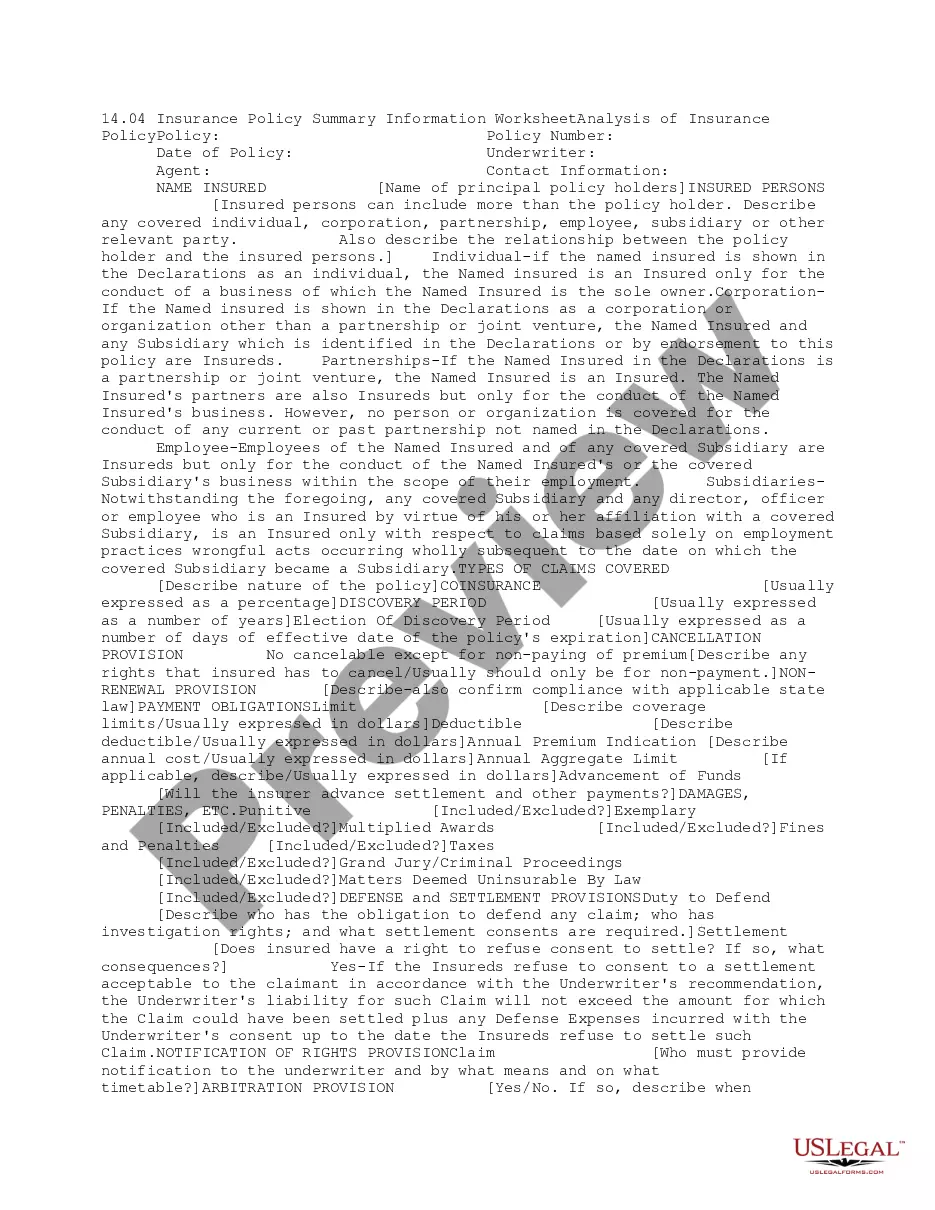

This due diligence form is a summary of insurance coverage analysis for directors and officers in a company.

Nevada Executive Summary Director and Officer Insurance Coverage Analysis

Category:

State:

Multi-State

Control #:

US-DD01409

Format:

Word;

PDF;

Rich Text

Instant download

Description

How to fill out Executive Summary Director And Officer Insurance Coverage Analysis?

If you wish to obtain, download, or print legal document templates, utilize US Legal Forms, the largest selection of legal forms available online.

Take advantage of the website's straightforward and user-friendly search feature to locate the documents you require.

A range of templates for business and personal use are organized by categories and regions, or keywords.

Step 4. Once you have found the form you need, click on the Get now button. Choose the pricing plan you prefer and enter your credentials to register for the account.

Step 5. Complete the transaction. You may use your credit card or PayPal account to finalize the payment.

- Utilize US Legal Forms to locate the Nevada Executive Summary Director and Officer Insurance Coverage Analysis in just a few clicks.

- If you are currently a US Legal Forms subscriber, Log Into your account and click the Download button to access the Nevada Executive Summary Director and Officer Insurance Coverage Analysis.

- You can also access forms you previously downloaded in the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the instructions listed below.

- Step 1. Ensure you have selected the form for the correct area/state.

- Step 2. Use the Review option to examine the contents of the form. Don’t forget to read the description.

- Step 3. If you are not satisfied with the form, utilize the Search field at the top of the screen to find alternative versions of the legal form template.

Form popularity

FAQ

A Directors and Officers (D&O) policy typically covers legal fees and settlements resulting from wrongful acts in managing a company. This includes issues like mismanagement or breach of fiduciary duty, which are essential aspects of the Nevada Executive Summary Director and Officer Insurance Coverage Analysis. Additionally, the policy may also cover claims related to employment practices, such as discrimination or harassment. Understanding your coverage options can provide significant protection for company leaders.

The main difference between Directors' and Officers' insurance and Professional indemnity insurance is that Directors and Officers insurance is aimed to provide financial assistance should DIRECTORS and senior OFFICERS of your business named in legal actions which will require legal costs to be covered should a claim

Key Takeaways. Directors and officers (D&O) liability insurance covers directors and officers or their company or organization if sued (most policies exclude fraud and criminal offenses). D&O insurance claims are paid to cover losses associated with the lawsuit, including legal defense fees.

Directors and officers (D&O) liability insurance protects the personal assets of corporate directors and officers, and their spouses, in the event they are personally sued by employees, vendors, competitors, investors, customers, or other parties, for actual or alleged wrongful acts in managing a company.

Directors and officers (D&O) liability insurance protects the personal assets of corporate directors and officers, and their spouses, in the event they are personally sued by employees, vendors, competitors, investors, customers, or other parties, for actual or alleged wrongful acts in managing a company.

Directors and officers (D&O) liability insurance protects the personal assets of corporate directors and officers, and their spouses, in the event they are personally sued by employees, vendors, competitors, investors, customers, or other parties, for actual or alleged wrongful acts in managing a company.

D&O policies include an exclusion for losses related to criminal or deliberately fraudulent activities. Additionally, if an individual insured receives illegal profits or remuneration to which they were not legally entitled, they will not be covered if a lawsuit is brought forward due to this.

Directors and Officers InsuranceD&O is there to protect high-level decision makers when someone asserts they were negligent in their duties as an officer or board member. E&O, on the other hand, covers acts, errors, and omissions committed by employees of the company.

D&O insurance specifically covers members on a board of directors and officers. Professional liability insurance, on the other hand, covers professionals (of nearly any position within a company) that offer specialized services.

The following are several examples of Management Liability (D&O) claims.Misrepresentation. Directors and officers at a company failed to disclose material facts and provided inaccurate and misleading information to their investors.Credit Fraud.Stolen Corporate Secrets.Recruiting Sales Executives.Investment Agreement.