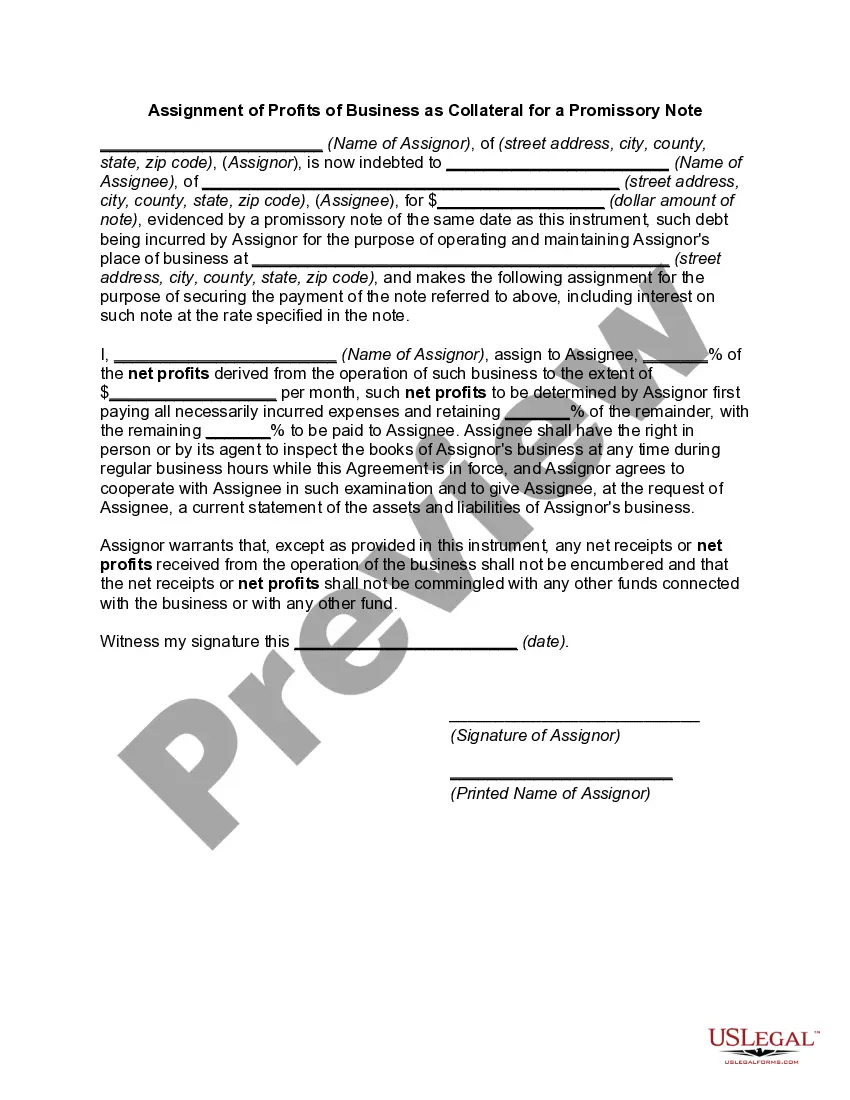

Montana Assignment of Profits of Business

Description

How to fill out Assignment Of Profits Of Business?

Are you in a situation where you need documents for both business or personal purposes nearly every day.

There are numerous legal document templates accessible online, but finding ones you can rely on is not simple.

US Legal Forms offers a vast array of form templates, such as the Montana Assignment of Profits of Business, designed to meet federal and state requirements.

Choose a convenient document format and download your copy.

View all the document templates you have purchased under the My documents menu. You can access another copy of the Montana Assignment of Profits of Business at any time. Click on the required form to download or print the document template.

- If you are already acquainted with the US Legal Forms site and possess an account, simply Log In.

- After that, you can download the Montana Assignment of Profits of Business template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Find the form you need and confirm it is for the correct city/state.

- Utilize the Preview button to review the form.

- Check the details to ensure you have selected the correct form.

- If the form isn't what you need, use the Search section to locate the form that fits your needs.

- When you find the correct form, click on Purchase now.

- Select the payment plan you prefer, enter the necessary information to create your account, and pay for the transaction using your PayPal or Visa or Mastercard.

Form popularity

FAQ

Montana is one of only nine states that offer a tax break for capital gains income. Over 50 percent of the tax break went to the wealthiest 4,500 households in Montana (those earning more than $365,000). More than 85 percent of taxpayers (more than 468,000 Montanans) did not benefit from the capital gains tax credit.

Revenues come mainly from tax collections, licensing fees, federal aid, and returns on investments. Expenditures generally include spending on government salaries, infrastructure, education, public pensions, public assistance, corrections, Medicaid, and transportation.

Montana has a graduated individual income tax, with rates ranging from 1.00 percent to 6.75 percent. Montana has a 6.75 percent corporate income tax rate. Montana does not have a state sales tax and does not levy local sales taxes.

The IRS counts the following common income sources as taxable income: Wages, salaries, tips and other taxable employee pay. Union strike benefits. Long-term disability benefits received prior to minimum retirement age. Net self-employment or freelance earnings under certain circumstances.

In general, all income from work performed in the state, real or personal property located in the state, and business conducted in the state is Montana source income.

Montana Capital Gains TaxWhile Montana does tax capital gains, the state offers the capital gain tax credit to offset the cost. The credit is equal to 2% of all net capital gains listed on your Montana income tax return. In effect, that lowers the top capital gains tax rate in Montana from 6.9% to 4.9%.

Passive loss carryover exclusion is the difference between passive losses allowed on Federal Form 8582 versus passive losses allowed on the Montana Form 8582. Notes: When the federal passive loss allowed is less than Montana's passive loss allowed, then an adjustment is made on MT Form 2, page 5, line 24.

The states with no additional state tax on capital gains are: Alaska, Florida, New Hampshire, Nevada, South Dakota, Tennessee, Texas, Washington, and Wyoming. These are the same states that do not tax personal income on wages, although they might tax interest and dividends from investments, depending on the state.

All wages and any other compensation for services performed in the United States are generally considered to be from sources in the United States.