New Hampshire Owner Financing Contract for Moblie Home

Description

How to fill out Owner Financing Contract For Moblie Home?

US Legal Forms - one of the largest collections of legal documents in the USA - offers a selection of legal template documents that you can download or print.

By using the website, you will find thousands of forms for business and personal purposes, categorized by types, states, or keywords. You can access the latest forms like the New Hampshire Owner Financing Contract for Mobile Home in just minutes.

If you have a monthly subscription, Log In and download the New Hampshire Owner Financing Contract for Mobile Home from your US Legal Forms library. The Download button will appear on each form you view.

Once you are satisfied with the form, confirm your choice by clicking the Buy now button. Then, choose the pricing plan you prefer and provide your information to register for an account.

Complete the transaction. Use your credit card or PayPal account to finalize the payment. Find the format and download the form onto your device. Make changes. Fill out, modify, and print the downloaded New Hampshire Owner Financing Contract for Mobile Home.

Every template you add to your account does not have an expiration date and belongs to you permanently. Therefore, if you wish to download or print another copy, simply go to the My documents section and click on the form you need.

Access the New Hampshire Owner Financing Contract for Mobile Home with US Legal Forms, one of the most extensive collections of legal document templates. Utilize thousands of professional and state-specific templates that meet your business or personal needs.

- You have access to all previously downloaded forms in the My documents section of your account.

- If you are using US Legal Forms for the first time, here are easy steps to get started.

- Ensure you have selected the right form for your region/area.

- Click the Preview button to review the form's content.

- Read the form description to confirm you have selected the correct form.

- If the form does not meet your requirements, utilize the Search area at the top of the screen to find one that does.

Form popularity

FAQ

When looking into a New Hampshire Owner Financing Contract for Mobile Home, it's essential to understand credit requirements. Generally, a credit score of 580 or higher is preferred for owner financing options. However, some sellers may consider lower scores depending on other factors like income and payment history. Make sure to review your credit report and address any issues before seeking financing.

Obtaining financing for a manufactured home can be challenging, mainly due to stricter lending requirements and appraisal issues. Traditional lenders often require higher credit scores and larger down payments for manufactured homes. Fortunately, seeking a New Hampshire Owner Financing Contract for Mobile Home can streamline the process. This option may offer you more lenient terms and a smoother path to financing your new home.

Banks may hesitate to finance mobile homes due to concerns about their resale value and depreciation. Additionally, mobile homes can be classified as personal property rather than real estate, complicating financing options. The New Hampshire Owner Financing Contract for Mobile Home serves as an effective alternative. It allows buyers to bypass traditional banking hurdles and secure the necessary funding more easily.

Most banks finance mobile homes that are built after 1976, as this is when the HUD code for manufactured homes was enacted. Homes built before this date may not meet modern safety standards, leading to financing difficulties. However, utilizing a New Hampshire Owner Financing Contract for Mobile Home can provide an alternative to traditional bank loans. This option can help you secure financing for older mobile homes that banks may overlook.

Financing a mobile home can be more challenging than financing a traditional home. This difficulty often stems from the perceived lower value and the depreciation of mobile homes. However, the New Hampshire Owner Financing Contract for Mobile Home offers flexible terms that can simplify the financing process. It provides a more accessible pathway for buyers who may struggle with conventional lending.

In a typical owner financing scenario, the seller retains the deed until the buyer fulfills the payment terms outlined in the New Hampshire Owner Financing Contract for Mobile Home. This arrangement protects the seller while the buyer builds equity. Once the final payment is made, the seller transfers the deed to the buyer, completing the transaction.

Typically, lenders will finance mobile homes built after 1976, as they must meet safety and construction standards set by the HUD. If you are considering a New Hampshire Owner Financing Contract for Mobile Home, ensure the home complies with any local regulations. Owner financing may provide more flexibility regarding the age of the mobile home compared to traditional loans.

Generally, a credit score of 580 or higher is considered acceptable for financing a mobile home. However, some lenders may accept lower scores if other financial aspects are strong. When entering into a New Hampshire Owner Financing Contract for Mobile Home, credit checks may not be necessary, depending on your agreement, making it easier for buyers with less-than-perfect credit.

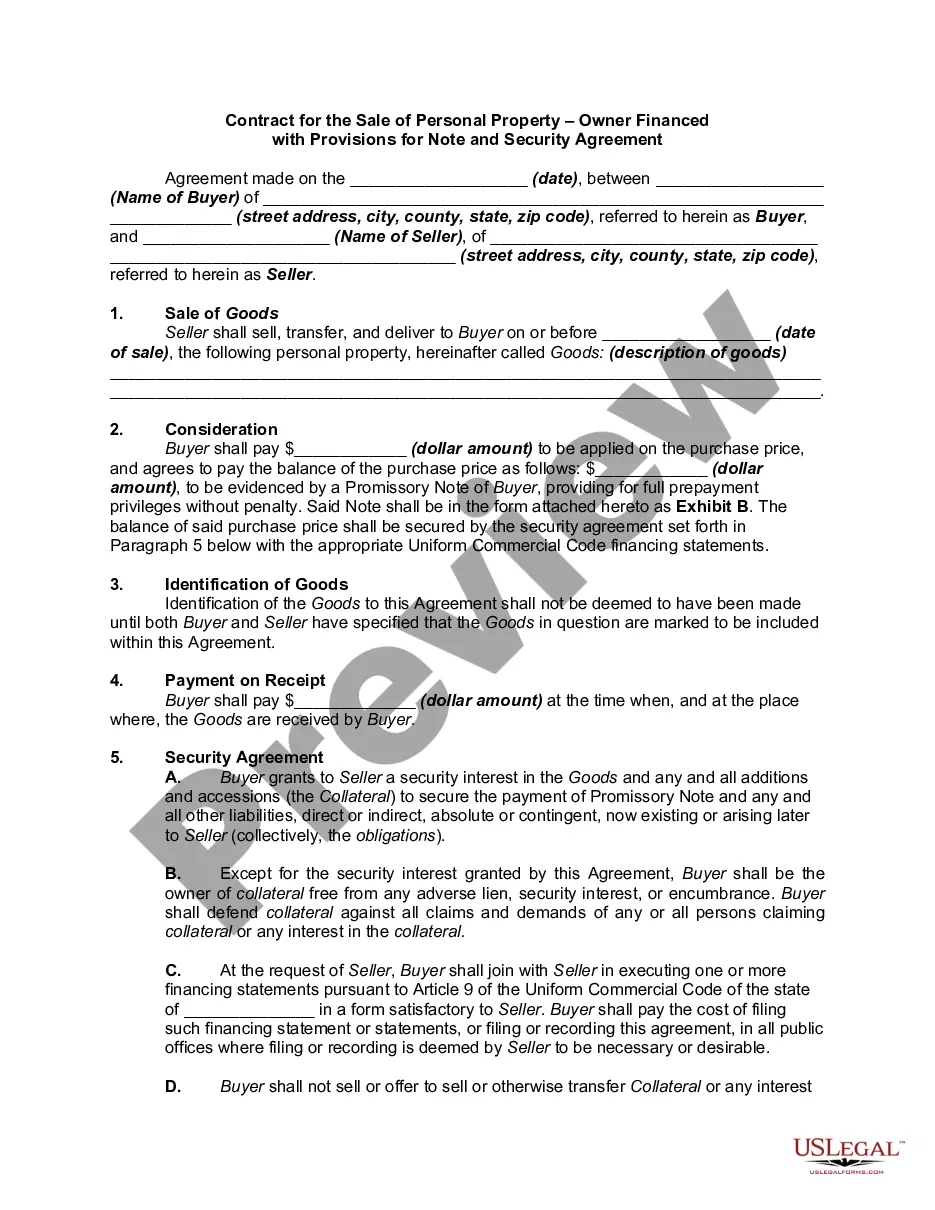

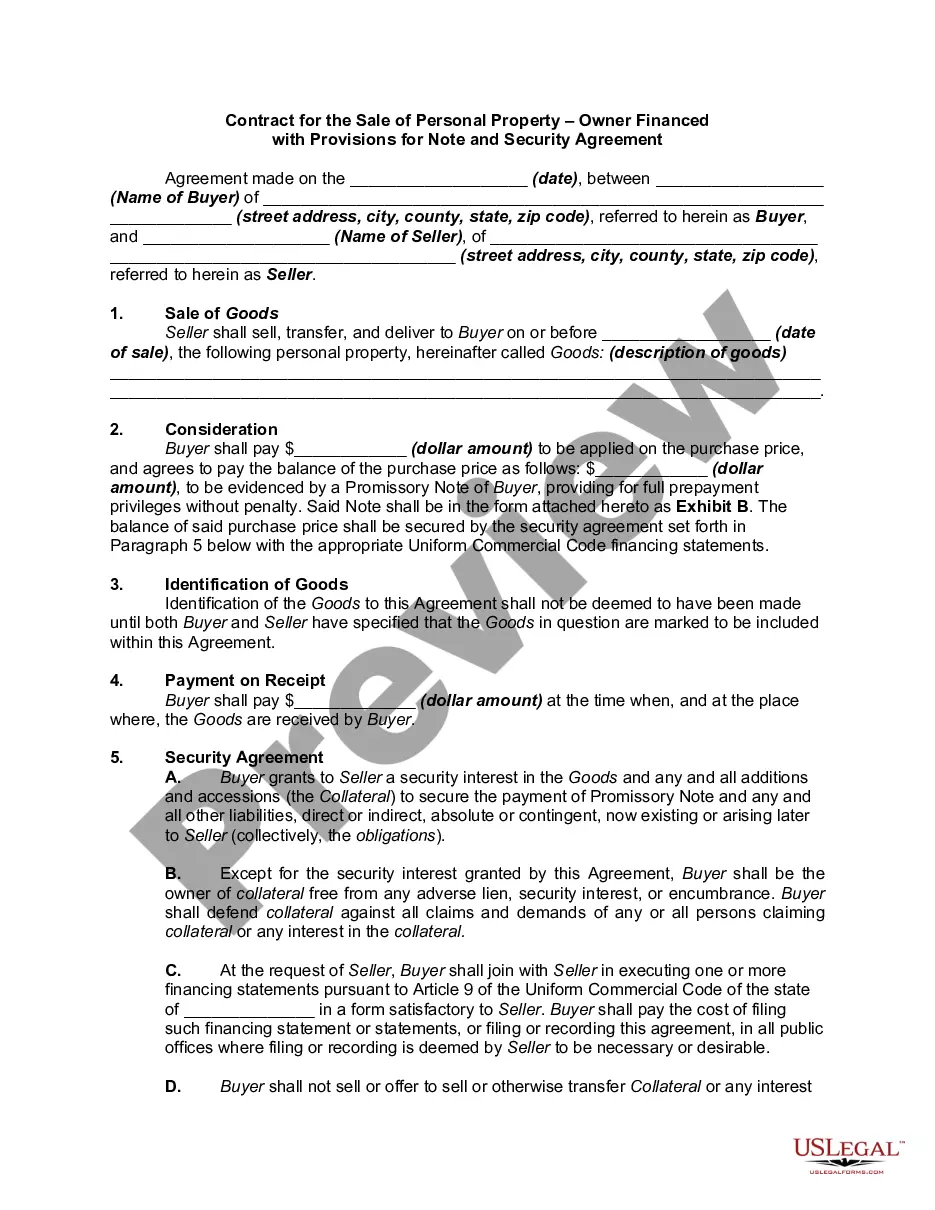

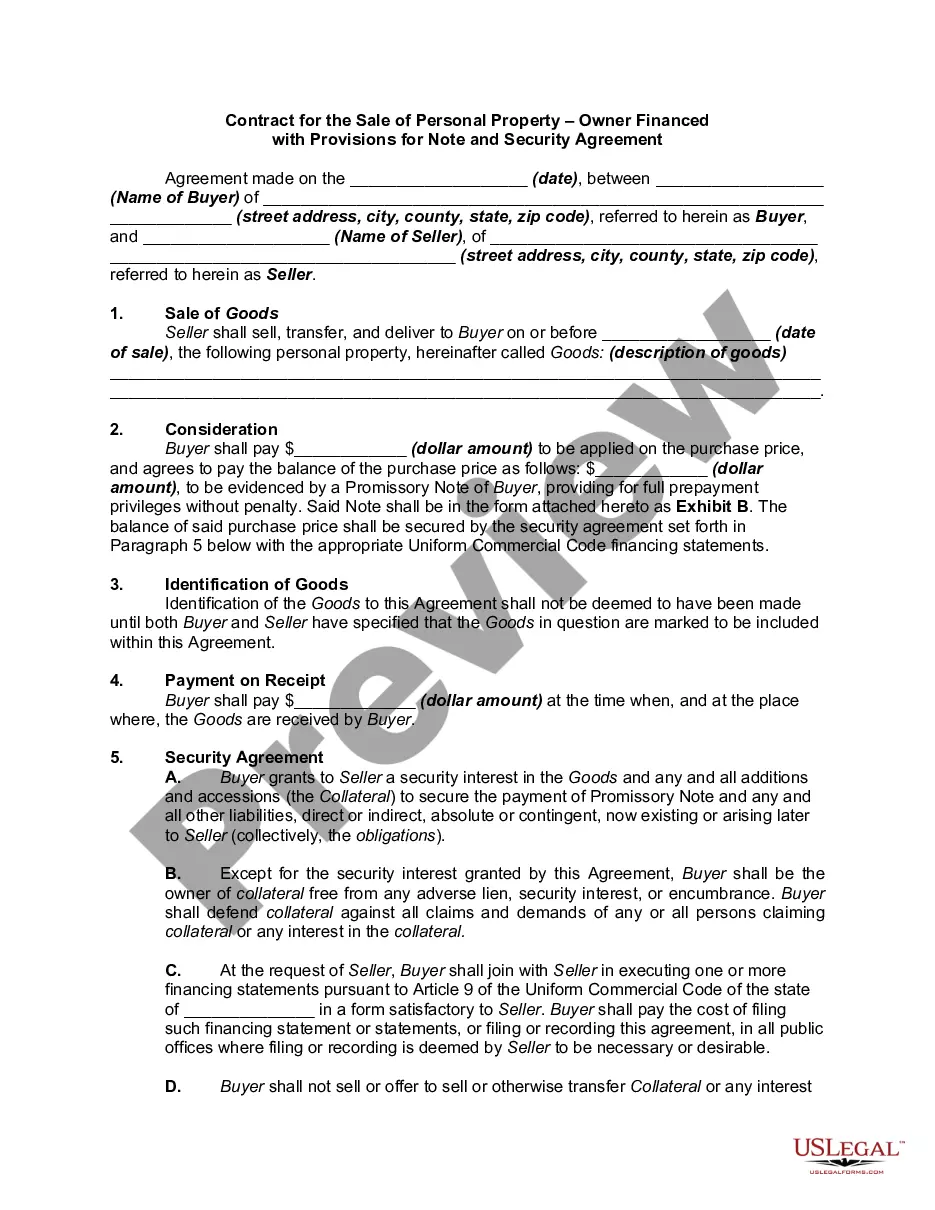

Setting up an owner financing contract begins with drafting a written agreement between you and the buyer, outlining payment terms, interest rates, and the length of the contract. You can use resources from US Legal Forms to create a legally binding document specific to the New Hampshire Owner Financing Contract for Mobile Home. Ensure both parties review the terms thoroughly before signing to avoid misunderstandings later.