New Jersey Assignment of Life Insurance as Collateral

Description

How to fill out Assignment Of Life Insurance As Collateral?

Choosing the best lawful document format can be quite a have difficulties. Of course, there are plenty of web templates available on the net, but how would you discover the lawful kind you require? Take advantage of the US Legal Forms internet site. The support provides a huge number of web templates, like the New Jersey Assignment of Life Insurance as Collateral, that you can use for company and personal requirements. All of the forms are inspected by pros and meet up with state and federal requirements.

In case you are presently authorized, log in for your profile and then click the Download switch to obtain the New Jersey Assignment of Life Insurance as Collateral. Make use of your profile to check with the lawful forms you possess acquired formerly. Go to the My Forms tab of the profile and obtain one more backup from the document you require.

In case you are a brand new consumer of US Legal Forms, listed here are easy recommendations that you should stick to:

- Initially, be sure you have selected the proper kind for your personal metropolis/county. It is possible to look through the shape utilizing the Preview switch and browse the shape outline to make sure this is the best for you.

- When the kind fails to meet up with your requirements, take advantage of the Seach field to discover the right kind.

- When you are positive that the shape is suitable, go through the Buy now switch to obtain the kind.

- Pick the costs strategy you would like and type in the needed details. Design your profile and pay for the order utilizing your PayPal profile or credit card.

- Pick the data file format and down load the lawful document format for your gadget.

- Complete, revise and produce and signal the obtained New Jersey Assignment of Life Insurance as Collateral.

US Legal Forms will be the greatest catalogue of lawful forms in which you can find various document web templates. Take advantage of the company to down load professionally-made papers that stick to condition requirements.

Form popularity

FAQ

Every case is different, and the amounts different companies offer vary. However, ing to the Life Insurance Settlement Association (LISA), the average life settlement is 20% of the policy's face value. That means if your policy has a $100,000 benefit, you might receive $20,000 from selling it.

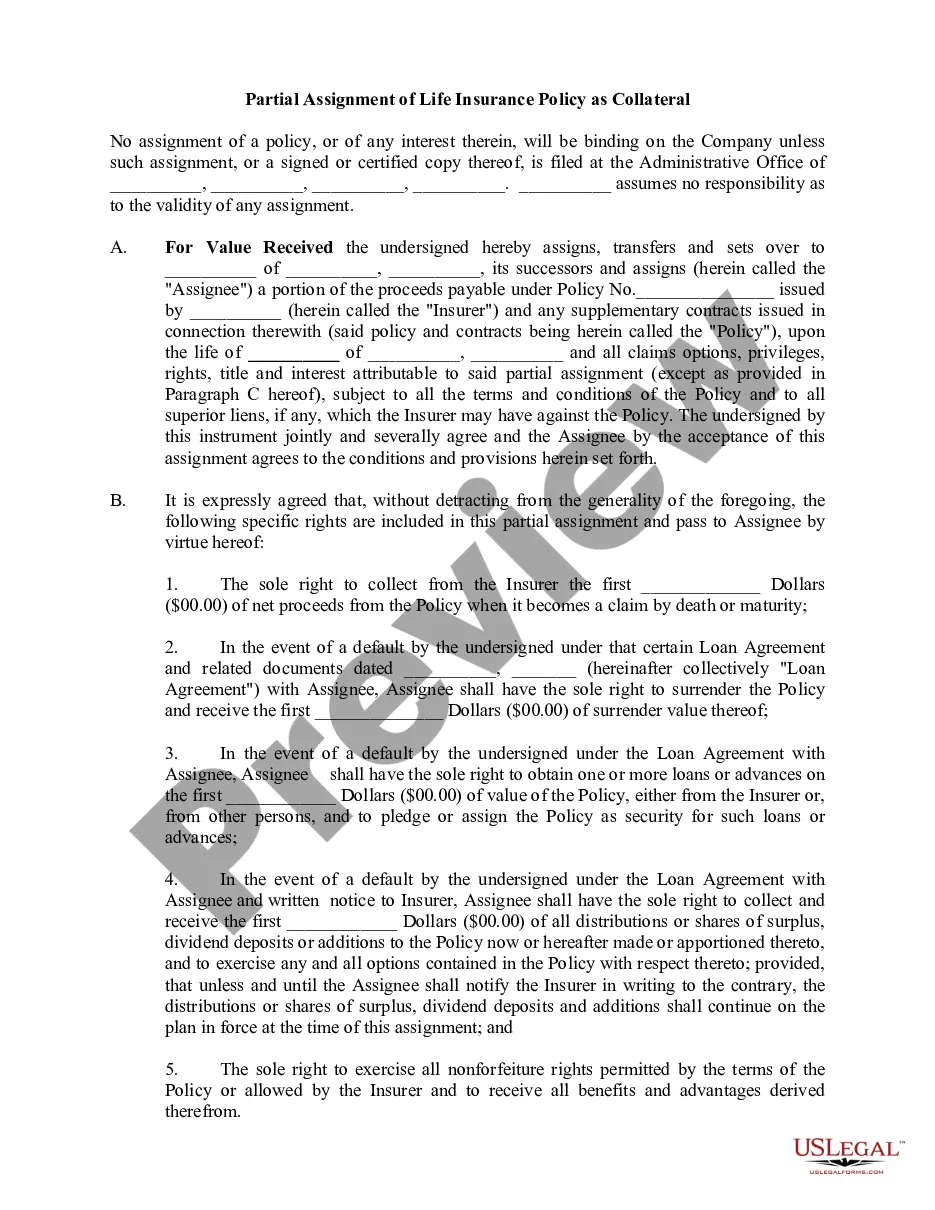

The collateral assignment is irrevocable as established by a written agreement preventing the holder of the life insurance policy from affecting or using the cash surrender value after the irrevocable assignment.

You can usually withdraw part of the cash value in a permanent life policy without canceling the coverage. Instead, your life insurance beneficiaries will receive a reduced payout when you die. Typically you won't owe income tax on withdrawals up to the amount of the premiums you've paid into the policy.

How fast does cash value build in life insurance? Most permanent life insurance policies begin to accrue cash value in 2 to 5 years. However, it can take decades to see significant cash value accumulation.

A collateral assignment of life insurance directs your insurance provider to use your death benefit to pay off an existing loan if you die while in debt. After the lender is paid, any remaining funds go to your policy's beneficiaries.

A collateral assignment of life insurance is a conditional assignment appointing a lender as an assignee of a policy. Essentially, the lender has a claim to some or all of the death benefit until the loan is repaid. The death benefit is used as collateral for a loan.

The limit for borrowing money from life insurance is set by the insurer, and it's typically no more than 90% of the policy's cash value. When your policy has enough cash value (minimums vary by insurer), you can use it as collateral to request a loan from your insurance company.

You can borrow from a life insurance policy as soon as there is enough cash value built up to take a loan in the amount you need. Depending on how your policy is structured, this can take several years to accrue.