Mississippi MHA Request for Short Sale

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out MHA Request For Short Sale?

It is feasible to spend numerous hours online searching for the legal document template that fits the state and federal requirements you need.

US Legal Forms offers a vast array of legal forms that can be examined by professionals.

You have the option to download or create the Mississippi MHA Request for Short Sale from your account.

To obtain an additional version of your form, utilize the Search field to locate the template that meets your needs and requirements.

- If you already have a US Legal Forms account, you can Log In and select the Obtain option.

- After that, you can complete, modify, create, or sign the Mississippi MHA Request for Short Sale.

- Every legal document template you purchase is yours indefinitely.

- To acquire an additional copy of any purchased form, navigate to the My documents tab and select the appropriate option.

- If this is your first time using the US Legal Forms website, follow the simple instructions below.

- First, ensure you have chosen the correct document template for your county/region of interest.

- Review the document description to confirm you have selected the correct form.

Form popularity

FAQ

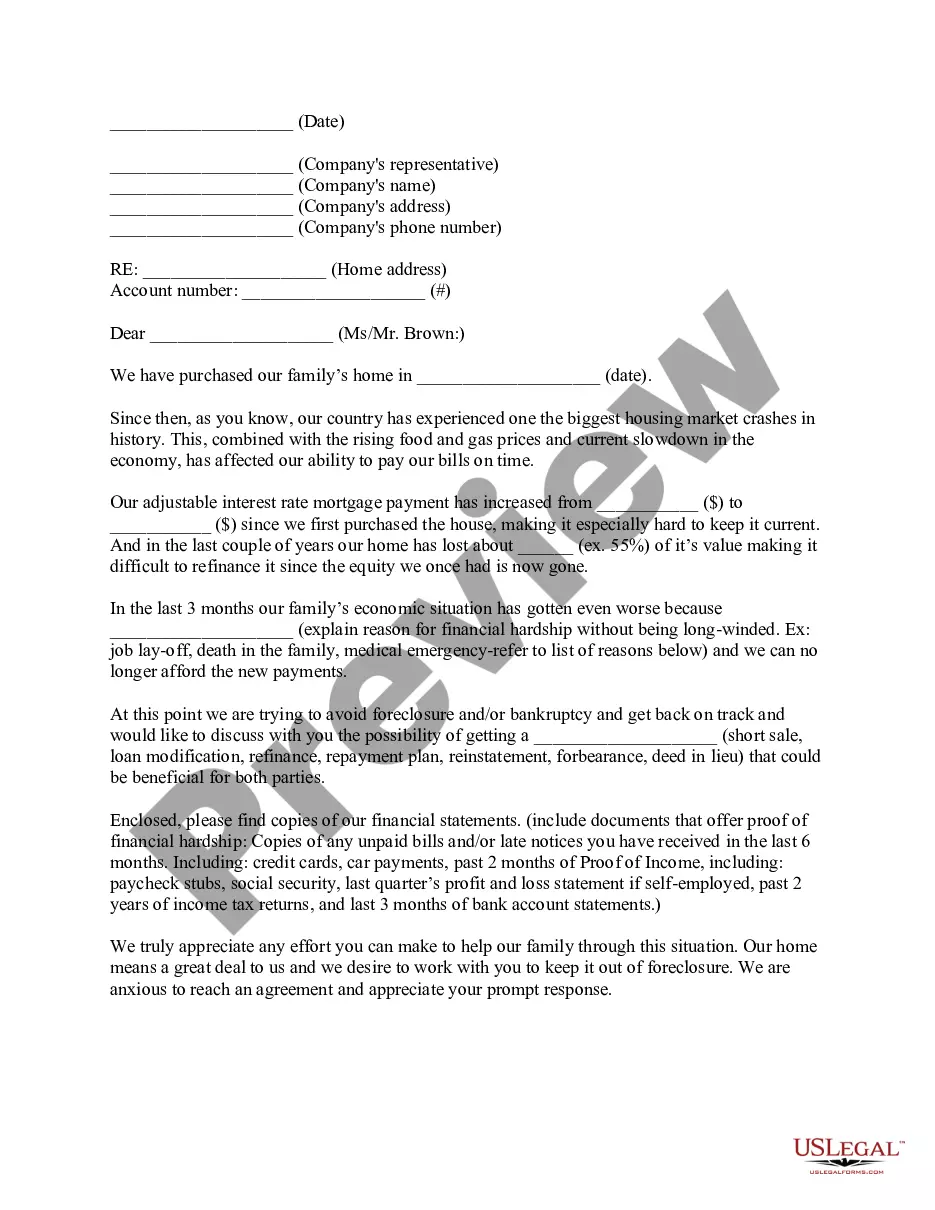

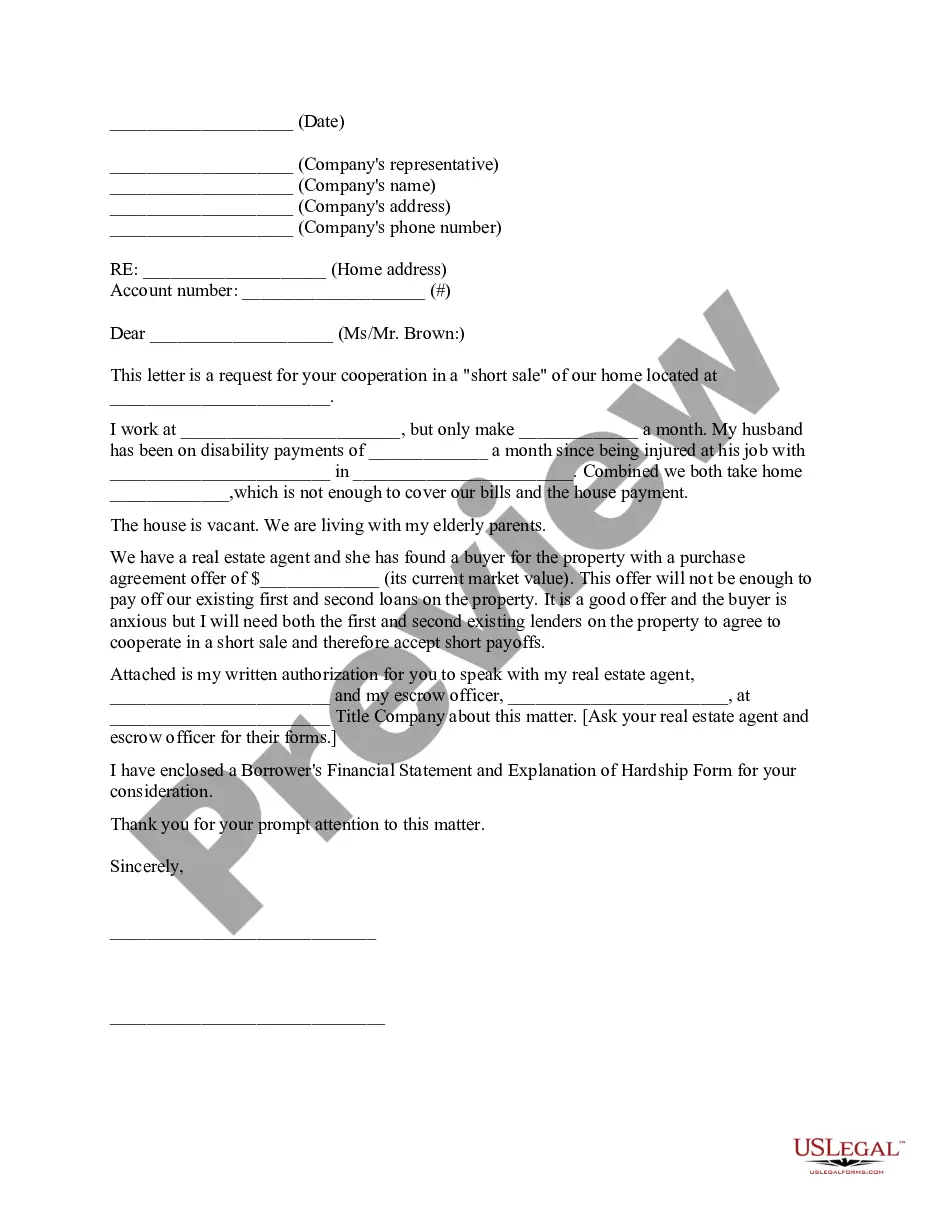

Mississippi law allows lenders to foreclose on a property through a non-judicial process, meaning they do not need to go to court. The process usually begins after three missed payments, and lenders must notify homeowners appropriately. If you're facing foreclosure, you might consider a Mississippi MHA Request for Short Sale as an alternative. This approach can help you navigate your options and avoid a foreclosure mark on your credit.

To buy a foreclosed home in Mississippi, first, check listings online or consult with a real estate agent. Often, these properties go to auction or are listed through banks. Knowing about programs like the Mississippi MHA Request for Short Sale can also provide insights into purchasing distressed properties. It’s wise to conduct thorough research and inspections before making an offer.

The second lien modification program, or 2MP, is designed to assist homeowners with a second mortgage. Through this program, borrowers may have the chance to reduce their second mortgage balance or payment. If you are facing challenges, consider submitting a Mississippi MHA Request for Short Sale; it might provide a way out while addressing your second lien issues. Be sure to research all available options for your situation.

A deed in lieu of foreclosure is when a homeowner voluntarily transfers their property title to the lender to avoid foreclosure. This option can simplify the process for both parties. If you are struggling to make payments, submitting a Mississippi MHA Request for Short Sale could also be beneficial. It’s essential to explore these alternatives to minimize the impact on your financial future.

In Mississippi, lenders usually begin the foreclosure process after you have missed three payments in a row. So, if you find yourself in this situation, it's crucial to act quickly. Options such as filing a Mississippi MHA Request for Short Sale can be viable alternatives to foreclosure, allowing you to sell your home and protect your credit. Always stay proactive in discussing your options with your lender.

Typically, a mortgage lender starts foreclosure proceedings after you miss three consecutive payments. However, this can vary by lender. Taking steps like submitting a Mississippi MHA Request for Short Sale can help you avoid foreclosure by potentially allowing you to sell your home and settle your debts. It's essential to communicate with your lender as soon as you realize you may miss a payment.

The 37 day foreclosure rule in Mississippi states that after a mortgage default, lenders must provide you with a notice of default at least 37 days before initiating foreclosure proceedings. This period gives you an opportunity to address your financial situation. Understanding this rule can be crucial when considering a Mississippi MHA Request for Short Sale. Early intervention can often lead to better outcomes.

The mortgage assistance program in Mississippi aims to support homeowners facing financial difficulties. This program includes options such as the Mississippi MHA Request for Short Sale, which helps distressed homeowners sell their property while potentially reducing or eliminating outstanding mortgage balances. Familiarizing yourself with this program can open doors to solutions tailored to your situation.

Yes, 211 can provide useful information and resources regarding mortgage payments. They can connect you to local financial assistance programs, including options related to the Mississippi MHA Request for Short Sale. If you’re struggling to keep up with payments, reaching out to 211 can be a valuable step towards finding the help you need.

Yes, the Mississippi RAMP program is still available to assist homeowners facing financial hardships. Through this program, you can access resources aimed at helping you keep your home or navigate options like the Mississippi MHA Request for Short Sale. To learn more about what’s currently offered, please check the official state resources or contact your local housing authority for updates.