The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use.

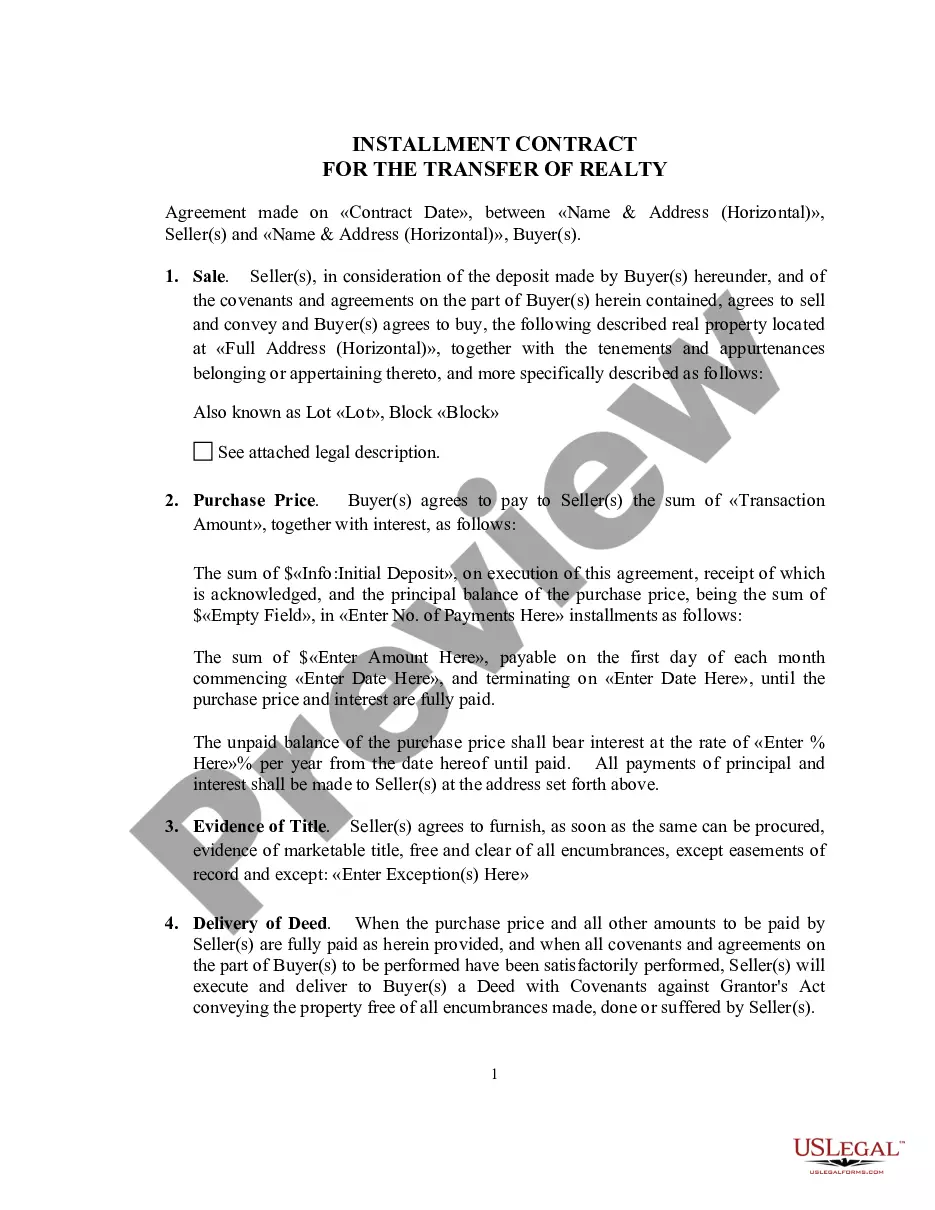

Closed-end transactions involve a fixed amount to be paid back over a period of time such as a note or a retail installment contract.

New Mexico General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures

Category:

State:

Multi-State

Control #:

US-02514BG

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

How to fill out General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures?

US Legal Forms - one of the largest collections of legal documents in the United States - provides a variety of legal form templates that you can download or print. By using the website, you can discover thousands of forms for business and personal purposes, organized by categories, states, or keywords.

You can obtain the most current versions of forms such as the New Mexico General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures in just seconds.

If you already have a subscription, Log In and download the New Mexico General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures from your US Legal Forms library. The Download button will be visible on each form you review. You can access all previously downloaded forms in the My documents section of your account.

Make modifications. Complete, edit, print, and sign the downloaded New Mexico General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

Every template added to your account has no expiration date and is yours permanently. Therefore, to download or print another version, simply navigate to the My documents section and click on the form you wish to access.

- To use US Legal Forms for the first time, here are simple steps to get started.

- Ensure you have selected the correct form for your city/county. Click on the Review button to check the form's details. Read the form information to confirm that you've selected the right one.

- If the form does not meet your needs, utilize the Search field at the top of the screen to find the appropriate one.

- If you are satisfied with the form, confirm your selection by clicking the Buy now button. Then, choose the payment plan you prefer and provide your credentials to register for an account.

- Process the transaction. Use a Visa or Mastercard or PayPal account to complete the transaction.

- Select the format and download the form to your device.

Form popularity

FAQ

A Truth in Lending statement is required whenever a consumer applies for short-term or long-term credit as defined by the New Mexico General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures. This typically applies to transactions involving loans or credit sales where the financing is extended. Understanding when this statement is necessary helps ensure compliance with legal obligations. For detailed guidance, consider leveraging resources available through uslegalforms.

The Truth in Lending Act mandates various disclosures intended to inform consumers about the costs of credit under the New Mexico General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures. Key information includes the APR, total finance charges, repayment terms, and any potential penalties. These disclosures protect consumers by promoting knowledgeable borrowing decisions. Proper compliance is crucial for lenders to avoid costly penalties and ensure fair lending practices.

The Truth in Lending Act primarily targets consumer credit, which means it generally does not apply to transactions conducted by businesses. However, there are specific circumstances under the New Mexico General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures where commercial entities might need to abide by certain disclosure requirements. Understanding these nuances is critical for business owners involved in lending or credit transactions. Proper guidance can help navigate your business compliance effectively.

Violations of the Truth in Lending Act commonly include failing to disclose required information, providing misleading terms, and not delivering the disclosures in a clear manner. Such infractions undermine consumer trust and financial education. By adhering to the New Mexico General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, lenders can maintain compliance and support consumer rights effectively.

Credit card companies must disclose several critical details under the Truth in Lending Act. These include the APR for purchases, the grace period, the balance calculation method, fees for late payments, and transaction fees. Such transparency meets the New Mexico General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, making sure you know what to expect with your credit account.

The TILA-RESPA disclosure rule integrates the requirements of the Truth in Lending Act with the Real Estate Settlement Procedures Act for real estate transactions. This rule mandates the use of a Closing Disclosure form that combines essential information and outlines closing costs. By simplifying the disclosure process, it aims to enhance clarity for borrowers in New Mexico who are engaging in retail installment contracts.

Yes, disclosures are a fundamental aspect of TILA. They are required for various types of credit transactions, ensuring that consumers receive critical information before making financial commitments. In line with the New Mexico general disclosures required by the Federal Truth in Lending Act, lenders must provide this information through retail installment contracts and closed-end disclosures.

The enforcement of TILA requirements falls under the jurisdiction of the Consumer Financial Protection Bureau (CFPB). This federal agency ensures that lenders comply with TILA's mandated disclosures and practices. Consequently, borrowers in New Mexico can feel confident that these regulations are upheld, protecting their rights in financial transactions.

When it comes to credit cards, the New Mexico General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures necessitates that issuers provide detailed information about terms and fees. This includes the APR, fees for late payments, and how interest is calculated. Understanding these details can help cardholders manage their credit usage effectively. Ultimately, this transparency fosters healthier financial habits.