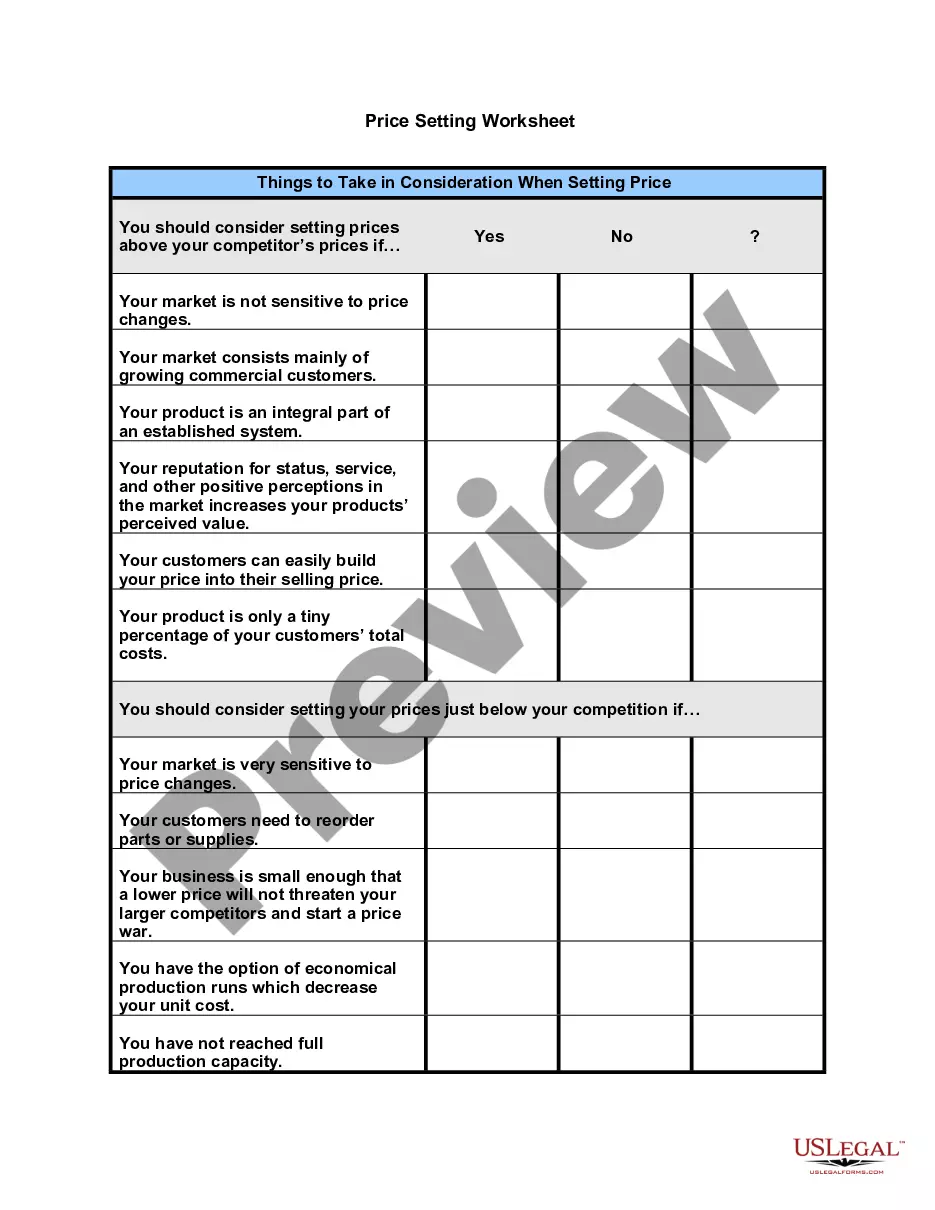

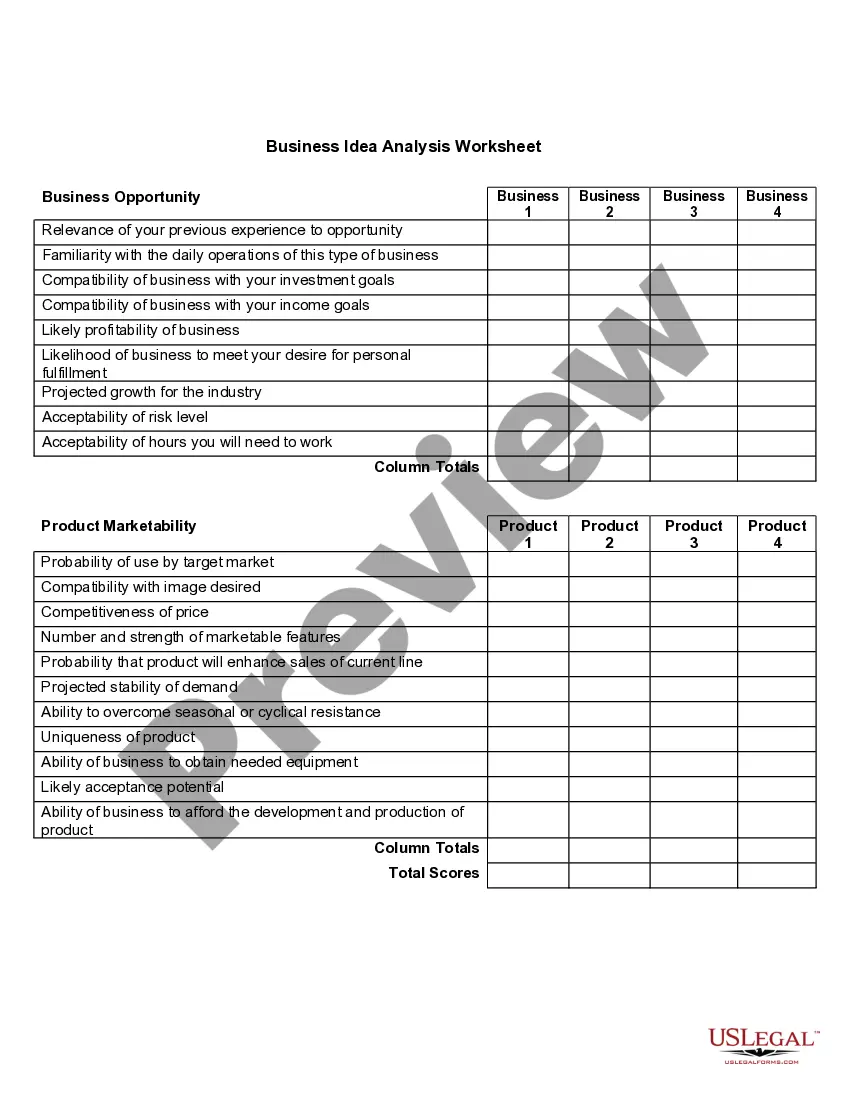

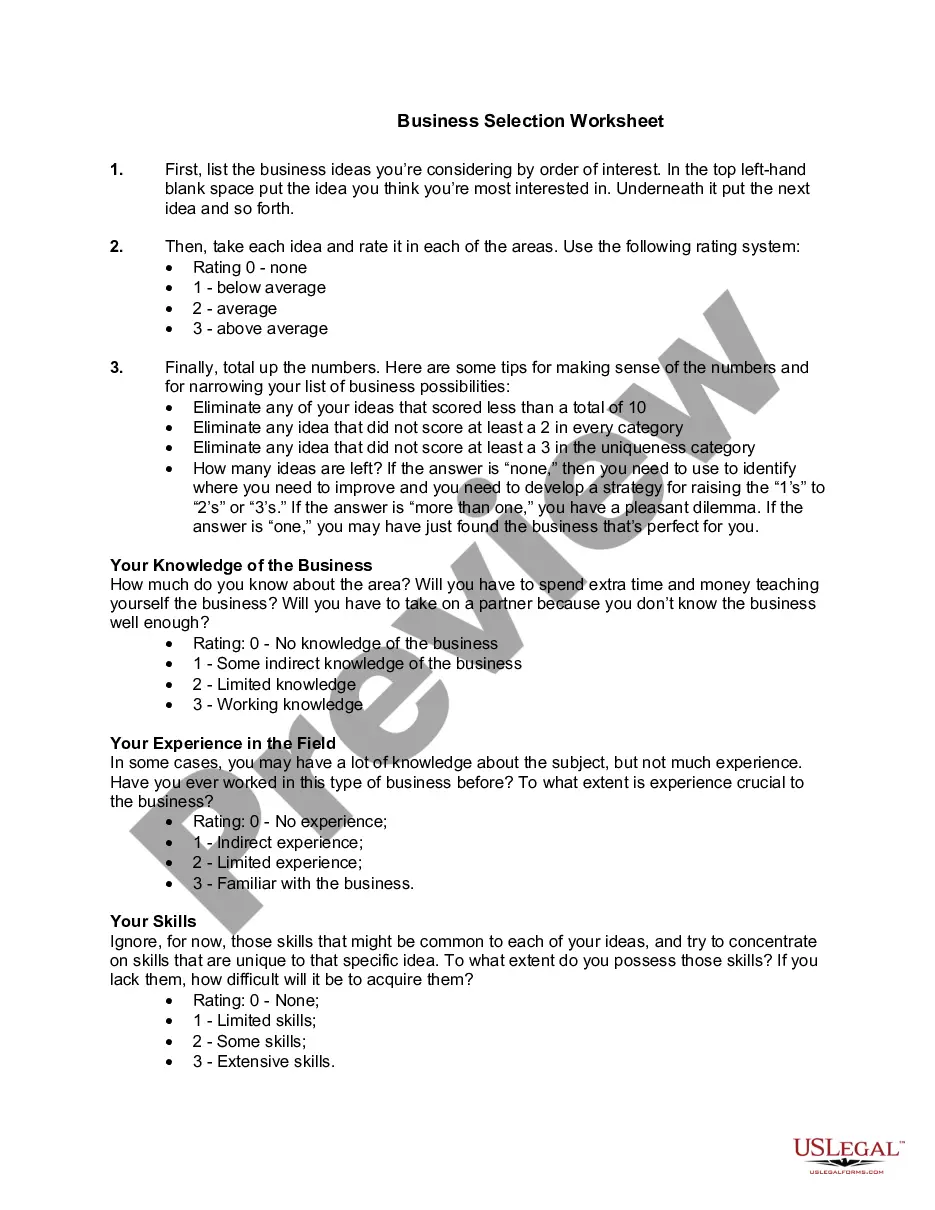

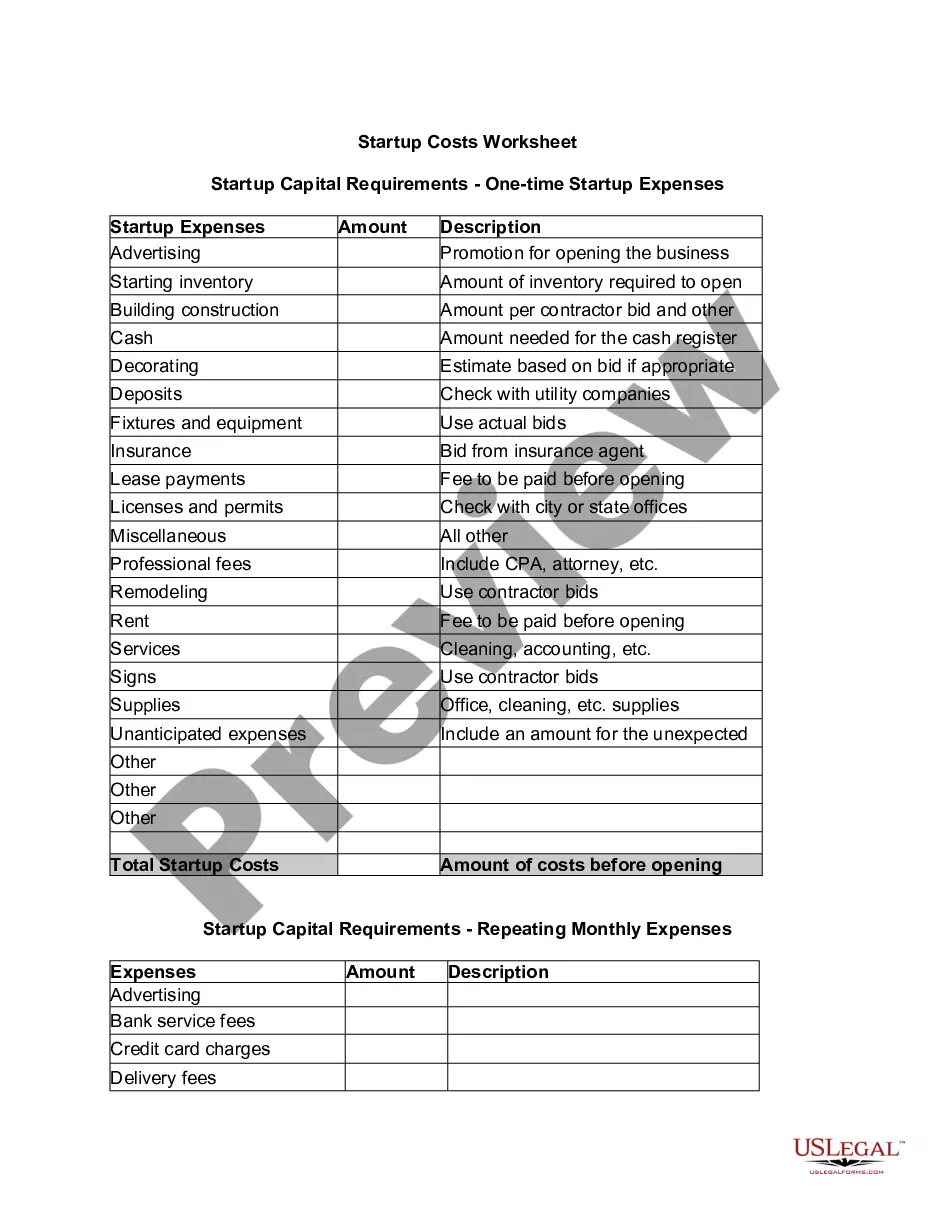

Nebraska Startup Costs Worksheet

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Startup Costs Worksheet?

Are you presently in a location where you frequently require paperwork for either business or personal reasons almost every day.

There are numerous credible document templates accessible online, but finding ones you can rely on isn't easy.

US Legal Forms provides thousands of form templates, including the Nebraska Startup Costs Worksheet, designed to meet state and federal regulations.

Once you have the correct form, click Buy now.

Select the pricing plan you require, complete the necessary information to create your account, and pay for the purchase using your PayPal or credit card.

- If you are already familiar with the US Legal Forms site and possess an account, simply Log In.

- Then, you can download the Nebraska Startup Costs Worksheet template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Choose the form you need and confirm it is for your correct jurisdiction/county.

- Utilize the Preview button to review the document.

- Read the description to ensure that you have selected the correct form.

- If the form isn't what you are looking for, use the Search field to find the form that suits your needs and requirements.

Form popularity

FAQ

Startup costs are costs paid or incurred in connection with investigating the creation or acquisition of an active trade or business or creating an active trade or business.

What are examples of startup costs? Examples of startup costs include licensing and permits, insurance, office supplies, payroll, marketing costs, research expenses, and utilities.

Qualifying costs Start-up costs include amounts paid for the following: An analysis or survey of potential markets, products, labor supply, transportation facilities, etc. Advertisements for the opening of the business. Salaries and wages for employees who are being trained and their instructors.

Startup costs will include equipment, incorporation fees, insurance, taxes, and payroll. Although startup costs will vary by your business type and industry an expense for one company may not apply to another.

Understanding your expenses and how you will manage them helps you launch your business successfully and continue to make a profit once your doors are open. By calculating your startup costs, you can: Estimate future profits. Perform a break-even analysis.

Key Takeaways. Startup costs are the expenses incurred during the process of creating a new business. Pre-opening startup costs include a business plan, research expenses, borrowing costs, and expenses for technology. Post-opening startup costs include advertising, promotion, and employee expenses.

Startup costs do not include costs for interest, taxes, and research and experimentation (Sec. 195(c)(1)).

Examples of startup costs include licensing and permits, insurance, office supplies, payroll, marketing costs, research expenses, and utilities.

The IRS allows you to deduct $5,000 in business startup costs and $5,000 in organizational costs, but only if your total startup costs are $50,000 or less. If your startup costs in either area exceed $50,000, the amount of your allowable deduction will be reduced by the overage.