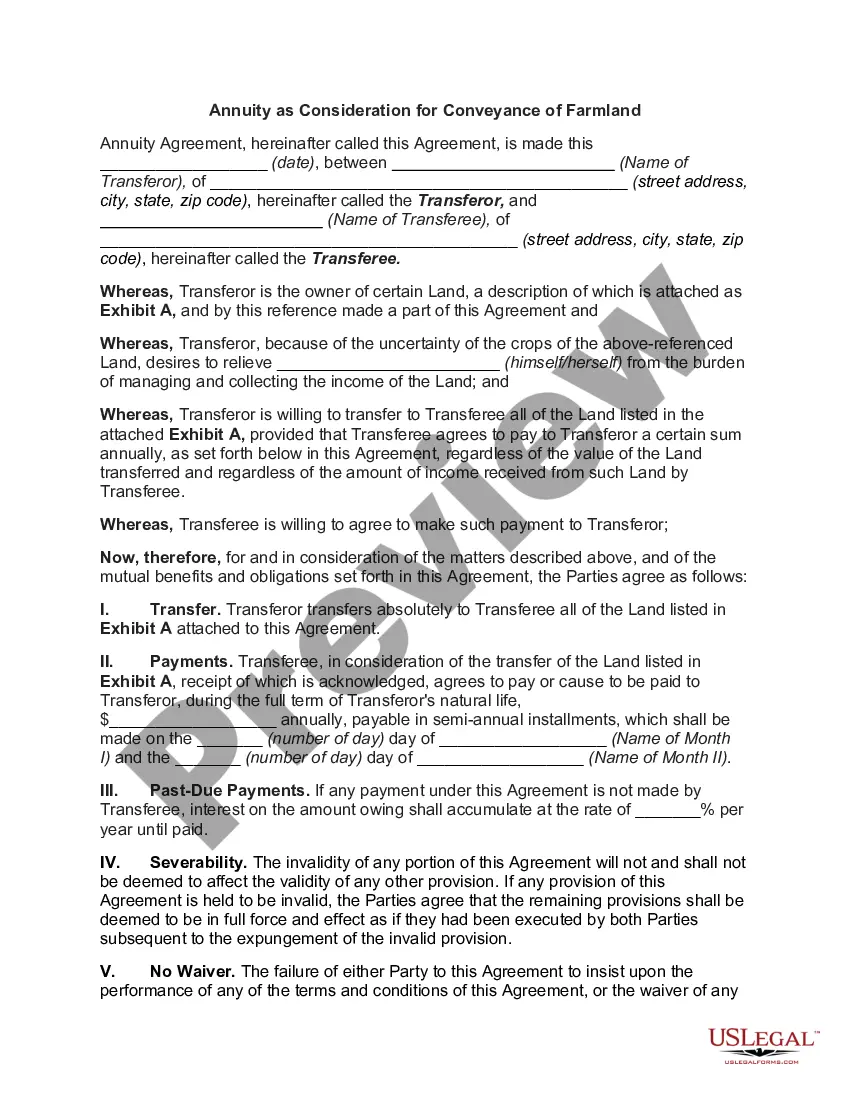

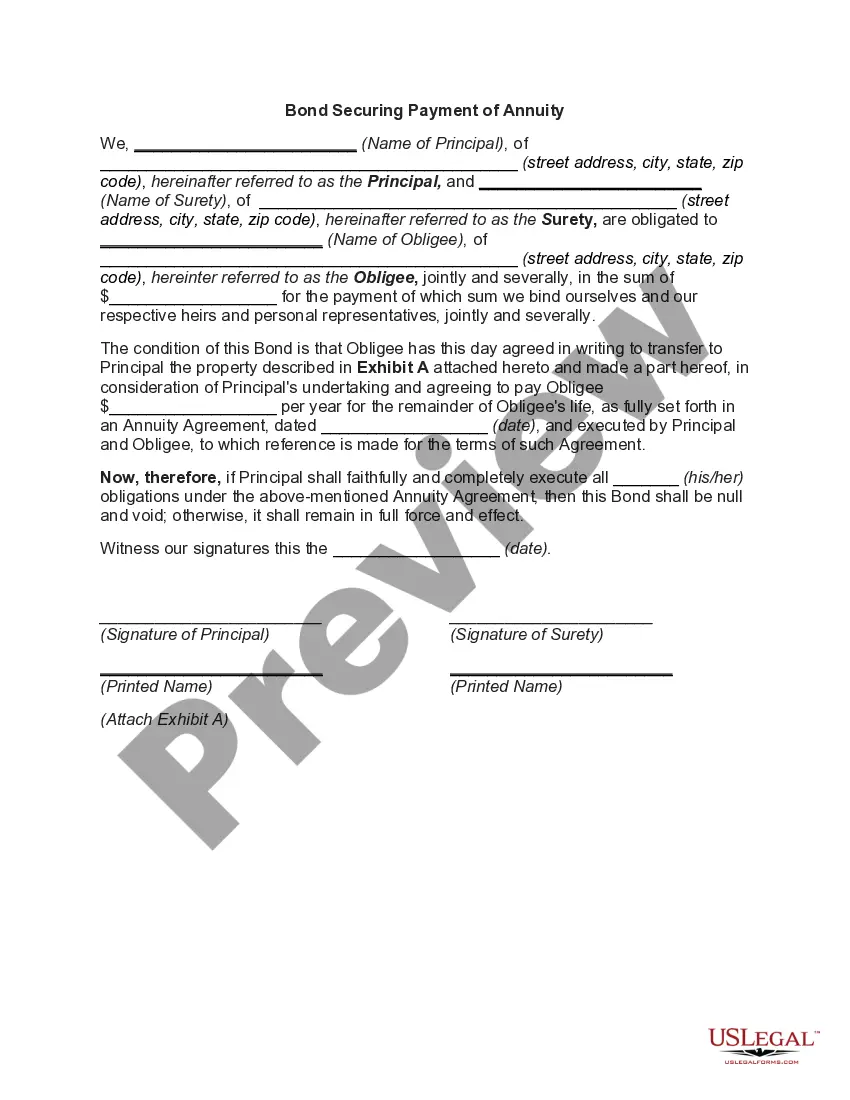

Oklahoma Annuity as Consideration for Transfer of Securities

Description

How to fill out Annuity As Consideration For Transfer Of Securities?

It is feasible to spend time online looking for the sanctioned document template that meets the state and national criteria you desire.

US Legal Forms offers thousands of sanctioned templates that can be assessed by professionals.

You can conveniently acquire or print the Oklahoma Annuity as Consideration for Transfer of Securities from the services.

If offered, utilize the Preview button to view the document template as well.

- If you have a US Legal Forms account, you can Log In and click on the Obtain button.

- Subsequently, you can complete, modify, print, or sign the Oklahoma Annuity as Consideration for Transfer of Securities.

- Every sanctioned document template you buy is yours permanently.

- To get an additional copy of the purchased form, go to the My documents tab and click on the relevant button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure that you have selected the correct document template for the region/area that you choose.

- Check the form description to confirm that you have selected the right template.

Form popularity

FAQ

The non-resident filing threshold for Oklahoma is typically based on the amount of income earned within the state. If your income exceeds this threshold, you will need to file an Oklahoma tax return. It's important to consider how the Oklahoma Annuity as Consideration for Transfer of Securities could impact your calculations and any tax liabilities. For personalized guidance, seeking help from an accountant or tax expert familiar with Oklahoma laws is a wise choice.

If you own an annuity inside of a Traditional IRA, the transfer is from one retirement account IRA to another retirement account IRA. It is a non-taxable event.

A 1035 transfer is a tax-free transfer from one insurance company annuity to another. You don't pay taxes or penalties if you transfer the funds this way.

Anyone selling variable annuities must carry a securities license. Learn from the experts and get our 101-level guide, Annuities Explained, delivered to your inbox for free.

The most clear-cut way to withdraw money from an annuity without penalty is to wait until the surrender period expires. If your contract includes a free withdrawal provision, take only what's allowed each year, usually 10 percent.

There are two ways to transfer a qualified annuity: Cash out and repurchase. In this case, you would simply cash out the annuity and use the funds to purchase a new one. This is the least efficient way to do it because once you receive the funds, you're going to have to pay tax on them at an ordinary income tax rate.

There are four basic types of annuities to meet your needs: immediate fixed, immediate variable, deferred fixed, and deferred variable annuities. These four types are based on two primary factors: when you want to start receiving payments and how you would like your annuity to grow.

Variable annuities are securities regulated by the SEC. An indexed annuity may or may not be a security; however, most indexed annuities are not registered with the SEC. Fixed annuities are not securities and are not regulated by the SEC.

This includes common and preferred stocks; call and put options; bonds and other individual fixed income investments; as well as all forms of packaged products (except for those that also require a life insurance license to sell).

To give the annuity away, you simply contact the insurance company and state that you want to gift the ownership of the annuity policy to someone else or a trust. There are some tax implications to consider with this, though. Before you give an annuity away, you need to look at its status.