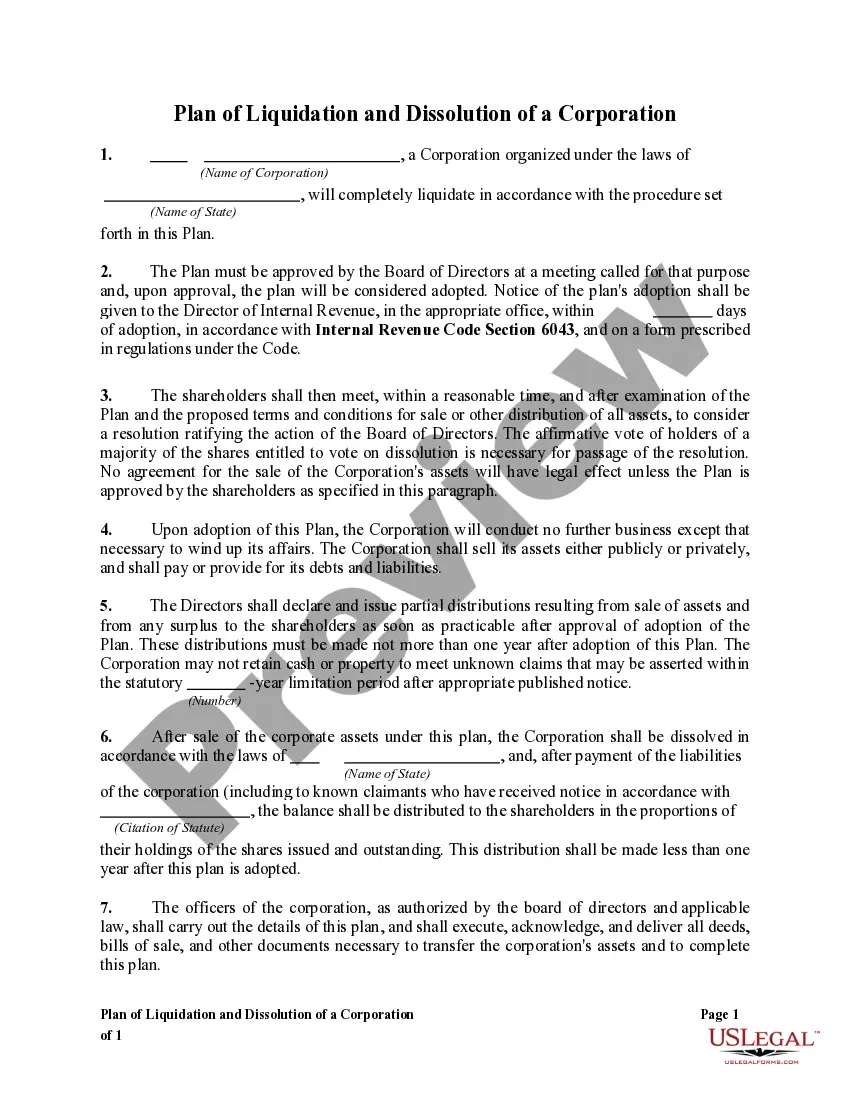

North Carolina Plan of complete liquidation and dissolution

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Plan Of Complete Liquidation And Dissolution?

US Legal Forms - one of several biggest libraries of legal varieties in the USA - delivers a wide array of legal record web templates you are able to down load or print out. Using the web site, you will get a huge number of varieties for business and person reasons, sorted by categories, says, or search phrases.You can find the most recent models of varieties just like the North Carolina Plan of complete liquidation and dissolution in seconds.

If you currently have a subscription, log in and down load North Carolina Plan of complete liquidation and dissolution from your US Legal Forms library. The Obtain option will appear on each develop you see. You have accessibility to all formerly delivered electronically varieties from the My Forms tab of the profile.

If you want to use US Legal Forms the very first time, listed below are straightforward recommendations to help you get started off:

- Be sure you have chosen the proper develop for your city/area. Go through the Review option to analyze the form`s information. See the develop explanation to ensure that you have selected the appropriate develop.

- When the develop does not fit your requirements, take advantage of the Look for industry towards the top of the display to obtain the the one that does.

- If you are satisfied with the form, affirm your choice by clicking on the Buy now option. Then, pick the pricing strategy you prefer and supply your credentials to sign up for the profile.

- Approach the transaction. Utilize your bank card or PayPal profile to accomplish the transaction.

- Select the formatting and down load the form on the system.

- Make changes. Load, revise and print out and signal the delivered electronically North Carolina Plan of complete liquidation and dissolution.

Each and every web template you included in your bank account does not have an expiry time and is also your own forever. So, if you would like down load or print out yet another copy, just proceed to the My Forms section and then click in the develop you need.

Gain access to the North Carolina Plan of complete liquidation and dissolution with US Legal Forms, by far the most comprehensive library of legal record web templates. Use a huge number of skilled and condition-specific web templates that satisfy your organization or person requires and requirements.

Form popularity

FAQ

The quick answer. Liquidate means a formal closing down by a liquidator when there are still assets and liabilities to be dealt with. Dissolving a company is where the business is struck off the register at Companies House because it is now inactive.

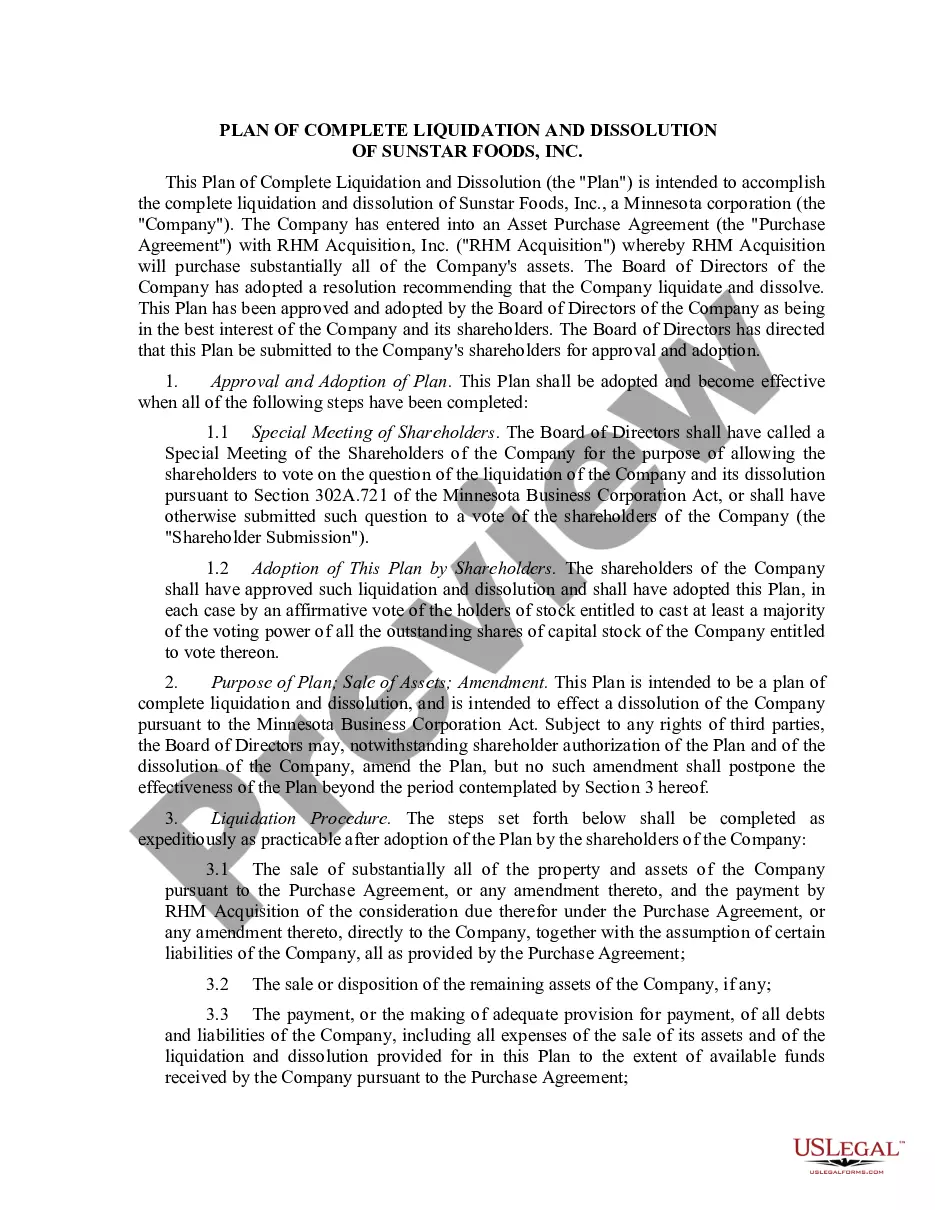

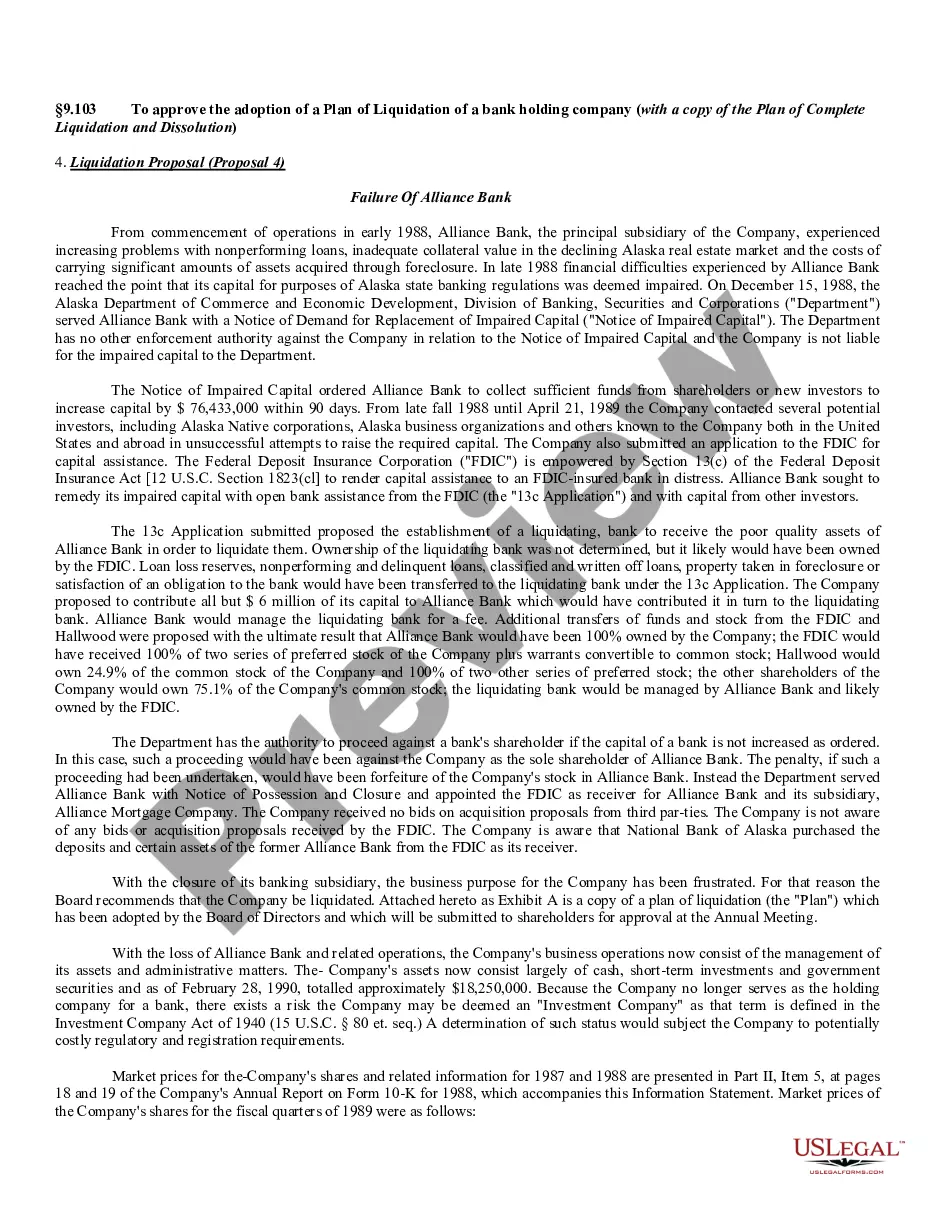

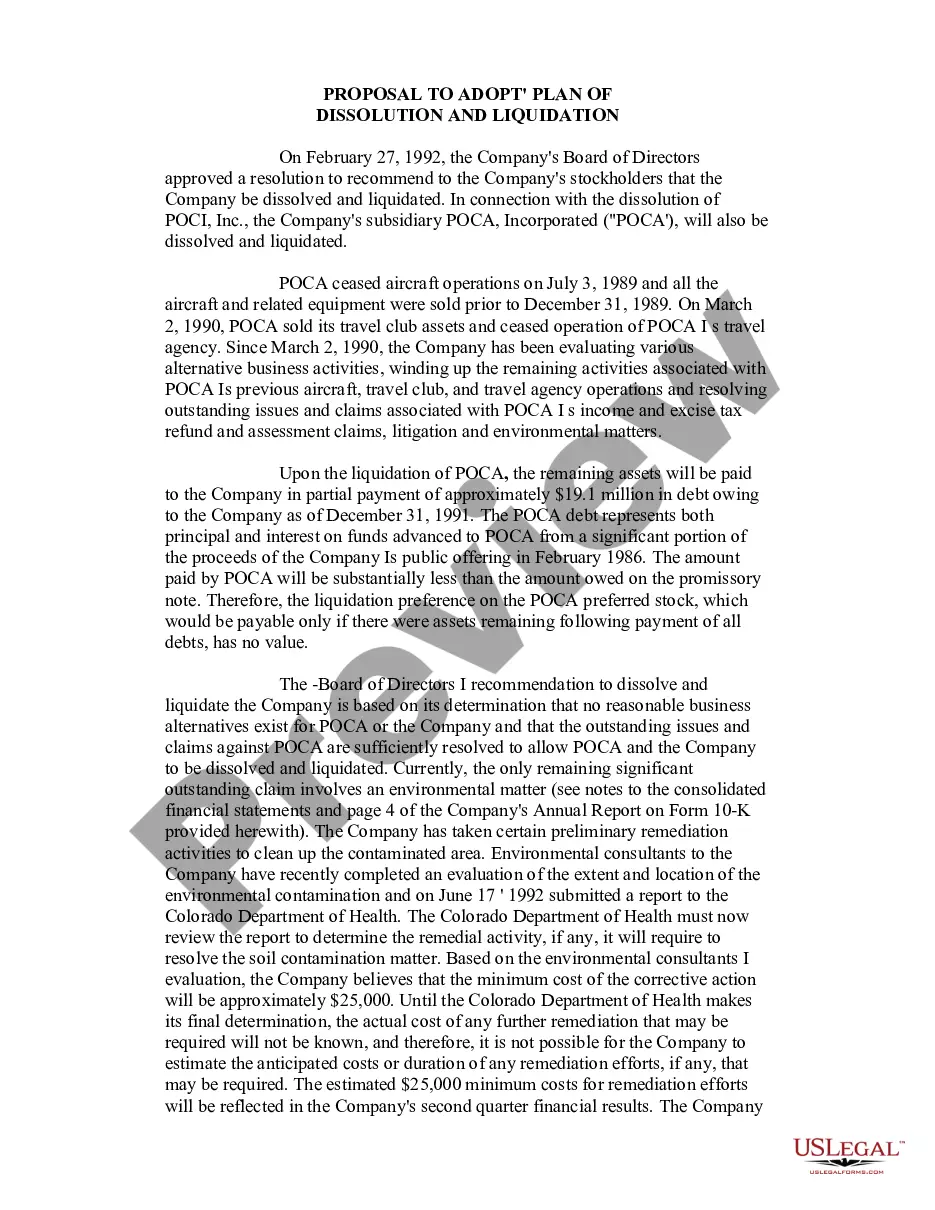

A plan of liquidation and dissolution that can be used for the dissolution of a Delaware corporation wholly owned by a US parent corporation when the parties intend to qualify the dissolution as a tax-free liquidation under Sections 332 and 337 of the Internal Revenue Code.

A plan of dissolution is a written description of how an entity intends to dissolve, or officially and formally close the business. A plan of dissolution will include a description of how any remaining assets and liabilities will be distributed.

To dissolve your nonprofit, you will need a plan of dissolution. At a minimum, the plan must provide that all of your nonprofit's liabilities and obligations are to be paid and discharged, or otherwise adequately provided for, and also provide for the proper distribution of any remaining assets.

Once an entity is administratively dissolved, it may apply to the Secretary of State for reinstatement (or requalification, in the case of foreign entities). The entities must submit an application and correct all reasons that led to the dissolution or else prove to the Secretary that the grounds do not exist.

A plan of dissolution, which specifies how the nonprofit corporation's remaining assets shall be distributed, must be attached to the Articles of Dissolution.

The liquidating corporation distributes all of its assets to its shareholders, the assets are distributed in one or a series of distributions, the distributions are in redemption of all of the corporation's stock, the distributions are made pursuant to a plan of liquidation.

A plan of dissolution is a written description of how an entity intends to dissolve, or officially and formally close the business. A plan of dissolution will include a description of how any remaining assets and liabilities will be distributed.