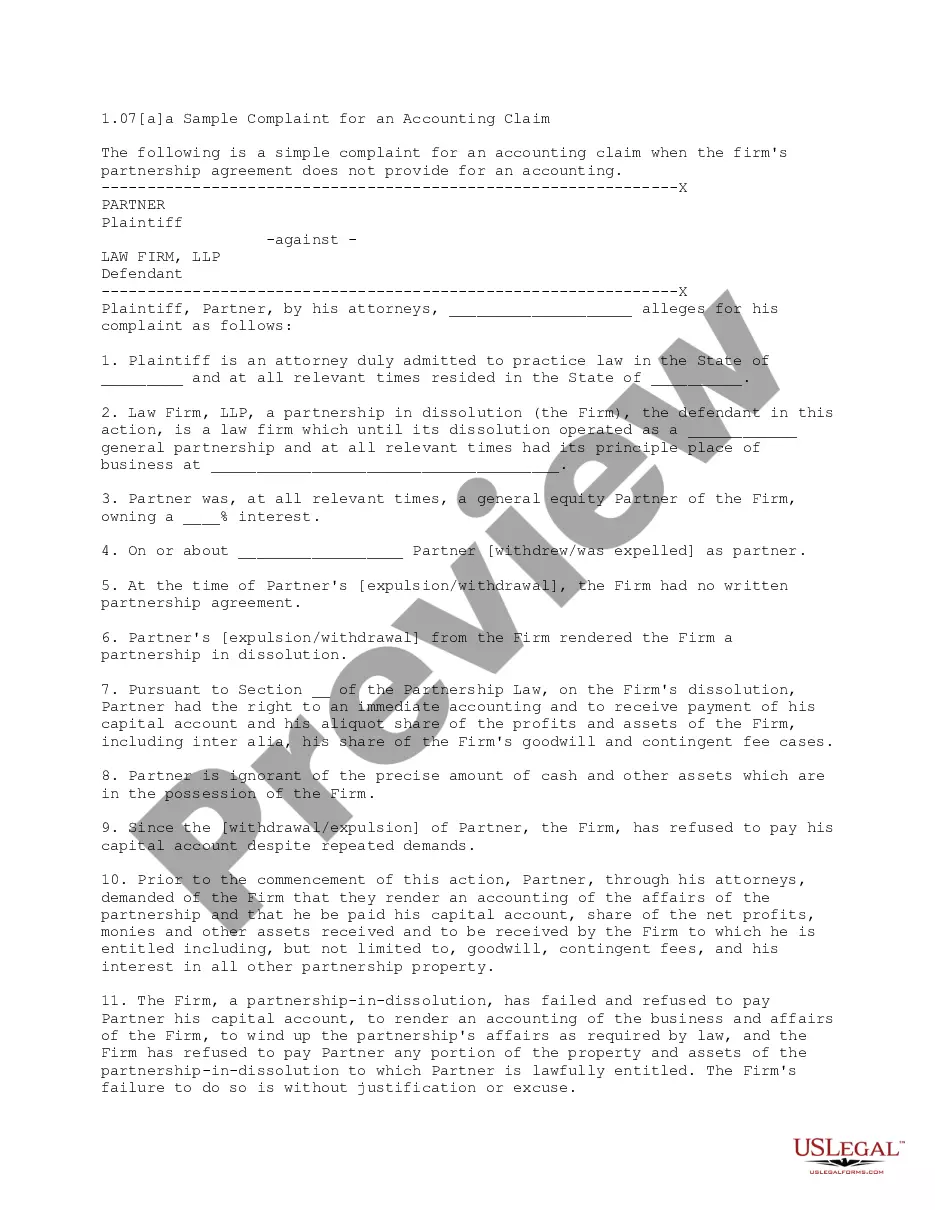

This complaint is for a plaintiff attorney who has been removed from the partnership of his former firm. The complaint requests an accounting of the former firm, stating that the plaintiff has been deprived of economic benefits rightfully due to him under the former partnership agreement, and also alleges egregious acts by his former partners.

North Carolina Alternative Complaint for an Accounting which includes Egregious Acts

Category:

State:

Multi-State

Control #:

US-L0107A

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Alternative Complaint For An Accounting Which Includes Egregious Acts?

Finding the right legal record template can be quite a struggle. Needless to say, there are a variety of themes available online, but how would you discover the legal type you want? Take advantage of the US Legal Forms site. The services provides thousands of themes, such as the North Carolina Alternative Complaint for an Accounting which includes Egregious Acts, that you can use for organization and personal demands. Every one of the types are examined by professionals and meet state and federal needs.

In case you are already authorized, log in to the accounts and click the Obtain key to find the North Carolina Alternative Complaint for an Accounting which includes Egregious Acts. Utilize your accounts to search from the legal types you possess bought earlier. Check out the My Forms tab of your respective accounts and acquire an additional copy in the record you want.

In case you are a new user of US Legal Forms, here are straightforward recommendations for you to comply with:

- Initially, ensure you have chosen the appropriate type to your area/county. You may examine the form while using Preview key and browse the form outline to ensure this is basically the right one for you.

- When the type does not meet your requirements, use the Seach discipline to get the right type.

- Once you are certain that the form would work, go through the Purchase now key to find the type.

- Select the costs prepare you need and type in the essential details. Build your accounts and buy the transaction using your PayPal accounts or bank card.

- Pick the file structure and obtain the legal record template to the device.

- Comprehensive, revise and produce and indicator the acquired North Carolina Alternative Complaint for an Accounting which includes Egregious Acts.

US Legal Forms may be the greatest library of legal types that you will find a variety of record themes. Take advantage of the service to obtain expertly-manufactured papers that comply with status needs.

Form popularity

FAQ

Rule III - EXTENSIONS OF TIME 3.1ANSWERS AND OTHER PLEADINGS: No Clerk of Court, or Assistant Clerk of Court, or Deputy Clerk of Court shall extend the time for answering any complaint or filing any pleading beyond the thirty (30) days allowed pursuant to the provisions of N.C.G.S. EXTENSIONS OF TIME, N.C. R. Prac. Super. & Dist. Ct. III Casetext ? rule ? north-carolina-court-rules Casetext ? rule ? north-carolina-court-rules

An extension of time to file a written Answer essentially provides an extra 30 days to file a written Answer at the courthouse. Although not guaranteed or automatic, filing an extension of time is common practice and is routinely granted in North Carolina.

Court Fees Filing a civil action (includes a $52.00 administrative fee) The administrative fee does not apply to applications for a writ of habeas corpus or to persons granted in forma pauperis status under 28 U.S.C § 1915.$402.00Filing a notice of appeal with the Fourth Circuit Court of Appeal1$505.0021 more rows ?

Steps to File a Suit Against an LLC Determine the court where the suit will take place. ... Find the legal name of the LLC. ... Draft the complaint which is the first document that will be filed with the court to begin the lawsuit. ... File the complaint with the court system.

14-43.16. Affirmative defense. (a) Affirmative Defense. - It is an affirmative defense to a prosecution under this Article that the person charged with the offense was a victim at the time of the offense and was coerced or deceived into committing the offense as a direct result of the person's status as a victim.

The following items must be submitted to the Clerk of Court: (i) complaint; (ii) summons; (iii) cover sheet; and (iv) filing fee. Venue is prescribed by statute. In civil actions, venue is typically the county in which the plaintiff or defendant resides.

Small claims court handles disputes involving less than $10,000 in cash or property. You don't need to hire an attorney and your case will usually be heard within one month of filing your lawsuit.

If someone sues your LLC, a judgment against the LLC could bankrupt your business or deprive it of its assets. Likewise, as discussed above, if the lawsuit was based on something you did?such as negligently injuring a customer?the plaintiff could go after you personally if the insurance doesn't cover their damages.

Within 30 days ? A defendant shall serve his answer within 30 days after service of the summons and complaint upon him. A party served with a pleading stating a crossclaim against him shall serve an answer thereto within 30 days after service upon him. NC General Statutes - Chapter 1A Article 3 North Carolina General Assembly (.gov) ? PDF ? ByArticle ? Arti... North Carolina General Assembly (.gov) ? PDF ? ByArticle ? Arti... PDF

? A defendant shall serve his answer within 30 days after service of the summons and complaint upon him. A party served with a pleading stating a crossclaim against him shall serve an answer thereto within 30 days after service upon him.