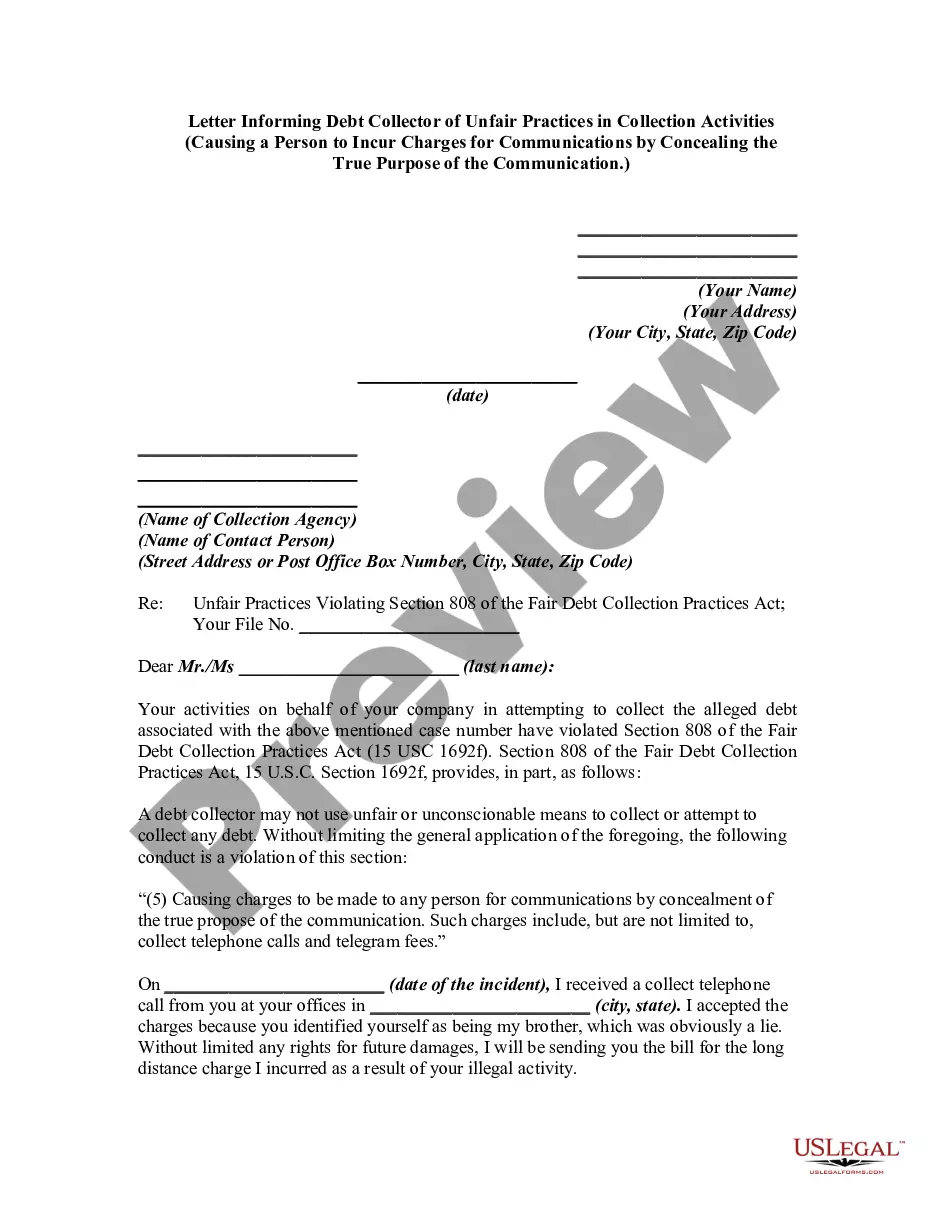

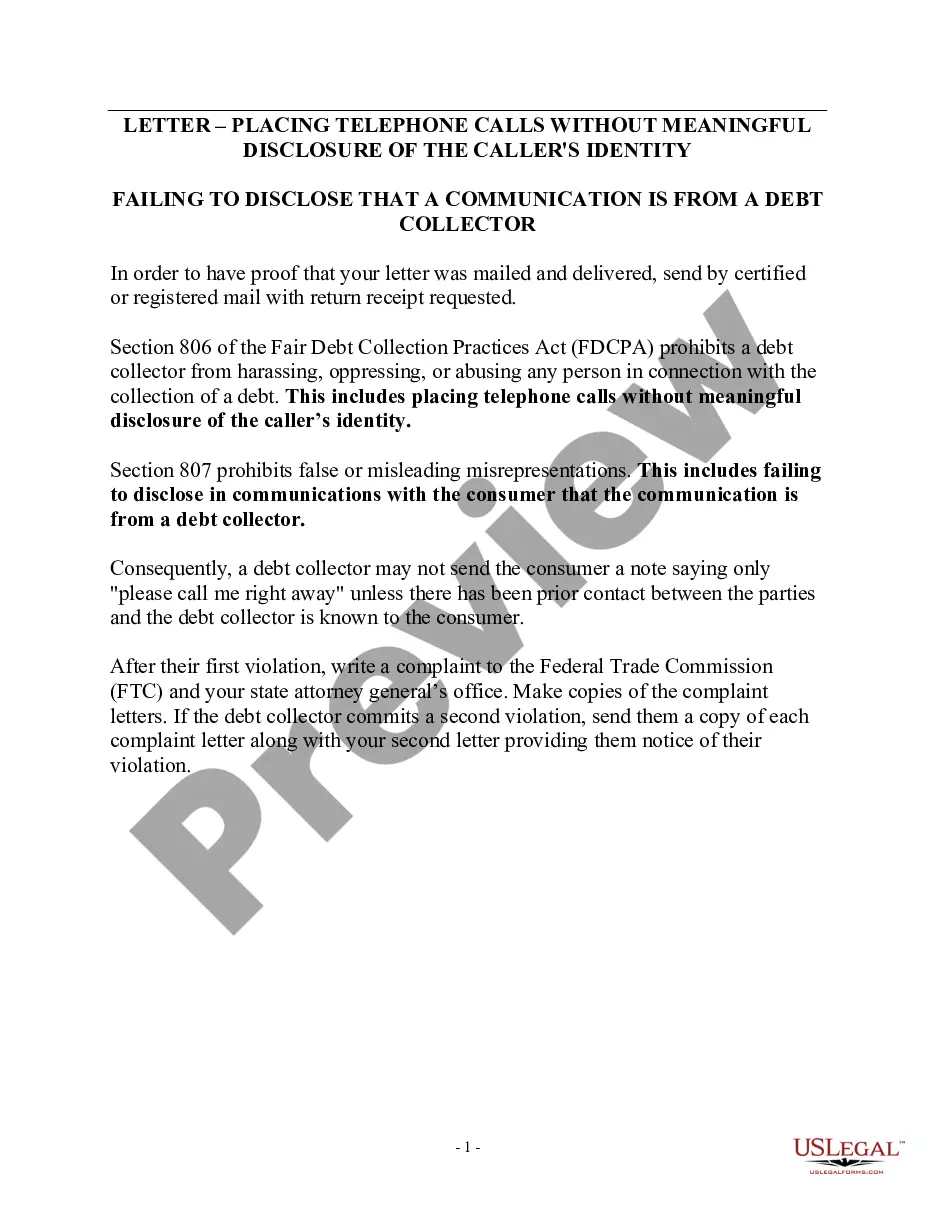

A debt collector may not use unfair or unconscionable means to collect a debt. This includes causing a person to incur charges for communications by concealing the true propose of the communication.

Nebraska Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication

Category:

State:

Multi-State

Control #:

US-DCPA-44

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Notice To Debt Collector - Causing A Consumer To Incur Charges For Communications By Concealing The Purpose Of The Communication?

Finding the appropriate lawful document template can be a challenge. Certainly, there is a multitude of formats accessible online, but how do you acquire the correct document you require? Utilize the US Legal Forms website. The platform provides thousands of templates, such as the Nebraska Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication, that can be used for both business and personal purposes. All templates are vetted by experts and comply with federal and state regulations.

If you are already registered, Log In to your account and click the Download button to obtain the Nebraska Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication. Use your account to browse through the legal documents you may have previously obtained. Navigate to the My documents section of your account and download another copy of the documents you need.

If you are a new user of US Legal Forms, here are simple steps you should follow: First, ensure you have selected the correct template for your city/region. You can review the document using the Preview button and check the form description to confirm it is suitable for you.

US Legal Forms is the largest collection of legal templates where you can find numerous document formats. Take advantage of the service to download professionally-crafted papers that comply with state regulations.

- If the document does not meet your requirements, use the Search function to locate the appropriate form.

- Once you are certain the document is suitable, click on the Purchase now button to acquire the template.

- Choose the pricing plan you prefer and fill in the required information.

- Create your account and pay for the transaction using your PayPal account or credit card.

- Select the file format and download the legal document template to your device.

- Complete, edit, print, and sign the downloaded Nebraska Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication.

Form popularity

FAQ

If you believe a debt collector is harassing you, you can submit a complaint with the CFPB online or by calling (855) 411-CFPB (2372). You can also contact your state's attorney general .

The average debt collection fee is typically between 20% to 35%. Several factors will impact how much a collection agency will charge. So let's break it down; Age of account Older debts are generally more complex to collect on, so they typically demand higher fees.

Regarding that amount: A debt collector can charge interest, but only up to the amount stipulated in your contract with the original creditor. Most states also cap the amount of interest and fees a debt collector can charge. Per FDCPA, a collector must cease contact if you send a letter requesting they do so.

The Debt Collectors Act specifically provides that a debt collector MAY NEVER charge more than 10% plus Vat of the amount received from the debtor as a collection commission (the Act refers to a receipt fee).

In addition to late charges and interest, an association is permitted to charge its reasonable costs incurred in collecting a delinquent assessment from a member, including reasonable attorney's fees. (Civ.

When a creditor sells a past due debt to a collection agency, the collection agency becomes the owner of debt. They may add additional interest and fees to the balance as part of their collection efforts, so the collection amount may be greater than the original amount that was written off by your creditor.

Believe it or not, though, it's possible to negotiate with a collection agent and end up paying less than you owe. Why is that? Because the collection agency bought the original debt from your creditor, most likely for a substantial discount. That means they don't have to recover the entire amount to make a profit.

A debt collector cannot collect more money than what is owed. For example, a debt collector cannot demand that you pay $2,000 in order to settle a debt that was originally only $500.

Extra charges may be added if you miss payments or you're late paying, but your creditor can only add charges if they're explained in your credit agreement. These charges must be fair and based on actual costs.

The creditor pays the collector a percentage, typically between 25% to 50% of the amount collected. Debt collection agencies collect various delinquent debtscredit cards, medical, automobile loans, personal loans, business, student loans, and even unpaid utility and cell phone bills.