New Jersey Proposal to adopt plan of dissolution and liquidation

Description

How to fill out Proposal To Adopt Plan Of Dissolution And Liquidation?

It is possible to invest time on-line trying to find the legitimate file format that meets the state and federal needs you require. US Legal Forms provides a huge number of legitimate forms that are examined by specialists. You can actually obtain or produce the New Jersey Proposal to adopt plan of dissolution and liquidation from your service.

If you already possess a US Legal Forms profile, it is possible to log in and click the Download button. Next, it is possible to comprehensive, revise, produce, or indication the New Jersey Proposal to adopt plan of dissolution and liquidation. Each legitimate file format you buy is your own for a long time. To obtain another version for any purchased form, visit the My Forms tab and click the corresponding button.

If you work with the US Legal Forms website initially, adhere to the simple instructions under:

- Initial, make certain you have chosen the correct file format to the county/town of your liking. Look at the form outline to make sure you have picked the proper form. If accessible, take advantage of the Preview button to appear with the file format too.

- If you would like find another version of your form, take advantage of the Look for industry to obtain the format that suits you and needs.

- Once you have identified the format you need, simply click Get now to continue.

- Select the pricing plan you need, type in your credentials, and sign up for your account on US Legal Forms.

- Complete the financial transaction. You may use your Visa or Mastercard or PayPal profile to cover the legitimate form.

- Select the formatting of your file and obtain it in your system.

- Make changes in your file if possible. It is possible to comprehensive, revise and indication and produce New Jersey Proposal to adopt plan of dissolution and liquidation.

Download and produce a huge number of file templates using the US Legal Forms web site, which provides the greatest collection of legitimate forms. Use skilled and express-distinct templates to take on your company or individual requirements.

Form popularity

FAQ

Section 331(a)(1) states the general rule that amounts dis- tributed in complete liquidation of a corporation shall be treated as payments to the shareholder in exchange for his stock.

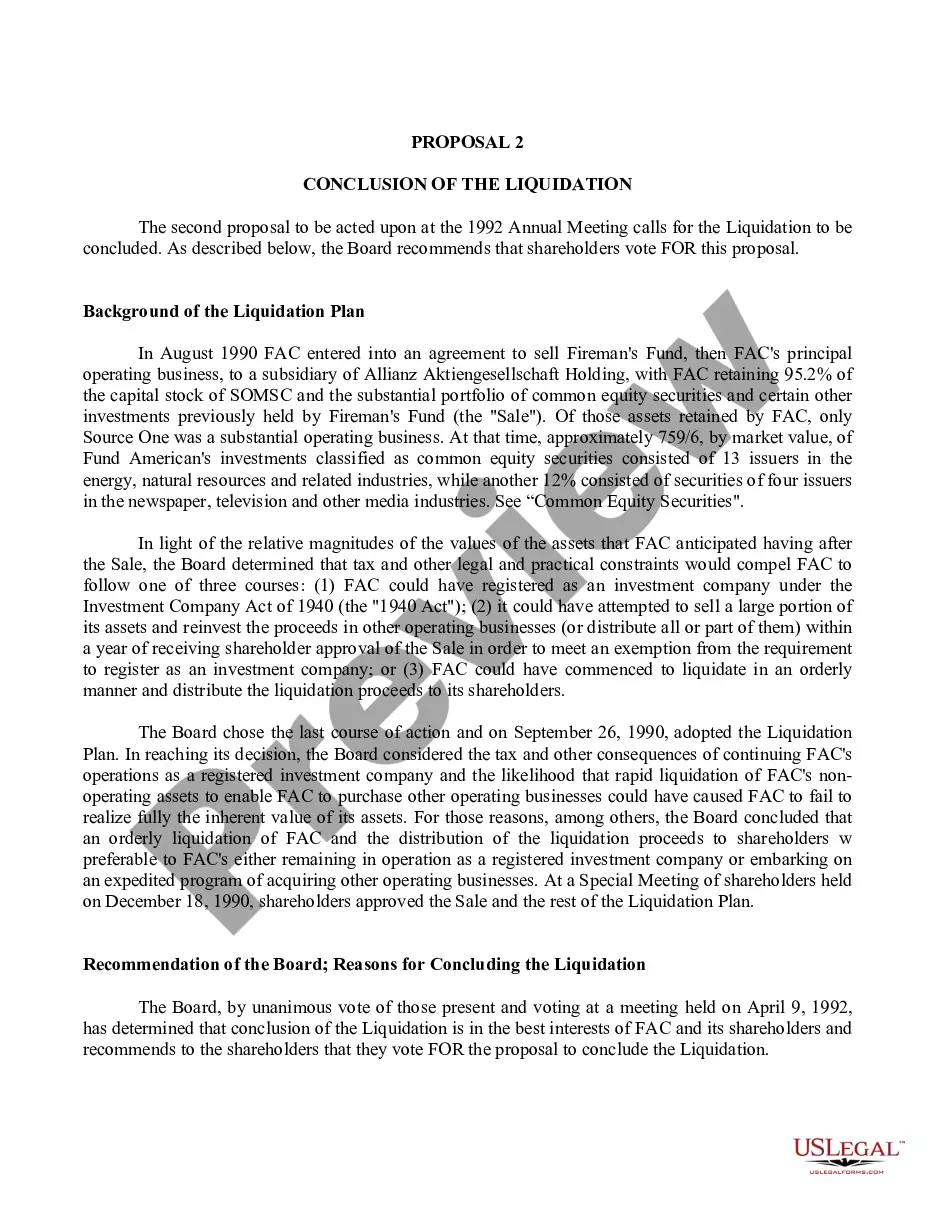

Dissolution, or the process of dissolving a company, will occur after a liquidation as the business must be struck off the Companies House register. This can only happen once the assets have been sold and distributed amongst creditors and shareholders.

In contrast to Code §331, Code §332 provides that no gain or loss is recognized by a corporation that is a shareholder upon complete liquidation of a subsidiary, provided that certain conditions are met.

IRC 731(a)(2). For liquidating distributions, gain is recognized to the extent money (or deemed money) distributed exceeds the partner's outside basis; loss is recognized to the extent the partner's outside basis exceeds money distributed and the basis of any hot assets distributed.

IRC §331 provides rules for the tax treatment of shareholders receiving distributions in a complete liquidation of a corporation. In a complete liquidation, a corporation usually distributes all of its assets to the shareholders in exchange for all of its stock pursuant to a plan of a complete liquidation.

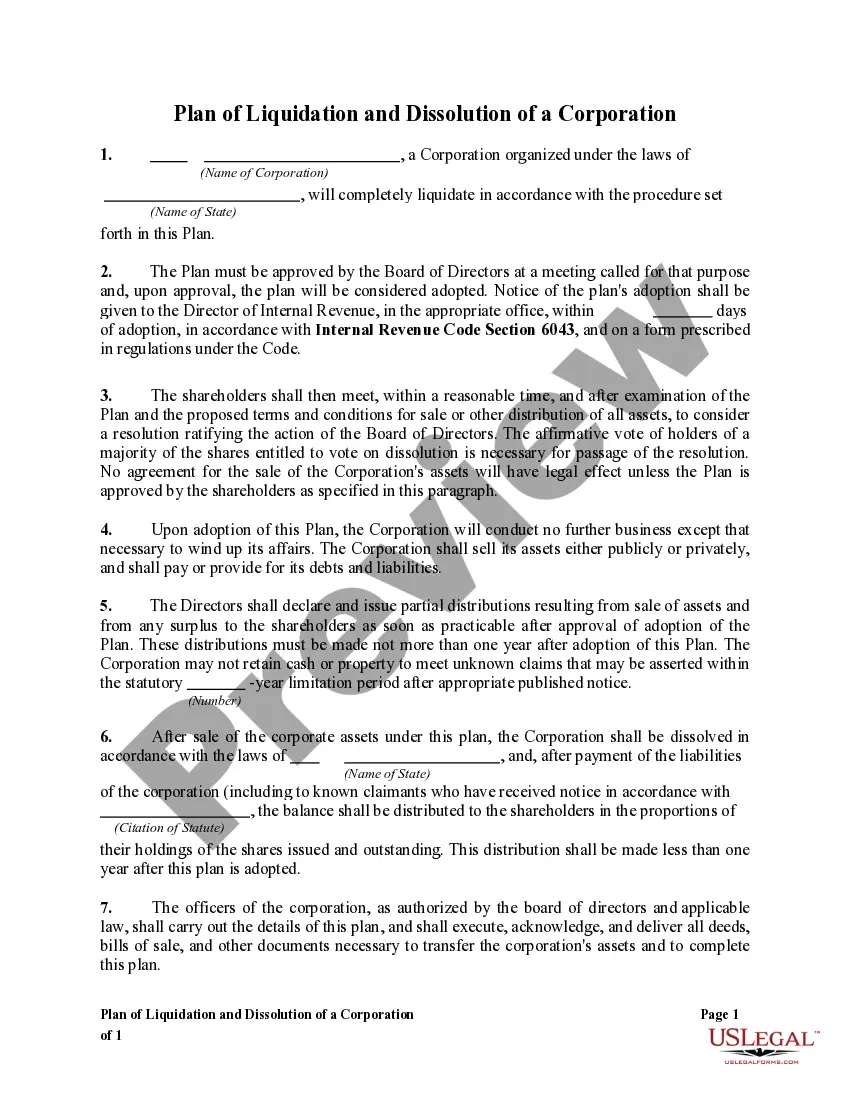

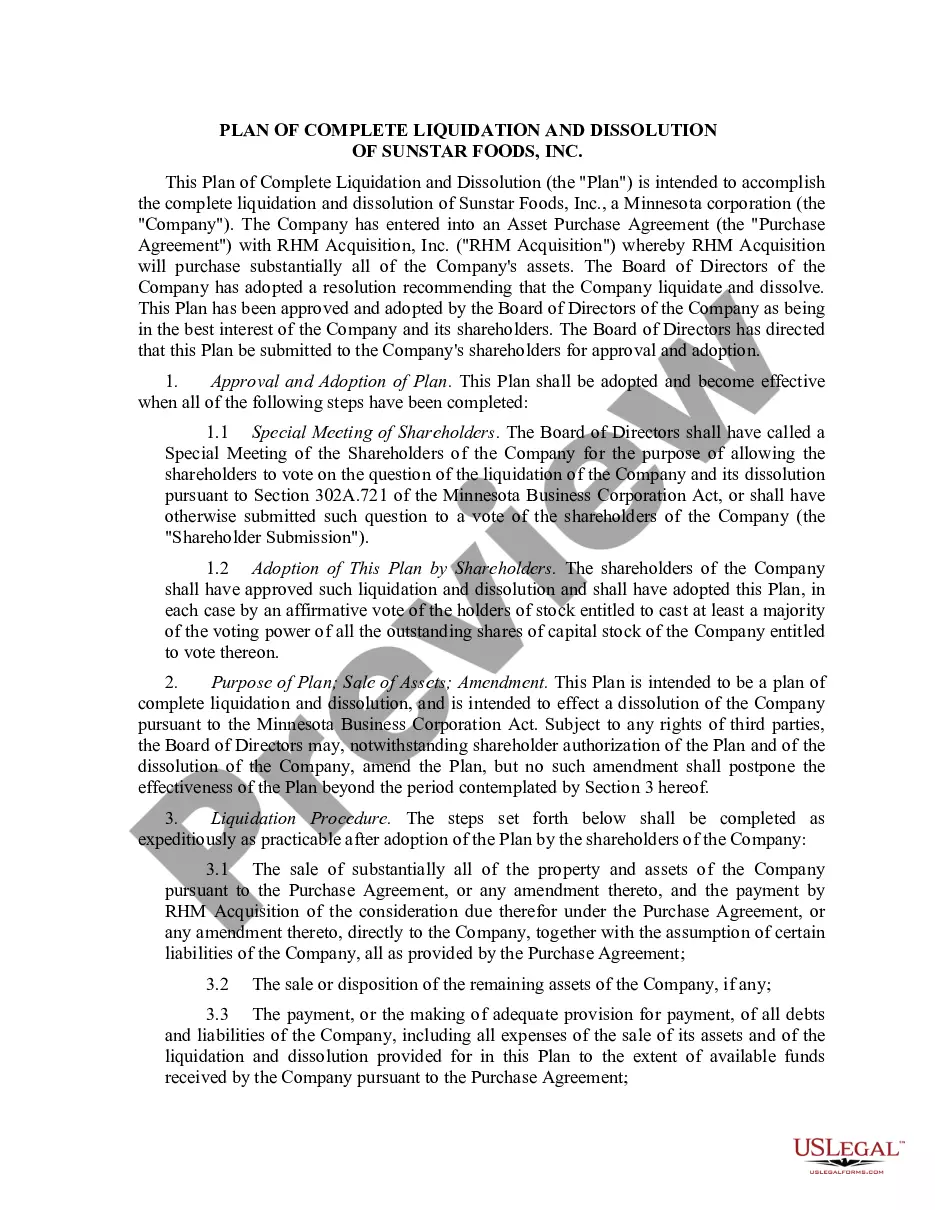

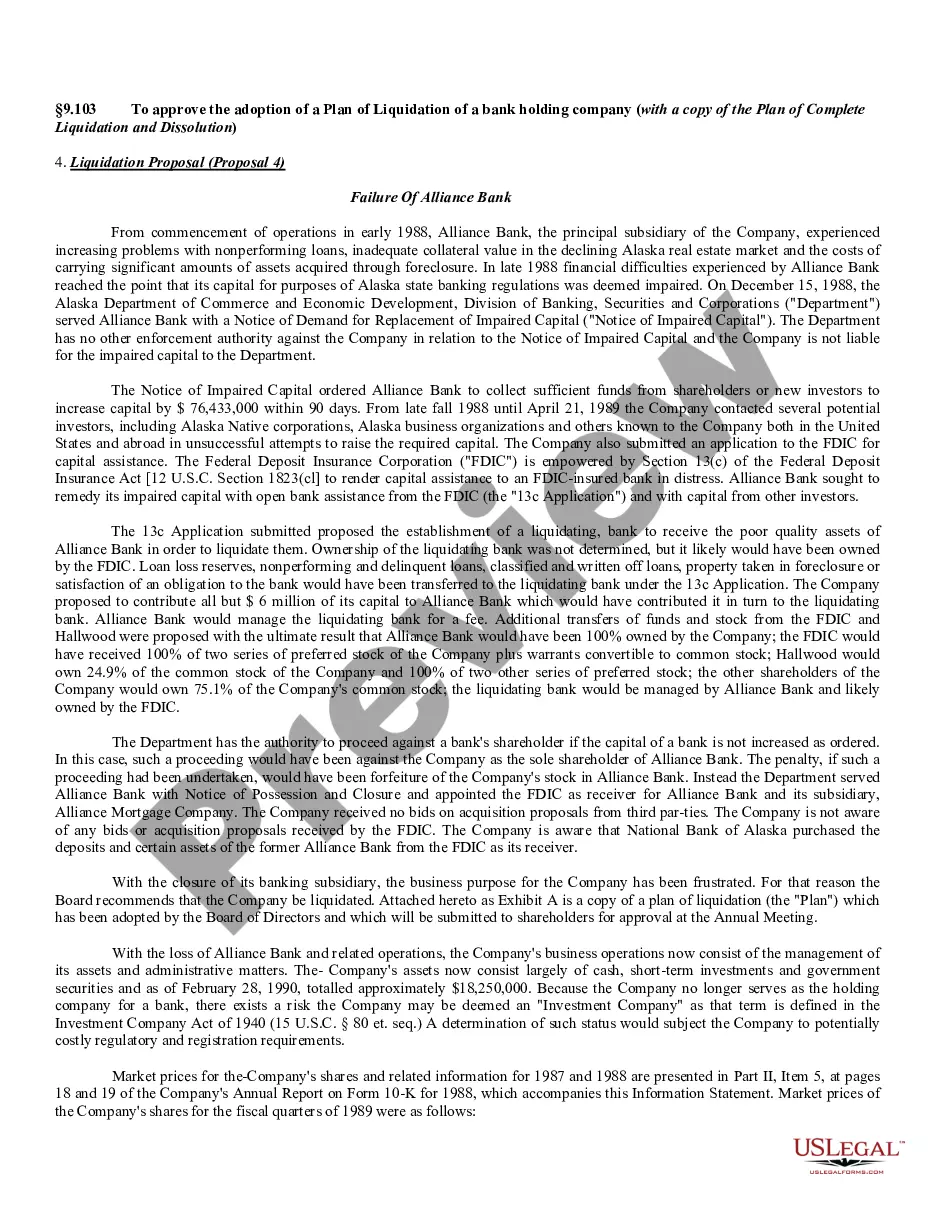

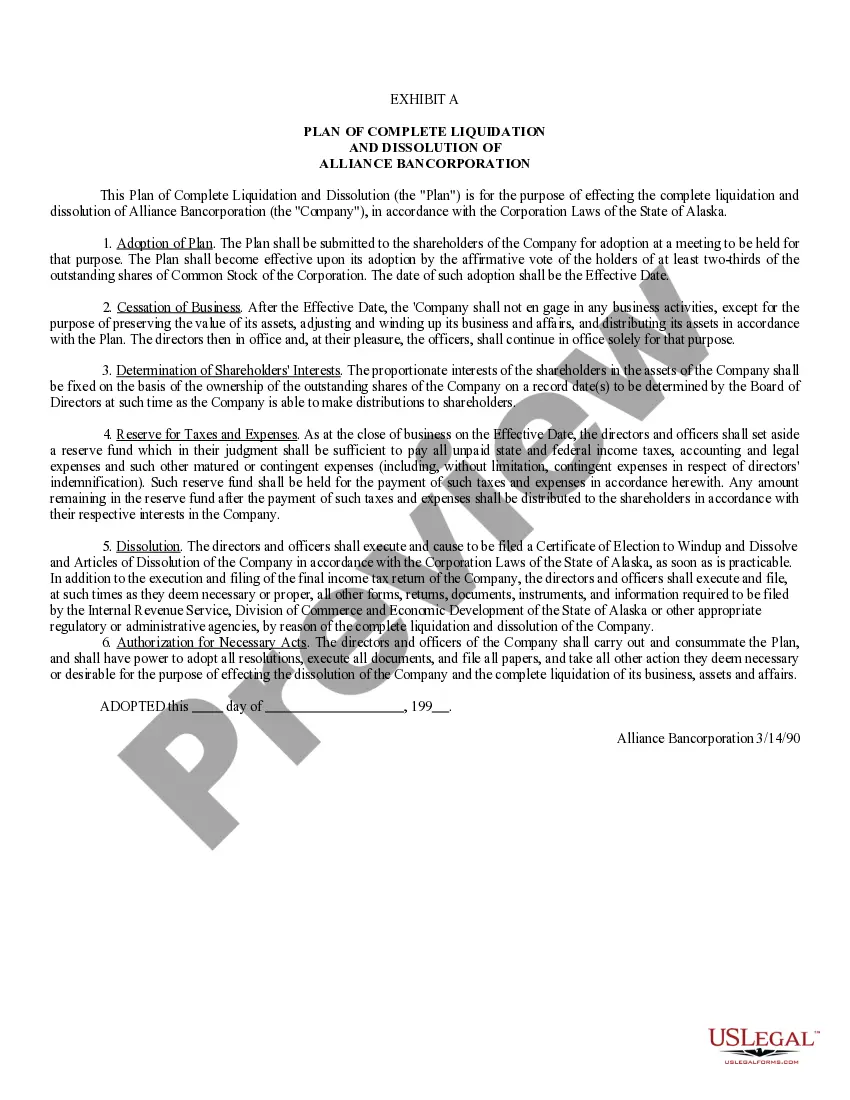

A plan for dissolving a New Jersey for-profit corporation. This document can be used as a standalone plan or incorporated into board or shareholders' resolutions. This Standard Document has integrated notes with important explanations and drafting and negotiating tips.

A plan of dissolution is a written description of how an entity intends to dissolve, or officially and formally close the business. A plan of dissolution will include a description of how any remaining assets and liabilities will be distributed.

IRC §331 provides rules for the tax treatment of shareholders receiving distributions in a complete liquidation of a corporation. In a complete liquidation, a corporation usually distributes all of its assets to the shareholders in exchange for all of its stock pursuant to a plan of a complete liquidation.