This is an official form from the Supreme Court State of New Mexico, which complies with all applicable laws and statutes. USLF amends and updates the forms as is required by New Mexico statutes and law.

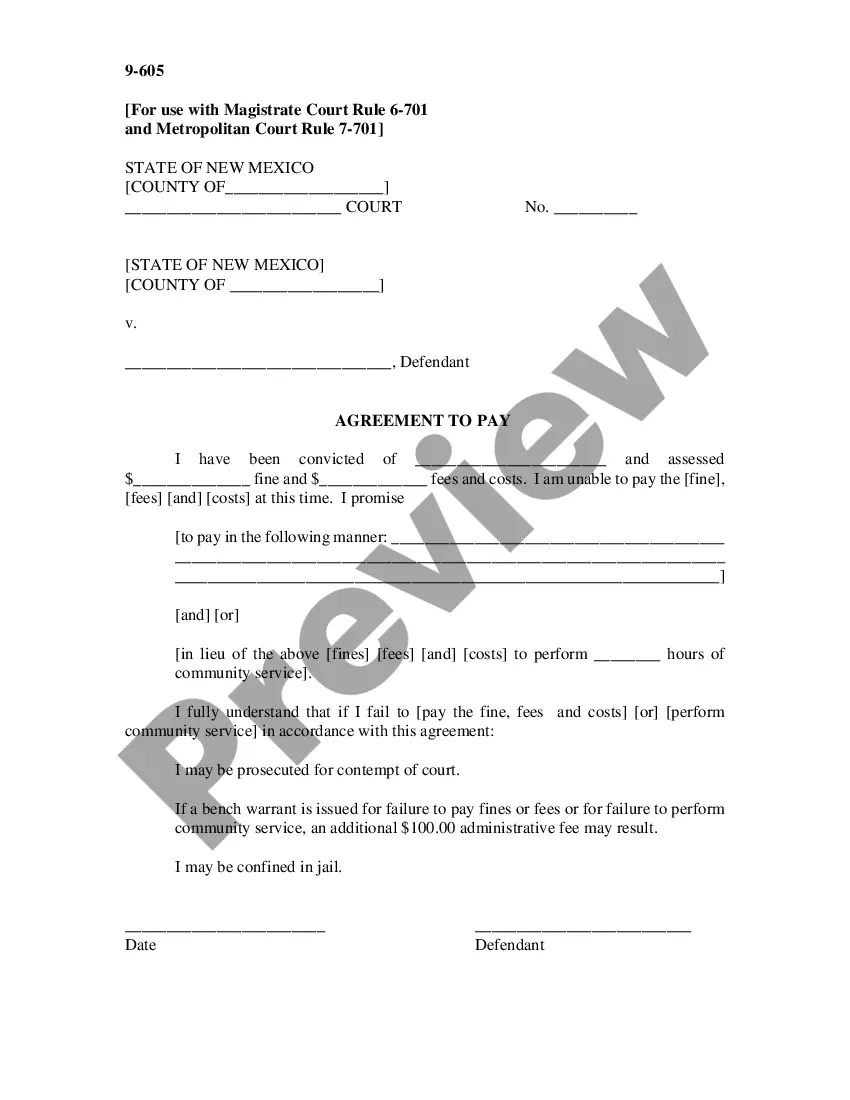

New Mexico Agreement to Pay - Municipal

Instant download

This website is not affiliated with any governmental entity

Public form

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out New Mexico Agreement To Pay - Municipal?

US Legal Forms is a unique system to find any legal or tax document for filling out, such as New Mexico Agreement to Pay - Municipal. If you’re fed up with wasting time looking for suitable examples and spending money on file preparation/attorney charges, then US Legal Forms is precisely what you’re searching for.

To experience all the service’s benefits, you don't have to download any application but simply choose a subscription plan and create an account. If you already have one, just log in and get the right sample, download it, and fill it out. Downloaded files are stored in the My Forms folder.

If you don't have a subscription but need New Mexico Agreement to Pay - Municipal, check out the recommendations listed below:

- make sure that the form you’re taking a look at applies in the state you need it in.

- Preview the example and read its description.

- Click on Buy Now button to get to the sign up webpage.

- Choose a pricing plan and carry on signing up by entering some information.

- Decide on a payment method to complete the sign up.

- Download the document by selecting the preferred format (.docx or .pdf)

Now, submit the file online or print it. If you are uncertain regarding your New Mexico Agreement to Pay - Municipal template, contact a lawyer to check it before you decide to send out or file it. Get started hassle-free!

Form popularity

FAQ

The compensating tax is imposed at a rate of 5.125% on certain property used in New Mexico and 5% on certain services used in New Mexico.

Typically the first half tax payment is due November 10 and becomes delinquent if not paid by December 10 (each year.) The second half is due April 10 and becomes delinquent after May 10 (each year).

DELINQUENT TAXES The notice will inform the owner that if the taxes on real property, including penalty and interest charges, are not paid within two years from the date of delinquency; the property will be sold at state public auction.

Use this number to report and pay state and local option gross receipts tax, New Mexico withholding tax and compensating tax under the Combined Reporting System (CRS). Known as a CRS Identification Number, it is used to report and pay tax collected on gross receipts from business conducted in New Mexico.

If all of a business's receipts are exempt, the business doesn't have to register with the state for GRT purposes. Common exemptions are receipts of a 501(c)(3) nonprofit and governmental entities, receipts from isolated or occasional sales, employee wages, interest and dividends and insurance company receipts.

In New Mexico, the seller pays the tax on the sales price of a product or service even if the seller doesn't collect it from the buyer and even if the buyer lives out of state. GRT was intended to widen the tax base by taxing more items at a lower rate than would be typical in states with a sales tax.

New Mexico residents are subject to the state's personal income tax. Additionally, the personal income tax applies to nonresidents who work in the state or derive income from property there.Personal income tax rates for New Mexico range from 1.7% to 4.9%, within four income brackets.

Generally speaking, sales and leases of goods and other property, both tangible and intangible, are taxable. Unlike many other states, sales and performances of most services are taxable in New Mexico.