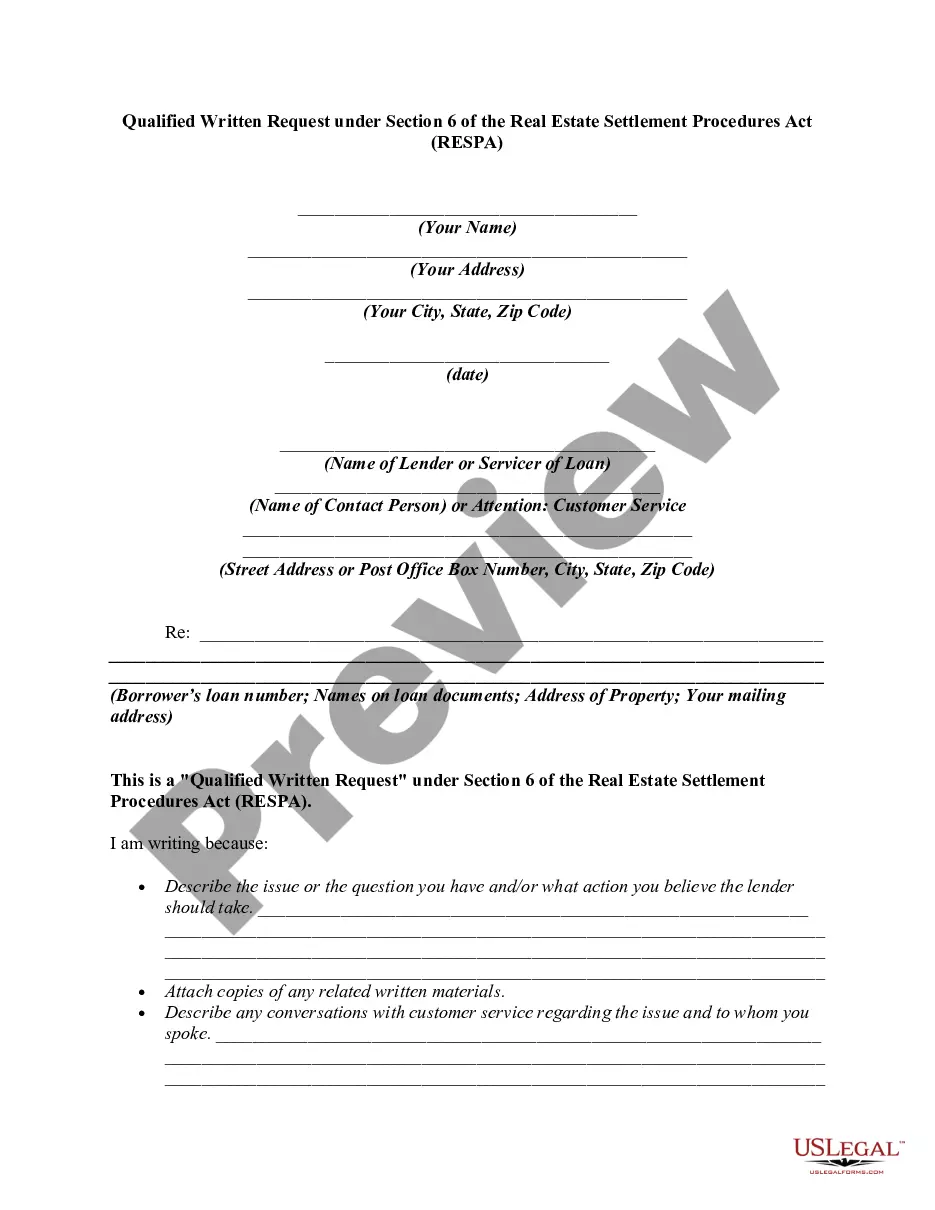

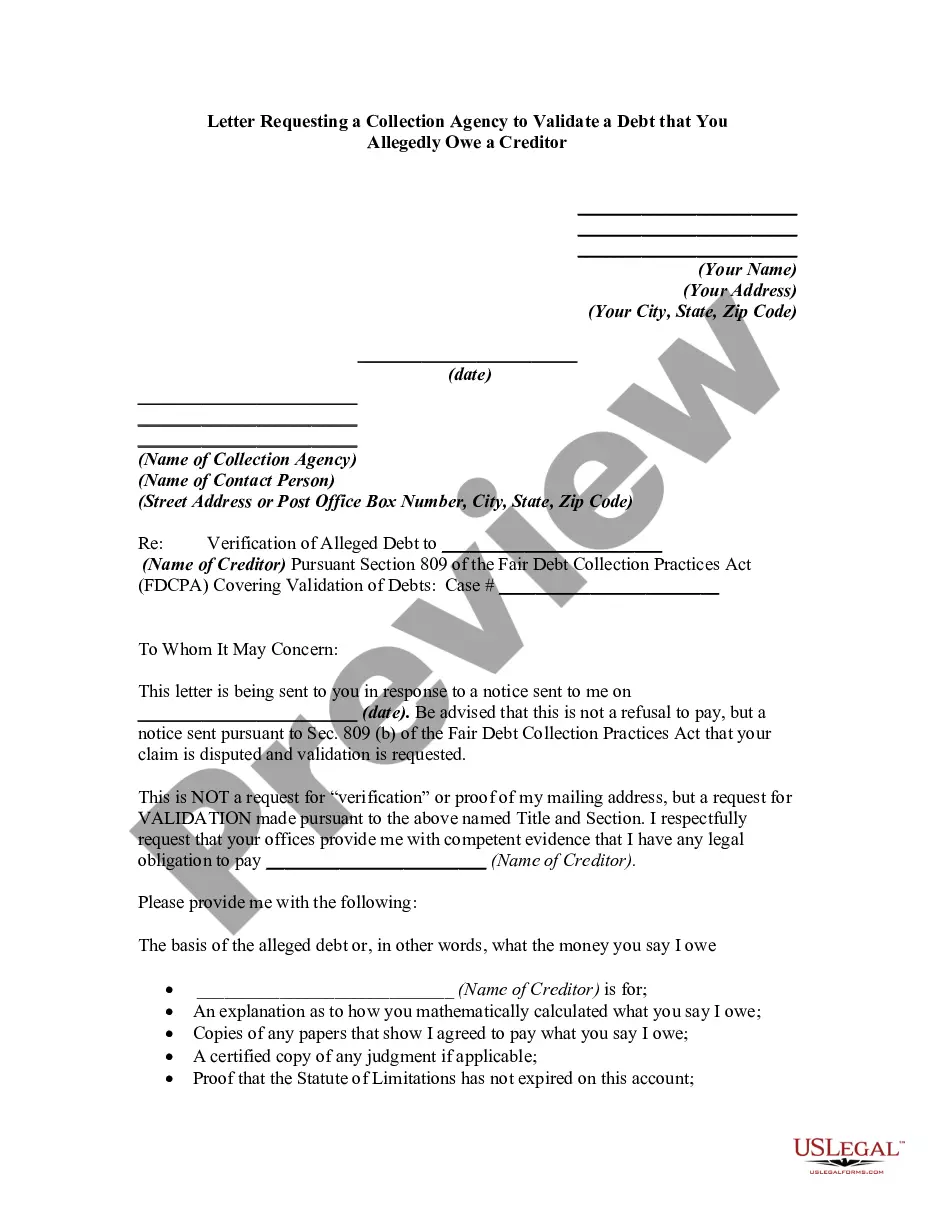

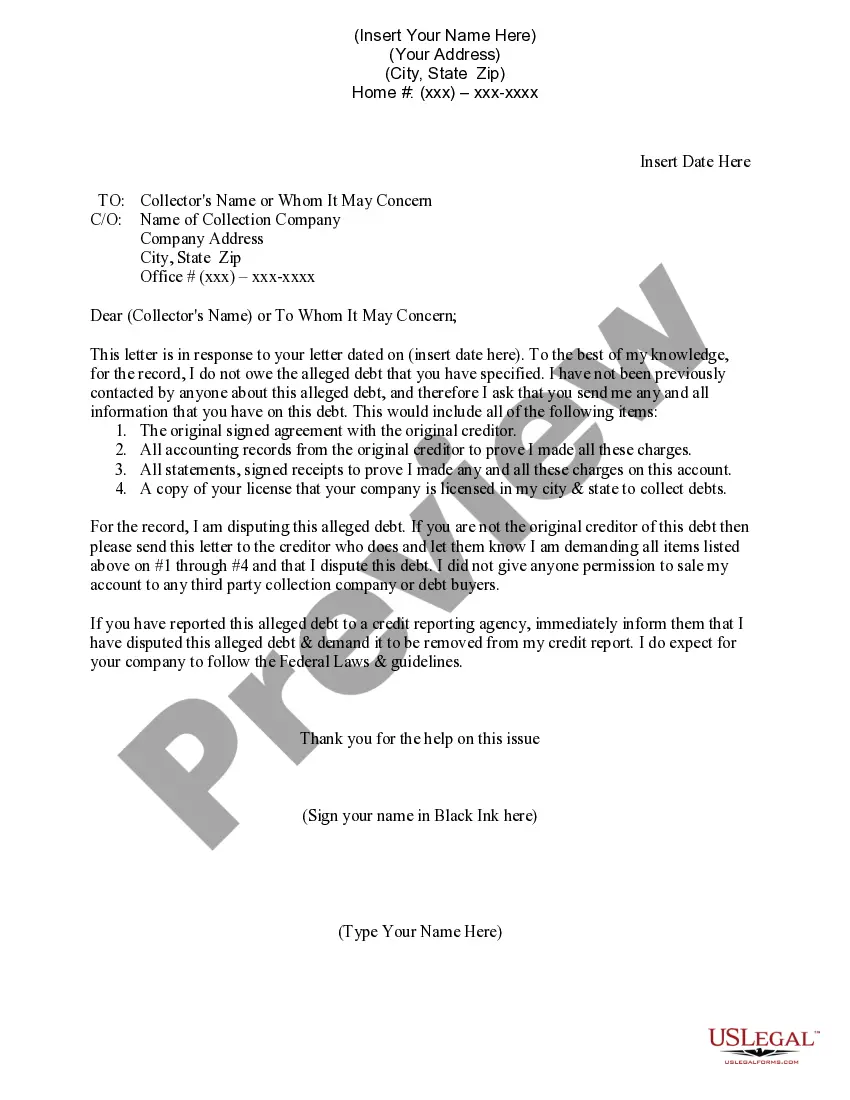

Mississippi Qualified Written RESPA Request to Dispute or Validate Debt

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Qualified Written RESPA Request To Dispute Or Validate Debt?

US Legal Forms - one of the largest collections of legal documents in the United States - provides a diverse range of legal form templates that you can download or create.

By using the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can find the latest versions of forms like the Mississippi Qualified Written RESPA Request to Dispute or Validate Debt in just a few seconds.

If you already have a subscription, Log In and download the Mississippi Qualified Written RESPA Request to Dispute or Validate Debt from your US Legal Forms library. The Download option will be available on every form you view. You can access all previously downloaded forms in the My documents tab of your account.

Make edits. Fill out, modify, print, and sign the downloaded Mississippi Qualified Written RESPA Request to Dispute or Validate Debt.

Every form you add to your account does not expire and is yours indefinitely. If you wish to download or create another copy, simply navigate to the My documents section and click on the form you need. Access the Mississippi Qualified Written RESPA Request to Dispute or Validate Debt with US Legal Forms, the most extensive collection of legal document templates. Utilize a multitude of professional and state-specific templates that meet your business or personal needs and requirements.

- To use US Legal Forms for the first time, here are simple instructions to get started.

- Ensure that you have selected the correct form for your city/state. Click the Preview option to review the form's details. Check the form information to confirm you have selected the appropriate form.

- If the form does not meet your needs, use the Search box at the top of the screen to find one that does.

- Once you are satisfied with the form, confirm your choice by clicking the Purchase now button. Then, select your preferred pricing plan and enter your credentials to register for an account.

- Process the payment. Use your credit card or PayPal account to complete the transaction.

- Choose the format and download the form to your device.

Form popularity

FAQ

To obtain a debt validation letter, you should submit a Mississippi Qualified Written RESPA Request to Dispute or Validate Debt to your creditor or debt collector. This written request should clearly state your demand for validation and include your account information. Once they receive your request, they are required by law to provide you with evidence of the debt. Using platforms like US Legal Forms can simplify this process by providing templates that help you craft an effective request.

Yes, you can dispute a valid debt if you believe there is an error or if the creditor has failed to provide sufficient evidence. Utilizing the Mississippi Qualified Written RESPA Request to Dispute or Validate Debt allows you to formally challenge the details of the debt. It is important to support your claim with any relevant documentation that highlights discrepancies. Addressing concerns in this manner helps protect your rights as a consumer.

When writing a letter to dispute the validity of a debt, begin by clearly stating your full name, address, and the details of the debt you are disputing. Use the Mississippi Qualified Written RESPA Request to Dispute or Validate Debt format to help articulate your request for verification from the creditor. Remember to ask for specific documentation that proves the legitimacy of the debt. This structured approach strengthens your position.

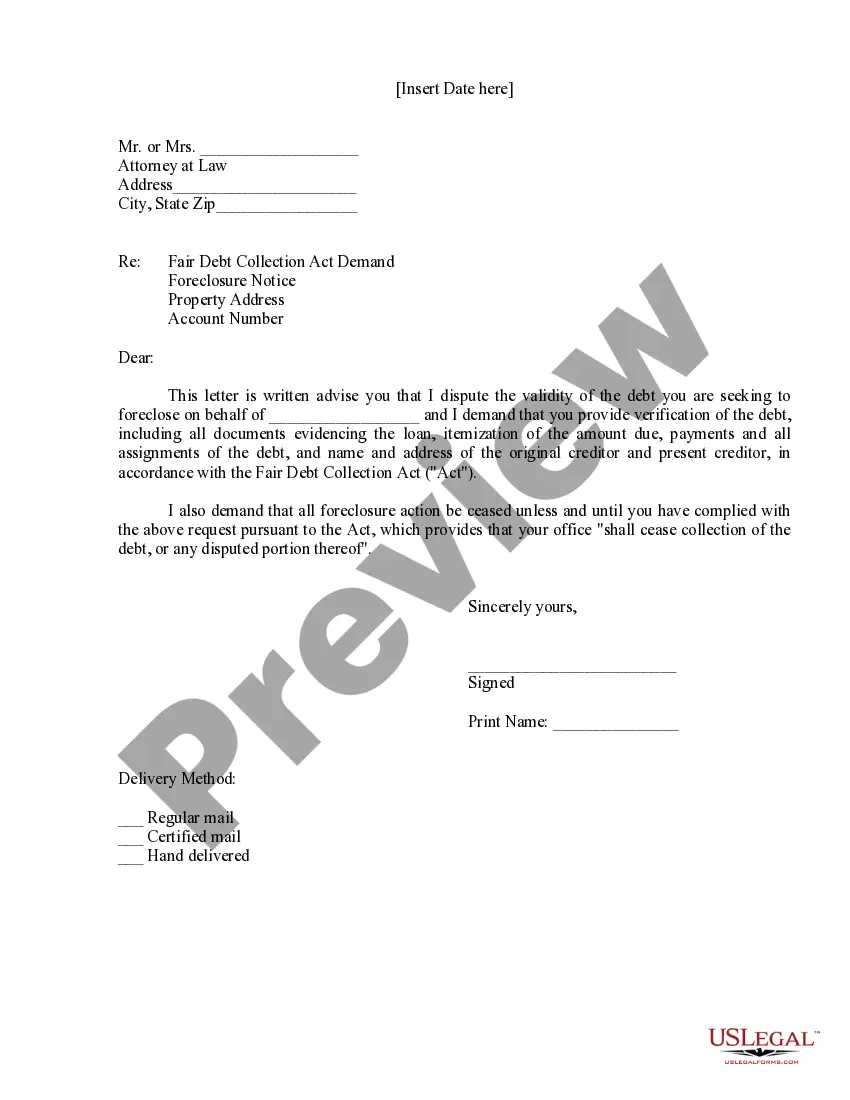

To file a debt validation claim, gather all relevant documentation, including your original contract and any communication with the creditor. Draft a letter following the Mississippi Qualified Written RESPA Request to Dispute or Validate Debt guidelines, clearly stating your intent to dispute the debt. Send your claim via certified mail to ensure it is tracked and receive confirmation of delivery. This process establishes a formal record of your dispute.

When responding to a debt validation letter, review the details provided by the creditor carefully. You may choose to acknowledge the debt if it is valid, or you can dispute it if you find discrepancies. Utilize the Mississippi Qualified Written RESPA Request to Dispute or Validate Debt to structure your response; formally request additional information or clarification as needed. This method demonstrates your diligence in handling the situation.

A strong sample for a debt validation letter includes your name, address, and the details of the debt in question. Use the Mississippi Qualified Written RESPA Request to Dispute or Validate Debt format to guide your structure. Make sure to state your request for verification clearly and ask for any relevant documentation to support the claim. Adopting this format helps you effectively communicate your concerns.

To write a letter disputing a debt, start by clearly stating your request for validation. Include your account information and specify the debt you are disputing. Use the Mississippi Qualified Written RESPA Request to Dispute or Validate Debt format, ensuring you ask the creditor for supporting documentation. This structure keeps your communication clear and effective.

A certified letter to validate debt is a formal communication you send to a debt collector, requesting proof of the debt's legitimacy. This letter provides you with legal backing to inquire about details such as the original creditor and the amount owed. Utilizing a Mississippi Qualified Written RESPA Request to Dispute or Validate Debt in this manner can initialize a thorough review and give you confidence in your dispute. By sending a certified letter, you ensure that you have a record of your request and the collector's response.

A debt collector must provide the written validation notice within five days of their initial contact with you. This notice should inform you about your rights under the Fair Debt Collection Practices Act. It is essential because it allows you to understand the debt details and how to dispute inaccuracies. If you decide to send a Mississippi Qualified Written RESPA Request to Dispute or Validate Debt, this notice is crucial for your process.