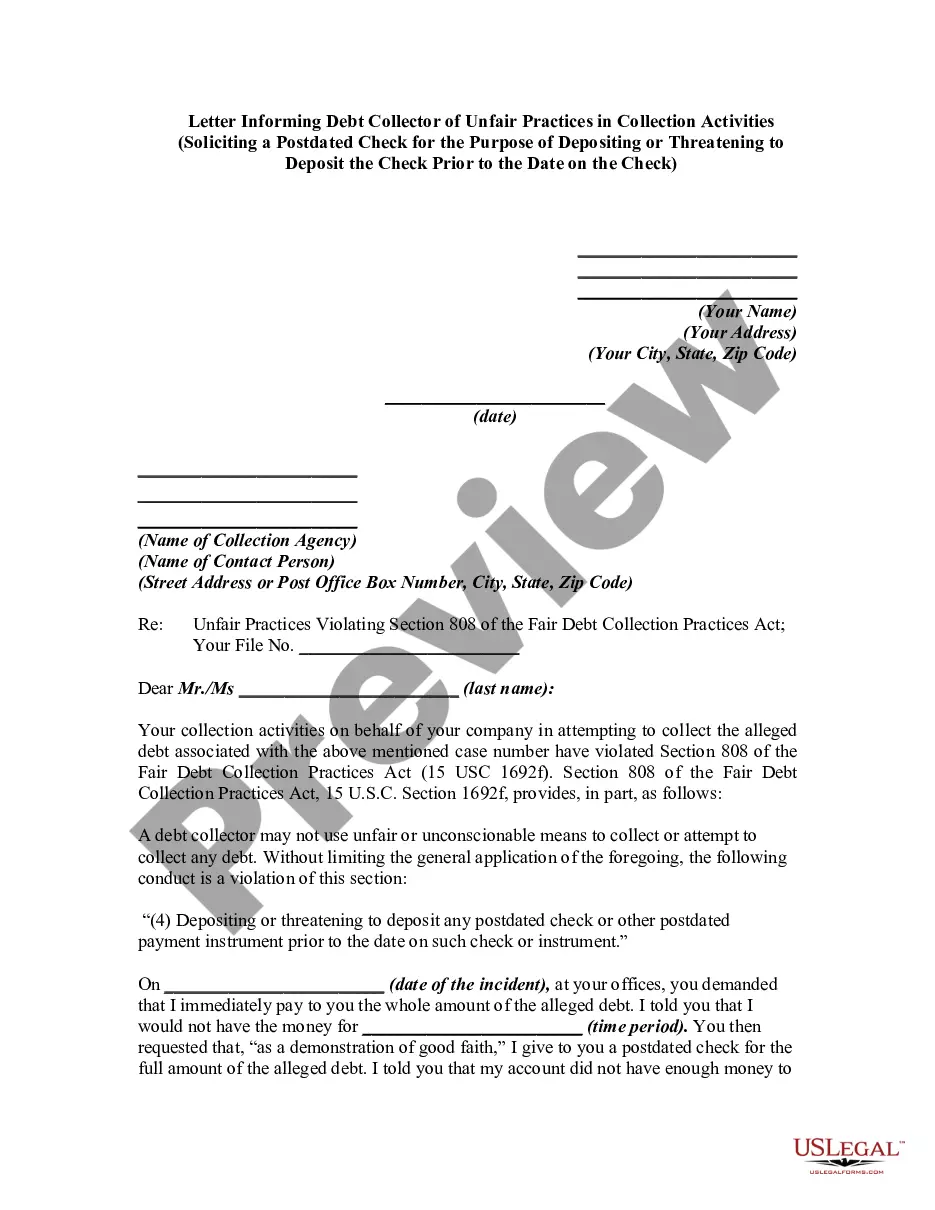

A debt collector may not use unfair or unconscionable means to collect a debt. This includes depositing a postdated check prior to the date on the check.

North Carolina Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check

Category:

State:

Multi-State

Control #:

US-DCPA-43

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Depositing A Postdated Check Prior To The Date On The Check?

It is feasible to spend hours online searching for the legal document template that meets the federal and state requirements you need.

US Legal Forms provides thousands of legal forms that have been reviewed by experts.

You can download or print the North Carolina Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check from their service.

If available, use the Preview option to look through the document template as well.

- If you have a US Legal Forms account, you can Log In and click the Obtain option.

- Once logged in, you can complete, revise, print, or sign the North Carolina Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check.

- Every legal document template you purchase is yours forever.

- To obtain another copy of the acquired form, go to the My documents tab and click the corresponding option.

- If this is your first time using the US Legal Forms site, follow the simple instructions below.

- First, ensure you have selected the correct document template for the county/region of your choice.

- Check the form details to ensure you have selected the right form.

Form popularity

FAQ

Can a bank or credit union cash a post-dated check before the date on the check? Yes. Banks and credit unions generally don't have to wait until the date you put on a check to cash it. However, state law may require the bank or credit union to wait to cash the check if you give it reasonable notice.

Federal law restricts what a debt collector can and cannot do with your postdated check. Specifically, under the Fair Debt Collection Practices Act (FDCPA), a debt collector cannot: coerce you into making a postdated payment by threatening or instituting criminal prosecution.

Several banks now offer a service where your paycheck is available one or two days before the regular payday if your employer uses direct deposit. This early direct deposit of your paycheck could help you keep up with bills and avoid late fees, especially on bills due around the time you receive your salary.

Unfortunately, the fact is that there's generally no actual obligation to honor the date on a check.

Can a bank or credit union cash a post-dated check before the date on the check? Yes. Banks and credit unions generally don't have to wait until the date you put on a check to cash it. However, state law may require the bank or credit union to wait to cash the check if you give it reasonable notice.

In most cases, when you receive a postdated check, you can deposit or cash a postdated check at any time. Debt collectors may be prohibited from processing a check before the date on the check, but most individuals are free to take postdated checks to the bank immediately.

Depositing a postdated check a day early may cause the check writer's bank to attempt to pay the check immediately. If the check writer does not yet have the funds in his bank account, this will cause the check to "bounce," or be returned for nonsufficient funds.

According to UCC § 3-113, if a financial instrument, such as a check, is undated, its official date is the date on which it first came into the possession of the person or business listed on it. Since banks follow the UCC, your undated check will be deposited.

A signed check immediately becomes legal tender that a bank can deposit or cash before the indicated date on the check. Therefore, a bank will be able to accept a check if it is dated and signed. Ask your bank or credit union for their specific policy for postdated checks in their account disclosures.

Yes. Banks and credit unions generally don't have to wait until the date you put on a check to cash it. However, state law may require the bank or credit union to wait to cash the check if you give it reasonable notice. Contact your bank or credit union to learn what its policies are.