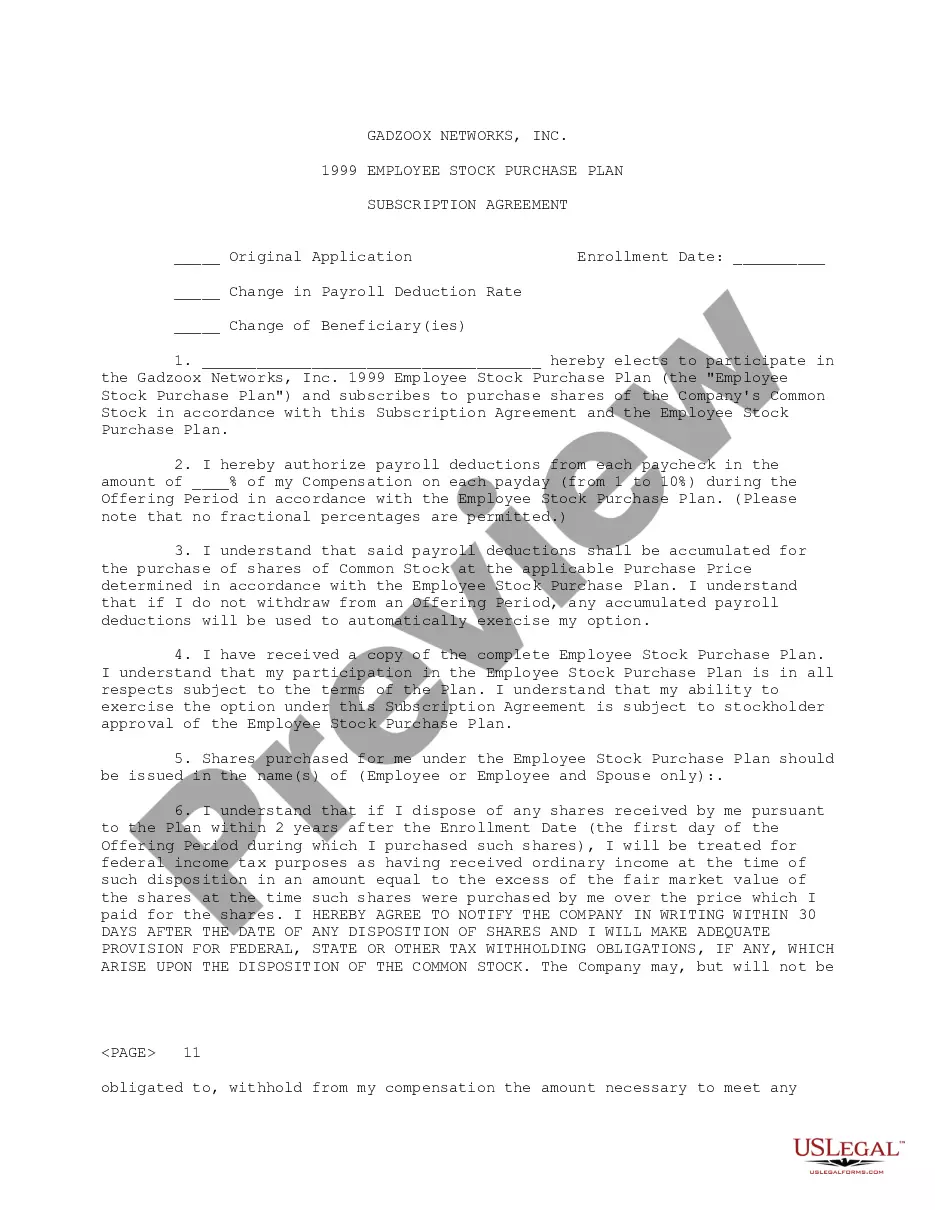

19-119 19-119 . . . Employee Stock Purchase Plan under which each employee can contribute from 1% to 10% of earnings through payroll deductions, and contributions are credited to account maintained on behalf of each employee by brokerage firm designated as custodian under Plan. So long as Plan is operated as "discount plan", corporation will sell shares directly to custodian at a price equal to lesser of 85% of fair market value of common stock at beginning of offering period or 85% of fair market value of common stock on purchase date. If Board designates Plan as a "matching plan", such discounted sales by corporation would be discontinued, but corporation instead would make matching contribution equal to 15% of employees' payroll contributions to be used by custodian to make market purchases of common stock at or promptly after purchase date

Mississippi Employee Stock Purchase Plan of Charming Shoppes, Inc.

Category:

State:

Multi-State

Control #:

US-CC-19-119

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Employee Stock Purchase Plan Of Charming Shoppes, Inc.?

If you need to total, obtain, or printing authorized document layouts, use US Legal Forms, the greatest variety of authorized varieties, that can be found on-line. Make use of the site`s simple and easy hassle-free lookup to find the paperwork you need. Different layouts for business and personal uses are sorted by categories and claims, or keywords and phrases. Use US Legal Forms to find the Mississippi Employee Stock Purchase Plan of Charming Shoppes, Inc. with a handful of clicks.

Should you be presently a US Legal Forms client, log in to the bank account and click the Acquire button to find the Mississippi Employee Stock Purchase Plan of Charming Shoppes, Inc.. Also you can gain access to varieties you formerly saved in the My Forms tab of the bank account.

If you work with US Legal Forms the very first time, refer to the instructions under:

- Step 1. Make sure you have chosen the shape for the proper area/region.

- Step 2. Use the Preview choice to look over the form`s content. Don`t overlook to learn the outline.

- Step 3. Should you be not happy with the form, take advantage of the Research industry on top of the display to discover other versions in the authorized form web template.

- Step 4. When you have found the shape you need, click the Buy now button. Choose the costs strategy you favor and put your accreditations to sign up for the bank account.

- Step 5. Method the transaction. You can use your charge card or PayPal bank account to accomplish the transaction.

- Step 6. Select the structure in the authorized form and obtain it on the device.

- Step 7. Total, edit and printing or sign the Mississippi Employee Stock Purchase Plan of Charming Shoppes, Inc..

Each authorized document web template you get is your own permanently. You possess acces to every form you saved in your acccount. Click the My Forms area and decide on a form to printing or obtain yet again.

Remain competitive and obtain, and printing the Mississippi Employee Stock Purchase Plan of Charming Shoppes, Inc. with US Legal Forms. There are many professional and express-distinct varieties you may use to your business or personal needs.

Form popularity

FAQ

Disadvantages of Employee Stock Purchase Plans Ensuring the ESPP follows security and tax law guidelines can be challenging. A large amount of HR functions goes into administering the stock purchase plan. There are legal, tax, and administrative issues that go into setting up the plan.

5 Ways To Use Your ESPP Contribute To Long Term Wealth. Contributing to an ESPP can boost your efforts towards building wealth through long-term investing. ... Reinvest Into A Roth IRA. An ESPP can be an avenue to fund a Roth IRA. ... Supplement Cash Flow. ... Short Term Savings Goals. ... Pay down debt.

You may withdraw from the ESPP by notifying Fidelity and completing a withdrawal election. When you withdraw, all of the contributions accumulated in your account will be returned to you as soon as administratively possible and you will not be able to make any further contributions during that offering period.

With 49 percent of the S&P 500 companies and 38.5 percent of Russell 3000 companies offering ESPPs to their employees, competition for top talent is fierce. By offering the opportunity to participate in the company's ownership, employees may feel more loyal and invested in the company's success.

How does a withdrawal work in an ESPP? With most employee stock purchase plans, you can withdraw from your plan at any time before the purchase. Withdrawals are made on Fidelity.com or through a representative. However, you should refer to your plan documents to determine your plan's rules governing withdrawals.

An employee stock purchase plan is an employer-sponsored incentive plan that allows employees to purchase company stock. Under such a plan, the employer offers its employees the option to purchase company stock at the end of an ?offering period,? which typically ranges between 3 months and 27 months.

An ESPP may be worth considering if you're already meeting your other financial goals, such as maxing out your 401(k), investing in a brokerage account, paying off debt or other savings goals, McKenna said.

You can sell your ESPP plan stock immediately to lock in your profit from the discount. You pay lower taxes if you hold the company stock for at least a year and sell it for more than two years after the offering date. However, there are risks to participating in an employee stock purchase program.

You will continue to own stock purchased for you during your employment, but your eligibility for participation in the plan ends. Any funds withheld from your salary but not used to purchase shares before the end of your employment will be returned to you, normally without interest, within a reasonable period.

The bottom line on ESPPs If you can afford it, you should participate up to the full amount and then sell the shares as soon as you can. You might even consider prioritizing your ESPP over 401(k) contributions, depending on your specific financial situation, because your after-tax returns could be higher.