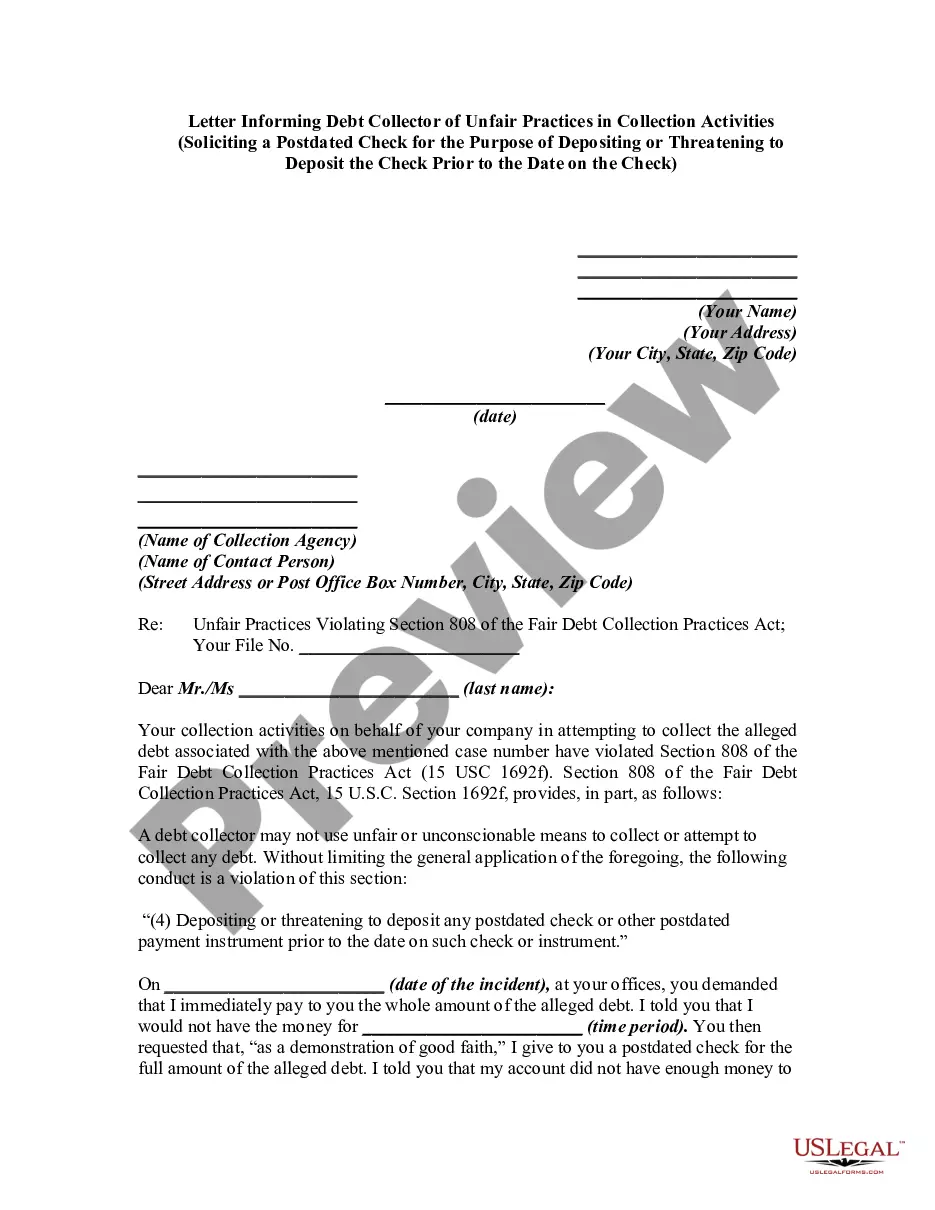

A debt collector may not use unfair or unconscionable means to collect a debt. This includes depositing a postdated check prior to the date on the check.

New Hampshire Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check

Category:

State:

Multi-State

Control #:

US-DCPA-43

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Notice To Debt Collector - Depositing A Postdated Check Prior To The Date On The Check?

US Legal Forms - one of the most prominent collections of legal documents in the United States - provides a vast array of legal document templates that you can download or print. By utilizing the website, you will obtain numerous forms for business and personal purposes, categorized by groups, claims, or keywords.

You can find the latest versions of forms such as the New Hampshire Notice to Debt Collector - Submitting a Postdated Check Before the Date on the Check within moments.

If you hold a monthly subscription, Log In and download New Hampshire Notice to Debt Collector - Submitting a Postdated Check Before the Date on the Check from your US Legal Forms library. The Get button will be visible on every form you view. You gain access to all previously downloaded forms from the My documents section of your account.

Make modifications. Fill out, edit, print, and sign the downloaded New Hampshire Notice to Debt Collector - Submitting a Postdated Check Before the Date on the Check.

Every template saved in your account has no expiration date and is yours permanently. Thus, if you wish to download or print another copy, simply go to the My documents section and click on the form you need. Access the New Hampshire Notice to Debt Collector - Submitting a Postdated Check Before the Date on the Check with US Legal Forms, one of the most extensive collections of legal document templates. Utilize a vast selection of professional and state-specific templates that meet your business or personal needs and specifications.

- To start using US Legal Forms for the first time, here are simple steps to help you get started.

- Ensure you have selected the correct form for your city/county. Click the Preview button to review the form's content. Read the form description to confirm you have selected the correct form.

- If the form does not meet your needs, use the Search field at the top of the screen to find one that does.

- If you are satisfied with the form, confirm your choice by clicking on the Get now button. Then, select your desired pricing plan and enter your details to register for the account.

- Process the payment. Use your credit card or PayPal account to complete the transaction.

- Choose the file format and download the form to your device.

Form popularity

FAQ

If the bank does not spot that the cheque has been post-dated, the cheque would then probably be paid before you intended or returned unpaid if you have insufficient funds in your account. This could potentially incur you charges and cause inconvenience to the recipient.

Federal law restricts what a debt collector can and cannot do with your postdated check. Specifically, under the Fair Debt Collection Practices Act (FDCPA), a debt collector cannot: coerce you into making a postdated payment by threatening or instituting criminal prosecution.

Among the insider tips, Ulzheimer shared with the audience was this: if you are being pursued by debt collectors, you can stop them from calling you ever again by telling them '11-word phrase'. This simple idea was later advertised as an '11-word phrase to stop debt collectors'.

Your credit card debt, auto loans, medical bills, student loans, mortgage, and other household debts are covered under the FDCPA.

Postdating a check is done by writing a check for a future date instead of the actual date the check was written. This is typically done with the intention that the check recipient will not cash or deposit the check until the future indicated date.

The Fair Debt Collection Practices Act (FDCPA) The FDCPA prohibits debt collection companies from using abusive, unfair or deceptive practices to collect debts from you.

Generally, state law provides that if you notified your bank or credit union about a post-dated check a reasonable time before it received the check, your notice is valid for six months. During that time, the bank or credit union should not cash the check before the date you wrote on the check.

Deceptive And Unfair Practices Calling you collect so that you have to pay to accept the call is an example of an unfair practice. Engaging in any practice that forces you to pay additional money other than the debt you owe is considered an FDCPA violation.

From a criminal law perspective, there is nothing inherently illegal about postdating a check, says Eric Hintz, a criminal defense attorney in Sacramento, California. Hintz says that only criminal intent, such as intentionally not having enough money for a payment, can be grounds for check fraud.

7 Most Common FDCPA ViolationsContinued attempts to collect debt not owed.Illegal or unethical communication tactics.Disclosure verification of debt.Taking or threatening illegal action.False statements or false representation.Improper contact or sharing of info.Excessive phone calls.