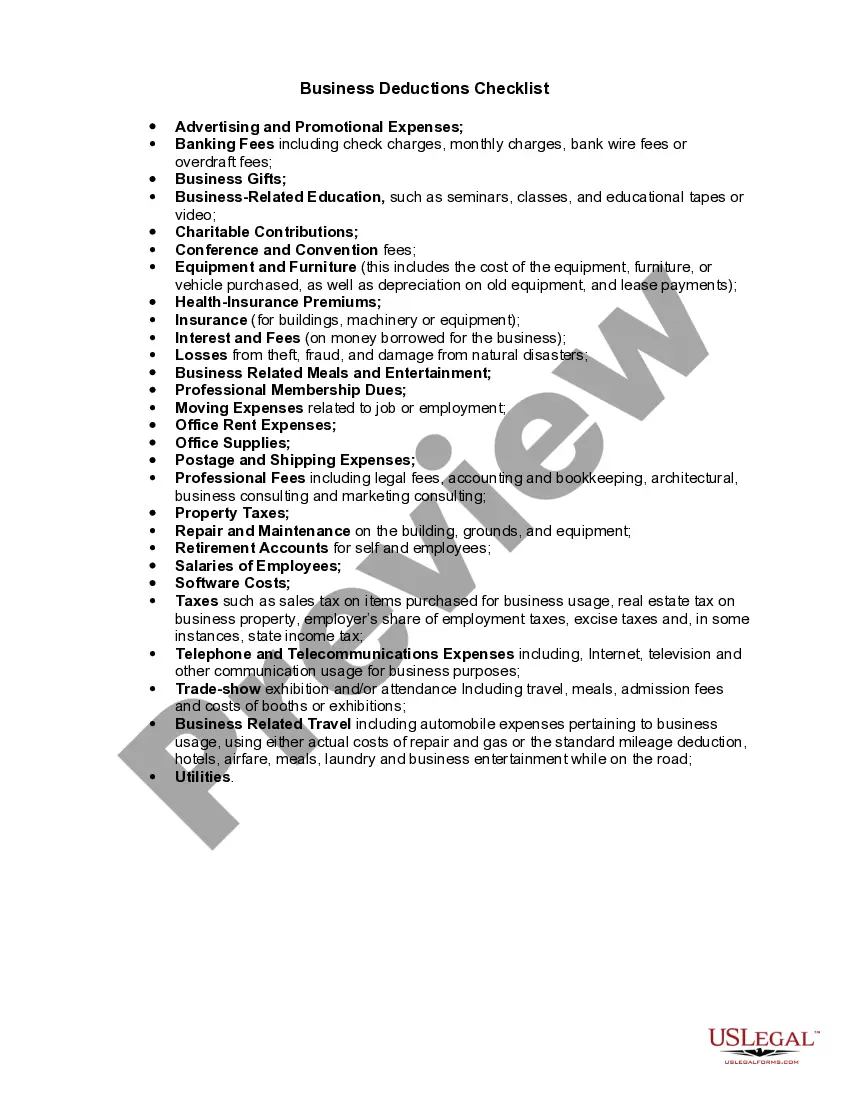

Costs you can claim as allowable expensesoffice costs, for example stationery or phone bills.travel costs, for example fuel, parking, train or bus fares.clothing expenses, for example uniforms.staff costs, for example salaries or subcontractor costs.things you buy to sell on, for example stock or raw materials.More items...

Office supplies, credit card processing fees, tax preparation fees, and repairs and maintenance for business property and equipment are also deductible. Still, other business expenses can be depreciated or amortized, meaning that you can deduct a small amount of the cost each year over several years.

If the company owns them for five years or more and later sells them for a value greater than their purchase price, then a capital gain on the transaction is recognized. Under current Oklahoma law, Widget Manufacturing's capital gain is eligible for the Oklahoma capital gain exemption.

Yes, getting a business off the ground takes time, and the IRS recognizes this. In your first few months or year of operation you may not bring in any income. Even without income, you may be able to deduct your expenses, as long as you meet certain IRS guidelines.

Federal tax laws allow LLCs to deduct initial startup costs, as long as the expenses occurred before it begins conducting business. A business is considered active the first time the company's services are offered to the public. The IRS sets a $5,000 deduction limit on startup and organizational costs.

What expenses can you write off as an LLC? There is a long list of expenses that you can deduct as an LLC. Some of the main operating costs that can be deducted include startup costs, supplies, business taxes, office costs, salaries, travel costs, and rent costs.

According to the Internal Revenue Service (IRS), business expenses are ordinary and necessary costs incurred to operate your business. Examples include inventory, payroll and rent. Fixed expenses are regular and don't change much things like rent and insurance. Variable expenses are expected, but they can change.

Types of Deductible ExpensesSelf-Employment Tax.Startup Business Expenses.Office Supplies and Services.Advertisements.Business Insurance.Business Loan Interest and Bank Fees.Education.Depreciation.More items...?

Business location expenses are deductible for tax purposes by an LLC. If the owner or owners of the LLC operate it from a home office, then such things as supplies and a phone meant specifically for business qualify as business expenses that can be written off.

To qualify for the Oklahoma deduction, the gain must be earned as a result of the sale of stock or ownership interest in an Oklahoma company, limited liability company, or partnership and the stock or ownership interest must have been held by the taxpayer for at least three (3) uninterrupted years prior to the date of