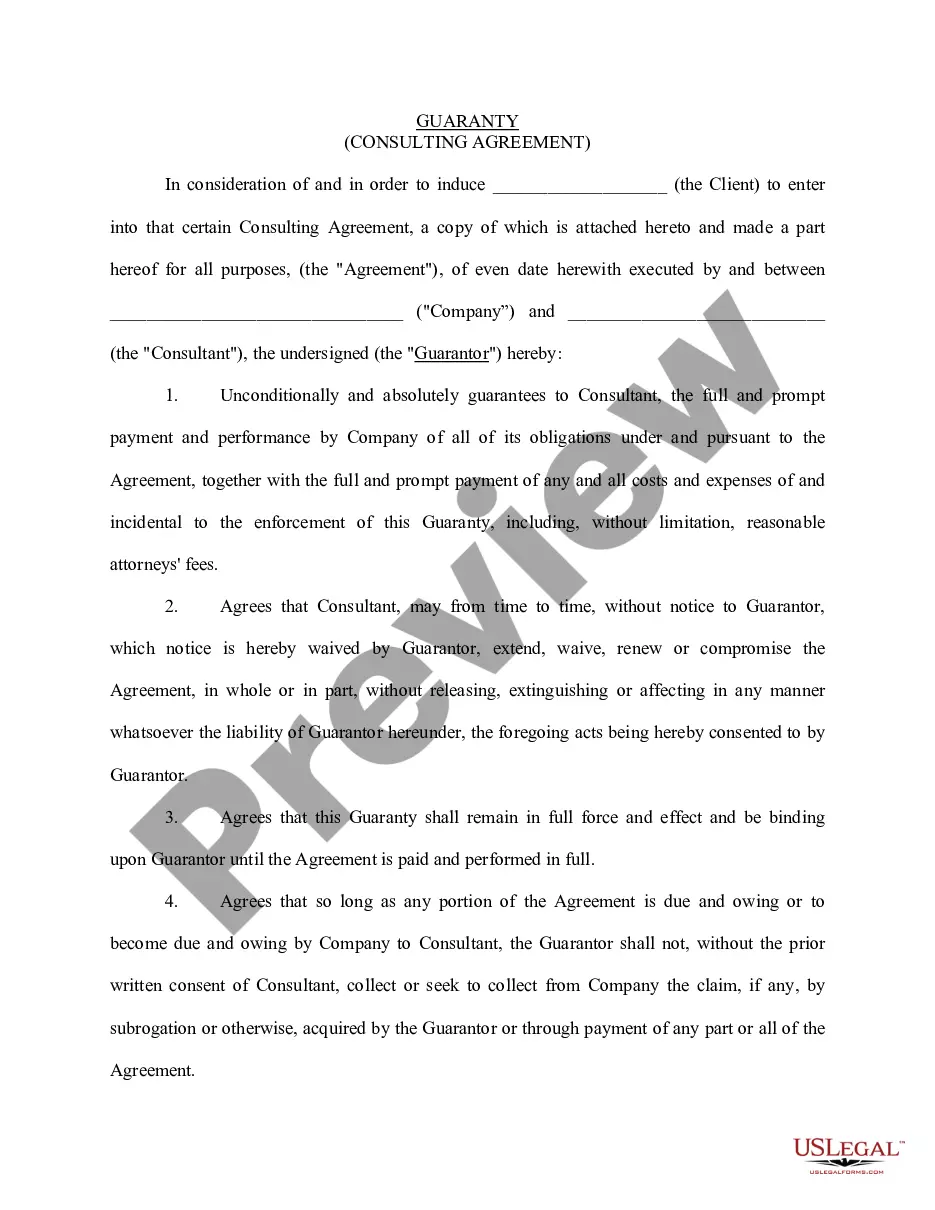

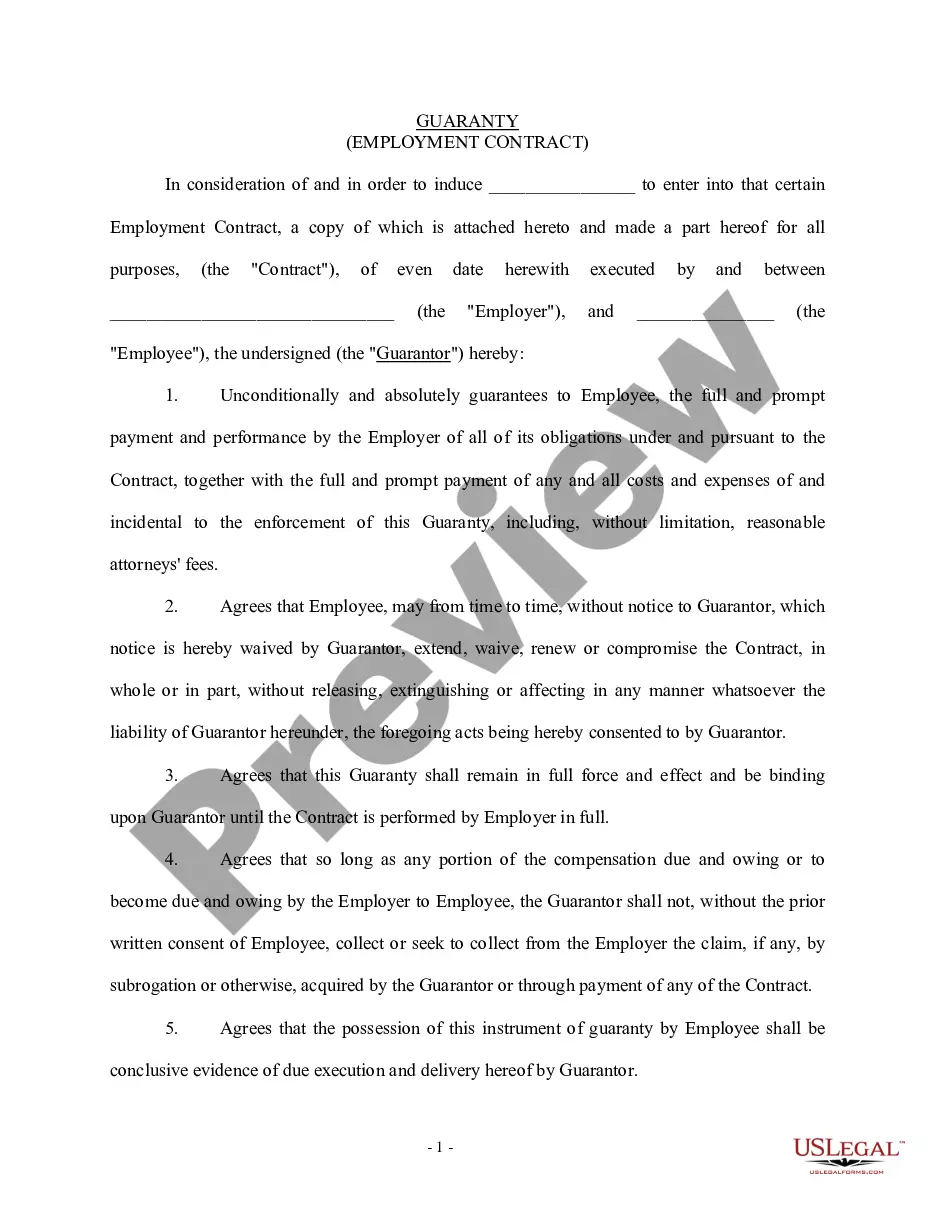

Ohio Personal Guaranty of Another Person's Agreement to Pay Consultant

Description

How to fill out Personal Guaranty Of Another Person's Agreement To Pay Consultant?

Selecting the optimal authorized document template can be a challenge. Clearly, there are numerous layouts available online, but how do you find the legal form you require? Utilize the US Legal Forms platform.

The service offers a myriad of templates, including the Ohio Personal Guaranty of Another Person's Agreement to Pay Consultant, which can be utilized for both business and personal needs. All forms are vetted by experts and comply with federal and state regulations.

If you are already registered, Log In to your account and click the Download button to obtain the Ohio Personal Guaranty of Another Person's Agreement to Pay Consultant. Use your account to explore the legal forms you have previously purchased. Navigate to the My documents section of your account and retrieve another copy of the document you require.

US Legal Forms is the largest collection of legal forms where you can find a wide variety of document templates. Use the service to obtain professionally crafted papers that adhere to state requirements.

- First, ensure you have selected the appropriate form for your locality/county. You can review the form using the Preview button and check the form description to confirm it is suitable for you.

- If the form does not meet your needs, utilize the Search field to find the correct document.

- Once you are certain that the form is appropriate, click the Buy now button to obtain the document.

- Select the payment plan you prefer and fill in the required information. Create your account and pay for your order using your PayPal account or Visa or Mastercard.

- Choose the document format and download the legal document template for your system.

- Complete, modify, print, and sign the acquired Ohio Personal Guaranty of Another Person's Agreement to Pay Consultant.

Form popularity

FAQ

In writing The guarantee must be evidenced in writing to be enforceable. Signed The document must be signed by the guarantor or their authorised agent. Their name can be written or printed. Secondary liability The document must establish that the guarantor has secondary liability for the debt.

Risks of Personal Guarantees If the business defaults on the loan, legal action could be taken against you to repay the loan balance. You could lose your personal assets. But note that some states have homestead laws, which prohibit creditors from seizing your primary residence and retirement savings accounts.

A personal guarantee can be enforced the same way as any debt. If the business owner does not pay, the creditor can bring a lawsuit to receive a judgment and levy the owner's personal assets to cover the debt. The exact terms of a personal guarantee specify a creditor's options under the guarantee.

A personal guaranty is not enforceable without consideration A contract is an enforceable promise. The enforceability of a contract comes from one party's giving of consideration to the other party. Here, the bank gives a loan (the consideration) in exchange for the guarantor's promise to repay it.

Your personal guarantee may be unenforceable due to circumstances outside of your contract. This may include being misled by the creditor, if a key fact was omitted from the contract, co-guarantor issues, suspicions of fraud, or if the facility provided by the bank changed significantly since you signed the guarantee.

When a personal guarantee is given, the principals of the company pledge their own assets and agree to repay a debt from personal capital in case the company defaults. In short, the business owner or principal becomes a cosigner on the credit application.

7 Ways to Avoid a Personal GuaranteeBuy insurance.Raise the interest rate.Increase Reporting.Increased the Frequency of Payments.Add a Fidelity Certificate.Limit the Guarantee Time Period.Use Other Collateral.

If you sign a personal guarantee, you are personally liable for the loan balance or a portion thereof. If your business later defaults on the loan, anyone who signed the personal guarantee can be held responsible for the remaining balance, even after the lender forecloses on the loan collateral.

Contracts of guarantee must be in writing For a guarantee to be enforceable, section 27(2) of the Act provides that the contract of guarantee must be: in writing; and. signed by the guarantor.