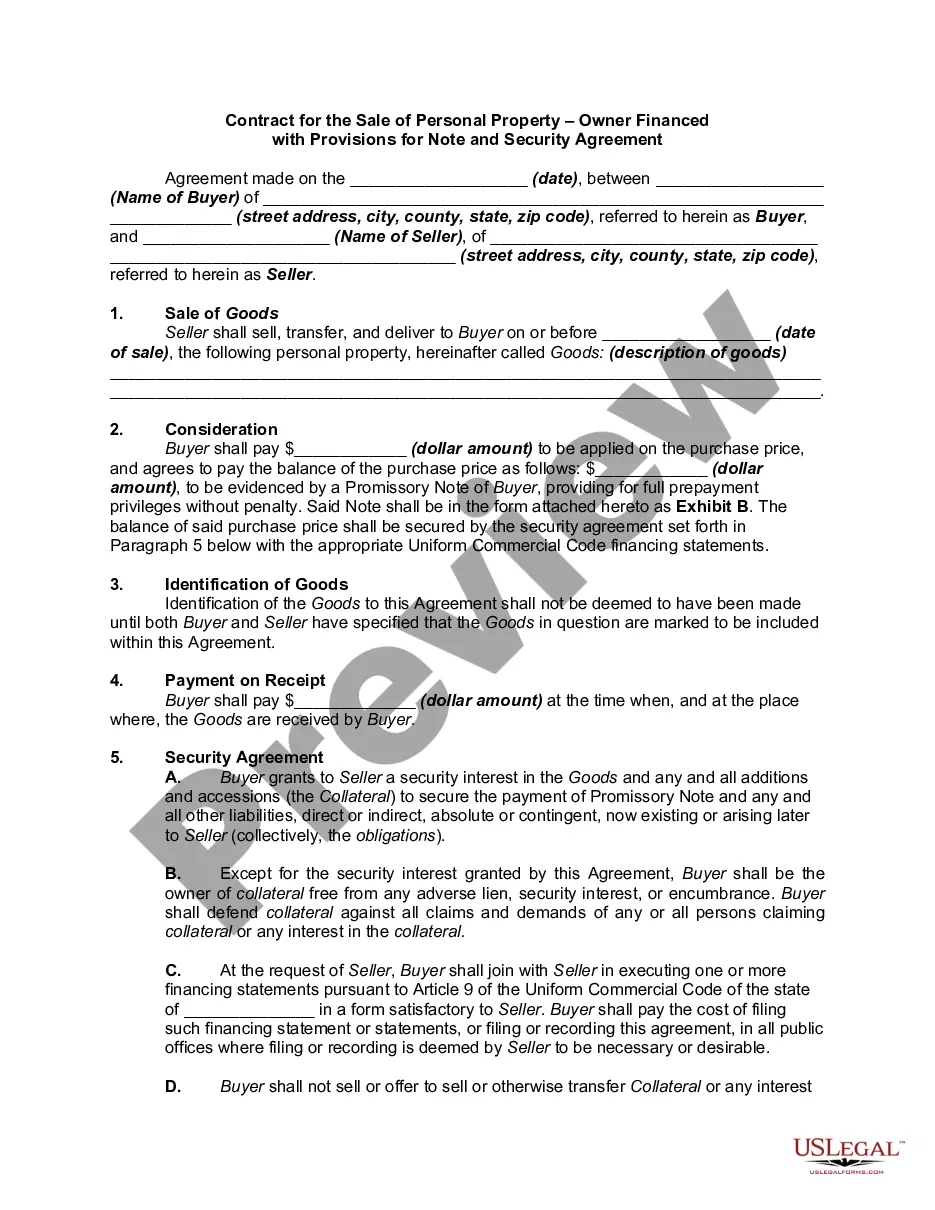

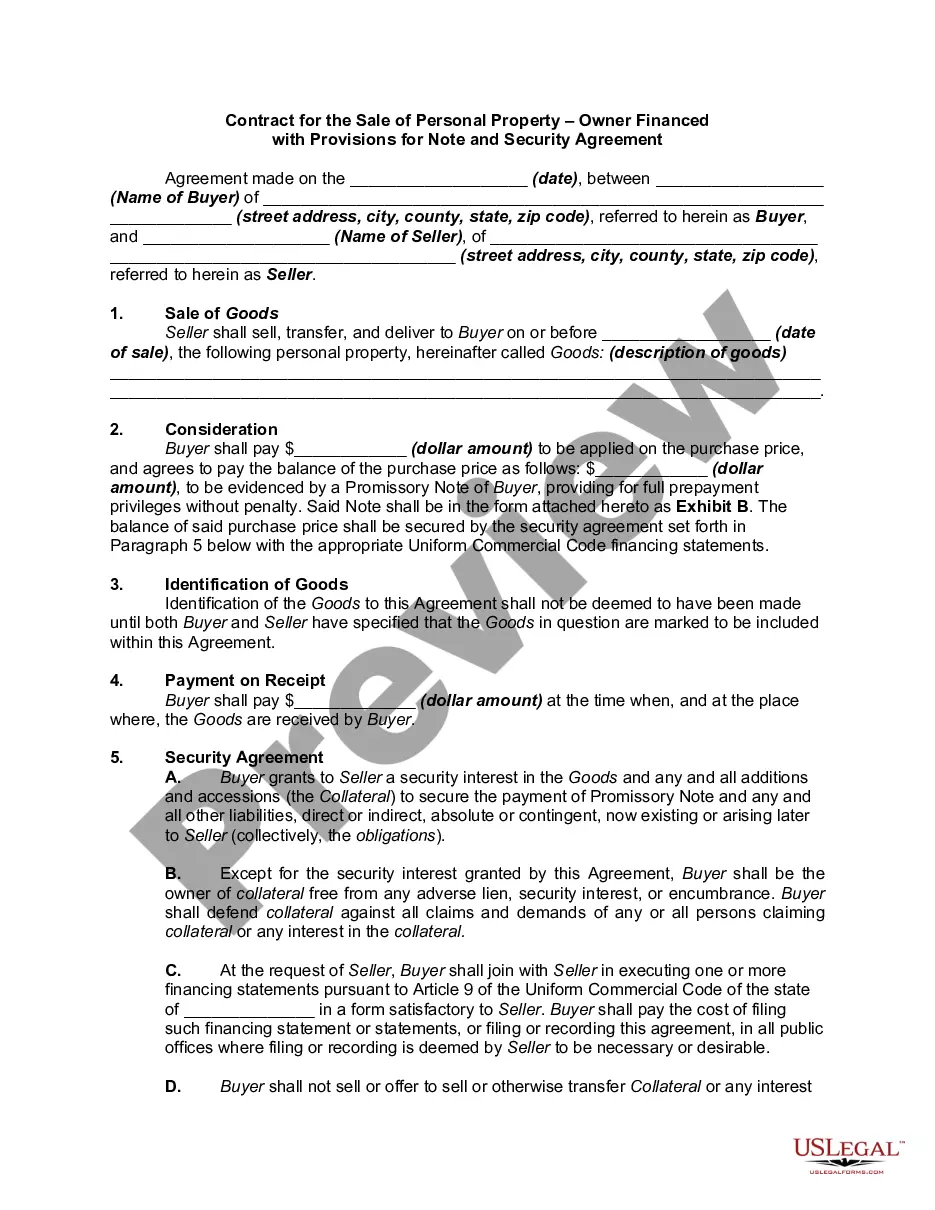

Nebraska Owner Financing Contract for Home

Description

How to fill out Owner Financing Contract For Home?

You can invest hours on the web attempting to locate the legal document template that complies with the federal and state requirements you require.

US Legal Forms offers a vast selection of legal documents that have been reviewed by experts.

You can obtain or create the Nebraska Owner Financing Agreement for Home via the service.

To locate another version of the form, utilize the Search field to find the template that meets your needs and specifications.

- If you already possess a US Legal Forms account, you can sign in and click the Download button.

- Subsequently, you can complete, modify, print, or sign the Nebraska Owner Financing Agreement for Home.

- Every legal document template you obtain is your personal property indefinitely.

- To retrieve another copy of any purchased form, navigate to the My documents tab and click on the appropriate button.

- If this is your first time using the US Legal Forms website, follow the simple instructions below.

- First, ensure that you have selected the correct document template for the county/city of your choice.

- Review the form description to ensure you have selected the correct template.

Form popularity

FAQ

In Nebraska, the seller typically sets up an owner financing arrangement. The seller can provide the terms of the financing through a Nebraska Owner Financing Contract for Home. It's essential for both parties to understand the agreement, including payment terms and interest rates. Engaging with professionals can make the process smoother, ensuring all legal requirements are met.

Two disadvantages of a contract for deed include the potential for higher interest rates compared to conventional loans and less legal protection for the buyer. Buyers may find themselves at risk if the seller faces financial difficulties or if the property needs repairs. Understanding these disadvantages is vital when considering a Nebraska Owner Financing Contract for Home.

Two notable disadvantages of a contract for deed include the potential for loss of equity and lack of consumer protections. If a buyer defaults, the seller can reclaim the property, often with little recourse for the buyer. It’s essential to understand these risks before entering into a Nebraska Owner Financing Contract for Home.

Yes, a contract for deed is often synonymous with seller financing. In this arrangement, the seller provides the financing directly to the buyer, allowing for an alternative means of purchasing property. The Nebraska Owner Financing Contract for Home specifically reflects this type of arrangement between the buyer and seller, with its unique terms.

In a Nebraska Owner Financing Contract for Home, the responsibility for property taxes usually falls on the buyer. Despite the seller retaining the title until the full payment, the buyer generally takes on the responsibility of paying property taxes. This ensures that the property remains in good standing with tax authorities.

The interest rate on a contract for deed can vary based on the seller’s terms and market conditions. Typically, the rates may range from 5% to 10%, similar to traditional mortgages. In the context of a Nebraska Owner Financing Contract for Home, the interest may also reflect the immediate needs and agreements between the buyer and seller.

Writing a Nebraska Owner Financing Contract for Home involves several key components. Clearly state the parties involved, describe the property, and outline the financial terms like principal, interest rates, and repayment schedule. Finally, include clauses that explain what happens in case of default and how disputes will be resolved. Utilizing tools from uslegalforms can streamline this process.

An example of owner financing can involve a seller who offers a property for $200,000 with a $20,000 down payment. The seller may then provide a mortgage for the remaining $180,000 at a fixed interest rate. This arrangement allows the buyer to make monthly payments directly to the seller instead of a bank, which is what an efficient Nebraska Owner Financing Contract for Home embodies.

The IRS has specific guidelines regarding a Nebraska Owner Financing Contract for Home that you should be aware of. They require that interest income from owner financing is reported and taxed accordingly. Additionally, any unpaid principal, interest, and default terms must be managed carefully to comply with IRS rules. Consider consulting a tax professional to navigate these rules effectively and ensure proper reporting.

Owner financing and seller financing are often used interchangeably, especially in a Nebraska Owner Financing Contract for Home. However, owner financing specifically refers to the seller providing financing directly to the buyer, while seller financing may include other arrangements or third-party involvement. Understanding this distinction can clarify expectations for both the buyer and the seller in the transaction. It’s important to have clear documentation to avoid any confusion in terms.