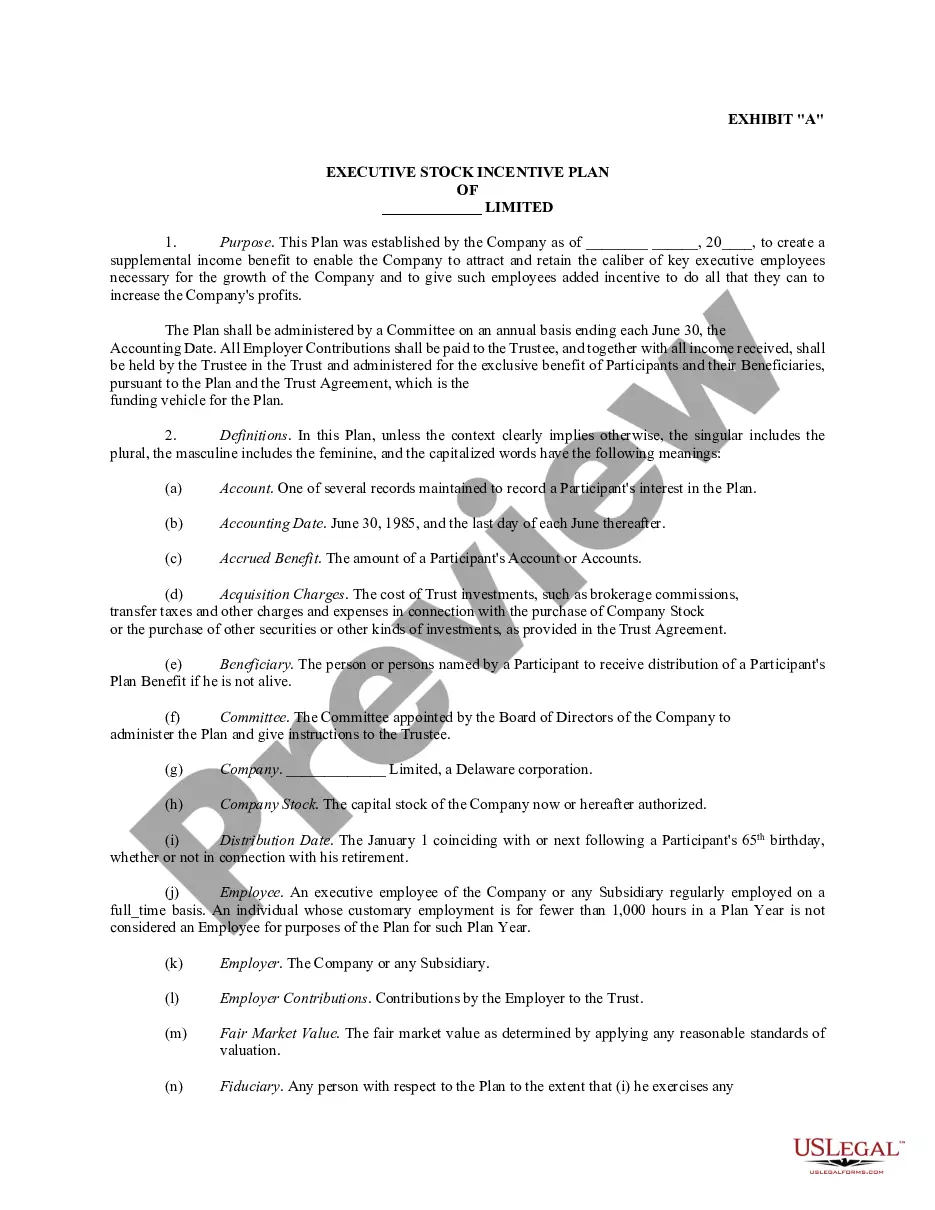

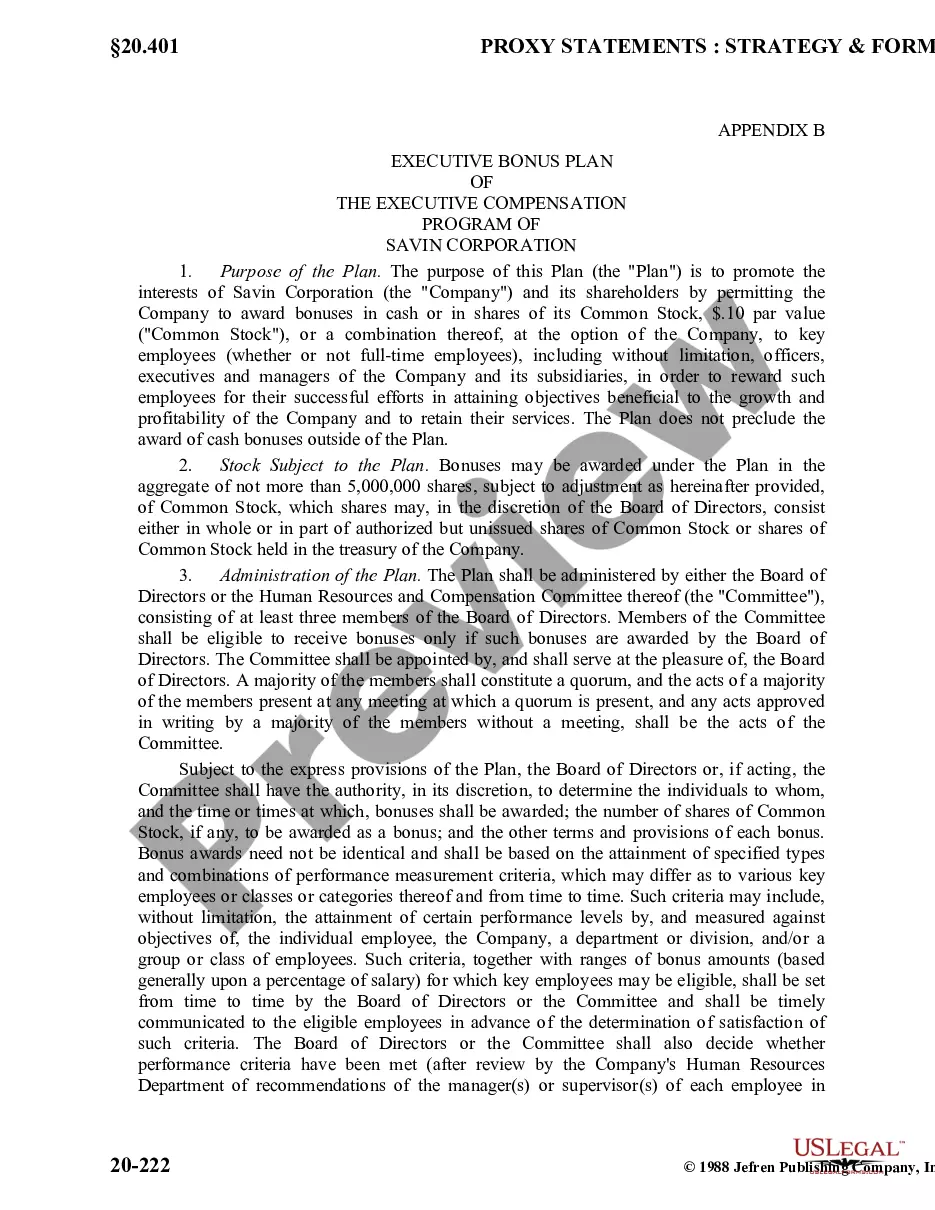

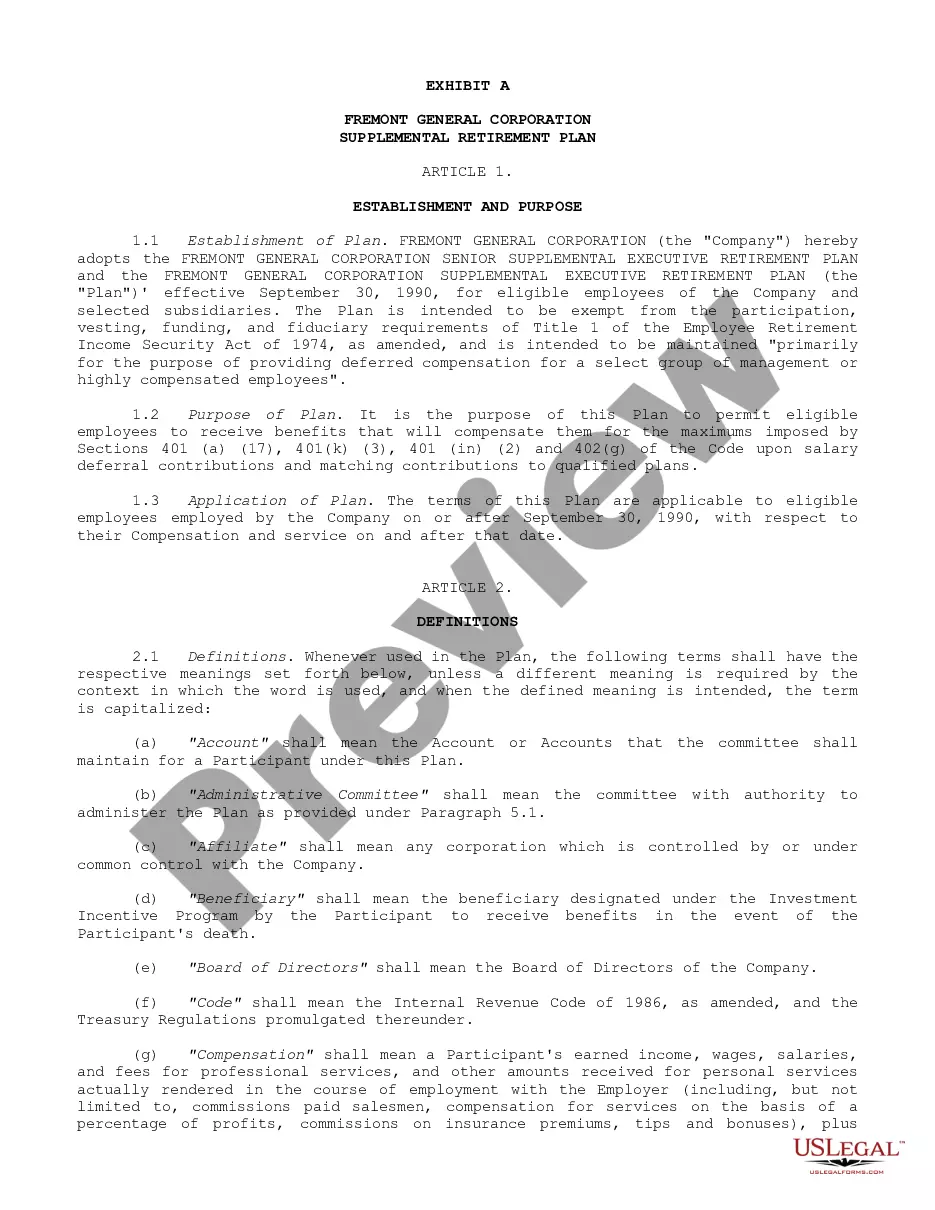

Ohio Supplemental Executive Retirement Plan - SERP

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Supplemental Executive Retirement Plan - SERP?

Are you currently in the situation the place you require documents for sometimes organization or personal functions almost every working day? There are a variety of legal record templates available on the Internet, but discovering types you can depend on isn`t straightforward. US Legal Forms provides a large number of type templates, much like the Ohio Supplemental Executive Retirement Plan - SERP, which can be written to meet federal and state requirements.

In case you are presently familiar with US Legal Forms internet site and possess a free account, simply log in. After that, you can down load the Ohio Supplemental Executive Retirement Plan - SERP design.

If you do not come with an account and wish to begin using US Legal Forms, abide by these steps:

- Find the type you will need and make sure it is for the correct town/state.

- Make use of the Preview key to analyze the form.

- Look at the description to ensure that you have selected the appropriate type.

- In case the type isn`t what you are looking for, take advantage of the Research discipline to get the type that meets your needs and requirements.

- Whenever you obtain the correct type, just click Purchase now.

- Choose the prices prepare you desire, submit the desired info to create your account, and pay money for the order with your PayPal or credit card.

- Decide on a practical data file file format and down load your version.

Discover all of the record templates you possess purchased in the My Forms menus. You can obtain a additional version of Ohio Supplemental Executive Retirement Plan - SERP any time, if required. Just click on the necessary type to down load or print out the record design.

Use US Legal Forms, one of the most extensive selection of legal forms, to save time as well as steer clear of blunders. The service provides skillfully manufactured legal record templates that can be used for a variety of functions. Generate a free account on US Legal Forms and begin making your daily life a little easier.

Form popularity

FAQ

A supplemental executive retirement plan (SERP) is a set of benefits that may be made available to top-level employees in addition to those covered in the company's standard retirement savings plan. A SERP is a form of a deferred-compensation plan. It is not a qualified plan.

The SERP differs from regular retirement plans. First of all, it's a non-qualified plan. Unlike a 401(k), it doesn't have a contribution limit or rules requiring it to be open to all employees.

Risk of forfeiture. Forfeiture can occur if the employee has not met the requirements to ?earn? or ?vest? in the future SERP payout. This usually occurs when the employee leaves the company prior to retirement. This also can happen when leaving the company prior to vesting or not achieving performance thresholds.

The funds can be withdrawn, without penalty, before you turn 59½, nor do you need to begin required minimum distributions at age 73. Although most employers require distributions to begin at retirement or when you are no longer employed. SERPs can be designed with many different options or configurations.

SERPs are paid out as either one lump sum or as a series of set payments from an annuity, with different tax implications for each method, so choose carefully.

Although SERPs could be paid out of cash flows or investment funds, most are funded through a cash value life insurance plan. The employer buys the insurance policy, pays the premiums, and has access to its cash value. The employee receives supplemental retirement income paid for through the insurance policy.

SERP withdrawals are taxed as regular income, but taxes on that income are deferred until you start making withdrawals. Much like other tax-deferred retirement plans, SERP funds grow tax-free until retirement. If you withdraw your SERP funds in a lump sum, you'll pay the taxes at all once.