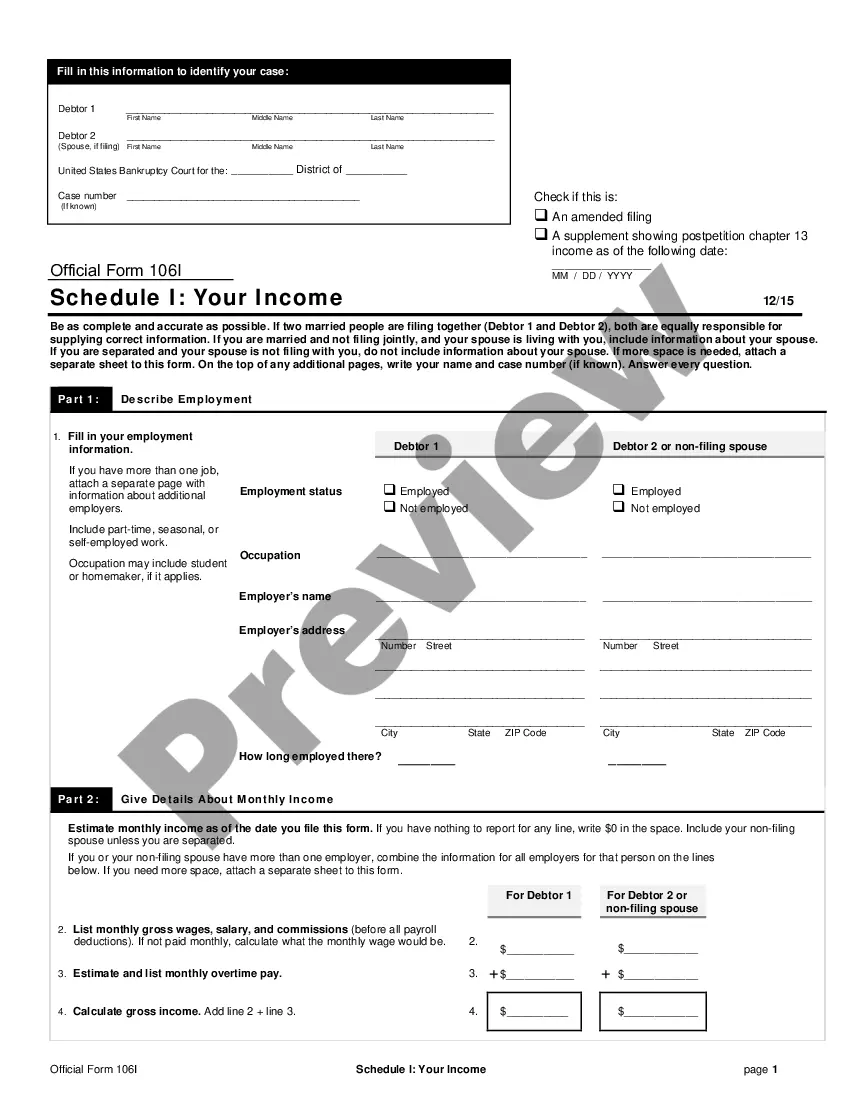

This form is Schedule I. The form lists the current income of the individual debtor(s). The form also contains the following information about the debtor(s): name and address of the debtor(s); place of employment; and total net monthly take home pay. This form is data enabled to comply with CM/ECF electronic filing standards. This form is for post 2005 act cases.

Montana Current Income of Individual Debtors - Schedule I - Form 6I - Post 2005

Category:

State:

Multi-State

Control #:

US-BKR-F6I

Format:

Word;

PDF;

Rich Text

Instant download

This website is not affiliated with any governmental entity

Public form

Description

How to fill out Current Income Of Individual Debtors - Schedule I - Form 6I - Post 2005?

Finding the right legal papers web template can be a have a problem. Needless to say, there are plenty of web templates available on the Internet, but how do you obtain the legal develop you will need? Make use of the US Legal Forms web site. The services provides thousands of web templates, for example the Montana Current Income of Individual Debtors - Schedule I - Form 6I - Post 2005, which can be used for business and private needs. All the varieties are examined by pros and satisfy federal and state requirements.

When you are presently signed up, log in for your bank account and then click the Down load key to find the Montana Current Income of Individual Debtors - Schedule I - Form 6I - Post 2005. Use your bank account to search through the legal varieties you might have bought in the past. Proceed to the My Forms tab of the bank account and obtain an additional duplicate in the papers you will need.

When you are a fresh end user of US Legal Forms, here are straightforward instructions that you can comply with:

- Very first, make certain you have selected the proper develop to your town/county. It is possible to examine the form making use of the Review key and browse the form information to make sure it is the right one for you.

- In case the develop is not going to satisfy your needs, utilize the Seach industry to get the proper develop.

- When you are certain that the form is suitable, go through the Get now key to find the develop.

- Select the rates prepare you want and type in the essential info. Create your bank account and pay for your order using your PayPal bank account or bank card.

- Select the file format and download the legal papers web template for your gadget.

- Comprehensive, change and print and sign the obtained Montana Current Income of Individual Debtors - Schedule I - Form 6I - Post 2005.

US Legal Forms may be the greatest library of legal varieties where you can discover a variety of papers web templates. Make use of the company to download professionally-manufactured files that comply with condition requirements.

Form popularity

FAQ

Examples of nonexempt assets that can be subject to liquidation: Additional home or residential property that is not your primary residence. Investments that are not part of your retirement accounts. An expensive vehicle(s) not covered by bankruptcy exemptions.

The biggest difference between Chapter 7 and Chapter 13 is that Chapter 7 focuses on discharging (getting rid of) unsecured debt such as credit cards, personal loans and medical bills while Chapter 13 allows you to catch up on secured debts like your home or your car while also discharging unsecured debt.

That being said, here's what you're not allowed to do with a Chapter 7: Lie under oath about your financial or property assets. Keep property that must be used to discharge your debts. Miss payments to certain creditors in order to keep your home.

A Chapter13 bankruptcy may be filed by individuals with regular income. Debtors must present a plan to repay all or part of their debts. The plan must provide for fixed monthly payments to be made to the Chapter 13 trustee for a period of three to five years, depending on income and other factors.

Bankruptcy is still a process that should be taken very seriously. While debtors in bankruptcy are still allowed to spend their own money on whatever they want, they should do everything possible to avoid spending beyond essential purchases.

It's a Long Term Commitment ? Filing Chapter 13 bankruptcy requires you to make a long-term commitment to the process. Tough To Get Credit or a Mortgage for 7 Years ? Other impacts include the inability to get credit cards at a good rate, and filing Chapter 13 makes it tough to get a mortgage.

Disadvantages to a Chapter 7 Bankruptcy: If you want to keep a secured asset, such as a car or home, and it is not completely covered by your bankruptcy exemptions then Chapter 7 is not an option. The automatic stay created by filing Chapter 7 Bankruptcy only serves as a temporary defense against foreclosure.

A chapter 13 bankruptcy is also called a wage earner's plan. It enables individuals with regular income to develop a plan to repay all or part of their debts. Under this chapter, debtors propose a repayment plan to make installments to creditors over three to five years.

In many cases, Chapter 7 bankruptcy is a better fit than Chapter 13 bankruptcy. For instance, not only is Chapter 7 quicker, many people prefer the following two things as well: filers keep all or most of their property, and. filers don't pay creditors through a three- to five-year Chapter 13 repayment plan.

A Chapter 13 petition for bankruptcy will likely necessitate a $500 to $600 monthly payment, especially for debtors paying at least one automobile through the payment plan. However, since the bankruptcy court will consider a large number of factors, this estimate could vary greatly.