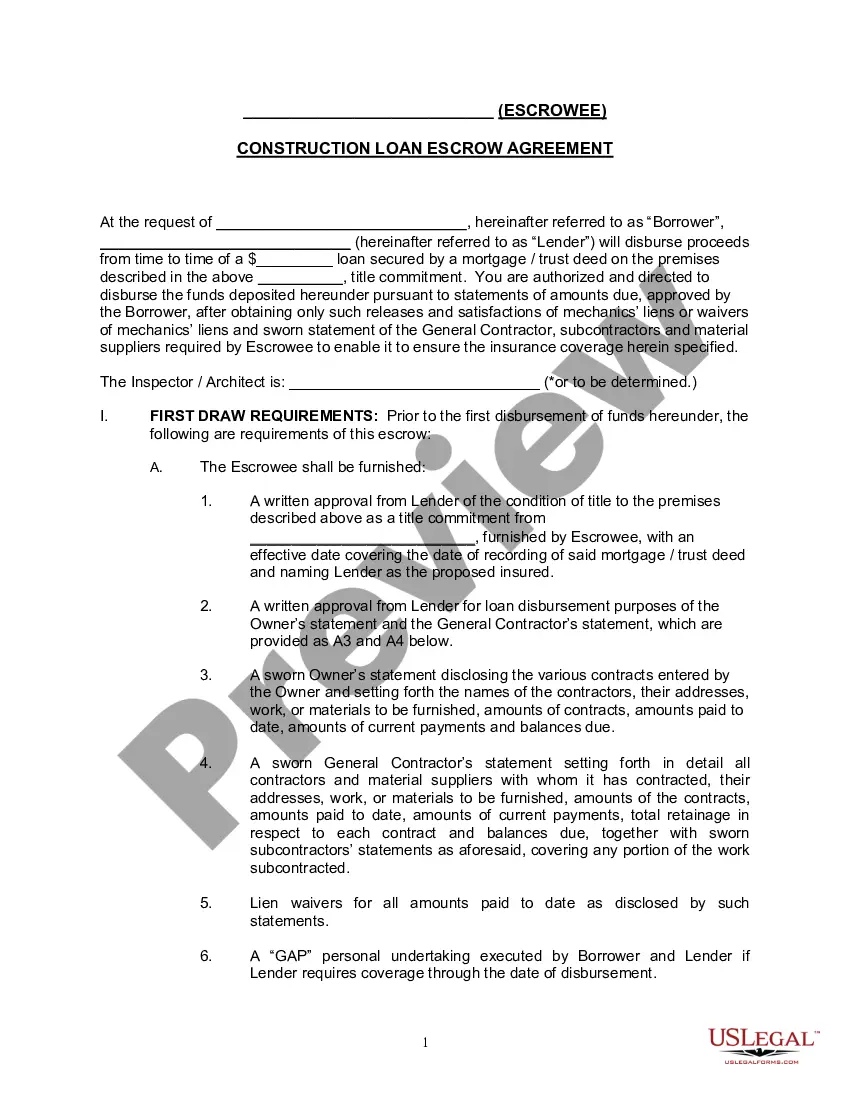

"A construction loan agreement isa legally binding contract between the lender and the borrower, detailing the promises and commitments both parties have to uphold through successful project completion.

A Loan Agreement is a document between a borrower and lender that details the loan repayment schedule.

The Loan Agreement protects the lender by enforcing the borrower's pledge to repay the loan; payment via regular payments or lump sums. The borrower may also find the loan contract useful because it records the details of the loan for their records and helps keep track of payments.

Loan agreements generally include information about:

* The location.

* The loan amount.

* Interest and late fees.

* Repayment method.

* Collateral and insurance."

Ohio Construction Loan Agreement

Category:

State:

Multi-State

Control #:

US-ENTREP-0065-1

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Construction Loan Agreement?

US Legal Forms - one of many most significant libraries of legal kinds in America - offers a variety of legal record templates you may down load or print out. While using site, you can get a large number of kinds for business and individual uses, sorted by groups, suggests, or key phrases.You can find the latest versions of kinds like the Ohio Construction Loan Agreement in seconds.

If you already have a subscription, log in and down load Ohio Construction Loan Agreement in the US Legal Forms collection. The Download key can look on each and every develop you perspective. You get access to all formerly delivered electronically kinds inside the My Forms tab of your own account.

If you want to use US Legal Forms the very first time, allow me to share basic directions to obtain started:

- Make sure you have picked the proper develop for the city/region. Click the Preview key to check the form`s articles. Look at the develop description to actually have chosen the right develop.

- In the event the develop does not satisfy your demands, use the Search area on top of the screen to obtain the one who does.

- When you are satisfied with the shape, validate your choice by clicking on the Acquire now key. Then, choose the pricing strategy you prefer and give your references to sign up to have an account.

- Process the deal. Utilize your credit card or PayPal account to accomplish the deal.

- Choose the file format and down load the shape on your own gadget.

- Make changes. Load, revise and print out and indication the delivered electronically Ohio Construction Loan Agreement.

Every design you included with your bank account lacks an expiry particular date and it is your own property for a long time. So, if you want to down load or print out yet another duplicate, just proceed to the My Forms portion and then click around the develop you want.

Gain access to the Ohio Construction Loan Agreement with US Legal Forms, by far the most comprehensive collection of legal record templates. Use a large number of specialist and state-certain templates that fulfill your small business or individual demands and demands.

Form popularity

FAQ

Construction loans typically cover the cost of the construction of the house and are converted into a traditional mortgage. Typically, home buyers only need to pay for interest during the construction period, but this will vary with the type of construction loan or mortgage you have.

An end loan is a specific type of long-term loan an individual procures to pay off a short-term construction loan or other interim financing structure. Such short-term loans are used by builders as start-up financing to launch the construction of homes or other real estate properties.

Construction Loans Compared Type of loanBest forConstruction-to-permanent loanHomeowners who want to save on closing costs and lock in mortgage financingConstruction-only loanThose who have a large amount of cash on hand or who intend to pay off the construction loan with the sale of their previous home2 more rows ?

A construction loan agreement is a legally binding contract between the lender and the borrower, detailing the promises and commitments both parties have to uphold through successful project completion.

The interest rates on construction loans are typically variable, which means that they are subject to change throughout the term of the loan. However, in general, the rates on construction loans are usually around 1 percent higher than mortgage rates.

A loan agreement should be structured to include information about the borrower and the lender, the loan amount, and repayment terms, including interest charges and a timeline for repaying the loan. It should also spell out penalties for late payments or default and should be clear about expectations between parties.

For loans by a commercial lender, the lender will provide the agreement. But for loans between friends or relatives, you will need to create your own loan agreement.

These loans are generally paid off with permanent financing using the cash flow generated by the completed building. The money borrowed through a construction loan is disbursed in a series of advances or draws ing to a prearranged schedule or milestones.