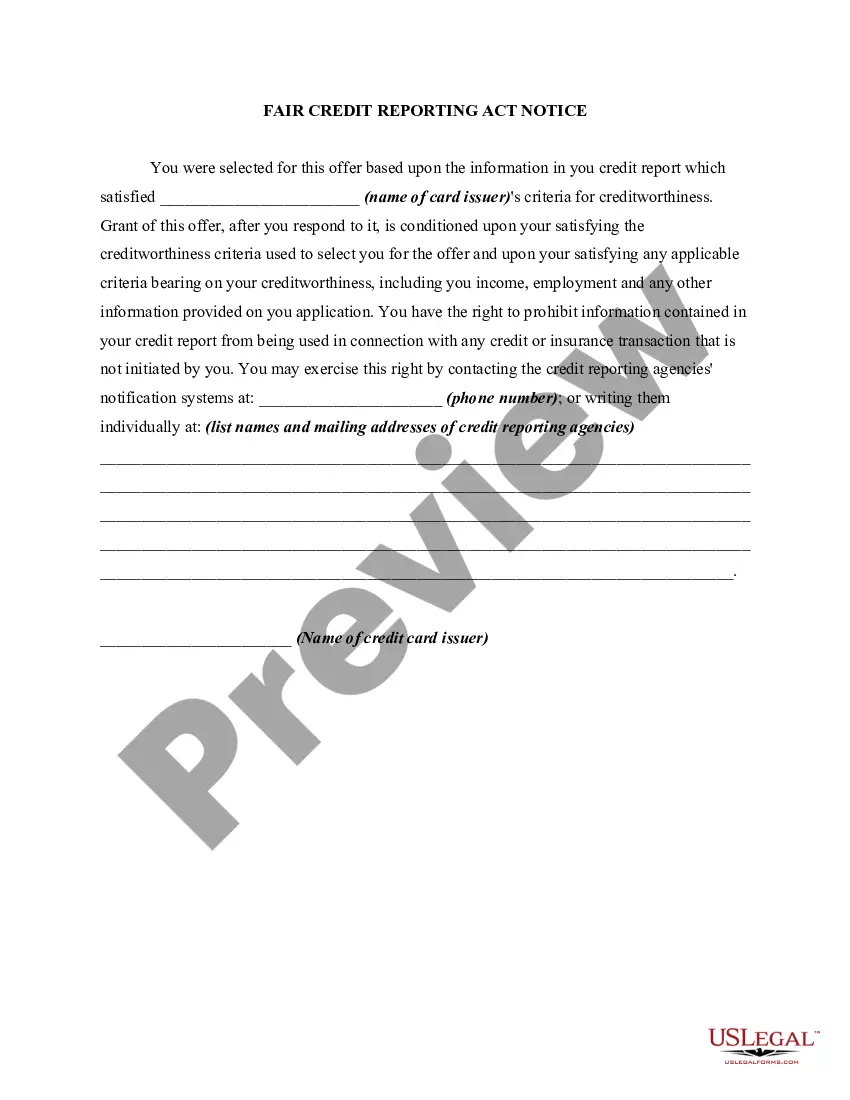

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information. If such a request is made and is received within 60 days after the consumer learned of the adverse action, the user, within a reasonable period of time, must disclose to the consumer the nature of the information.

Mississippi Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency

Description

How to fill out Notice Of Increase In Charge For Credit Based On Information Received From Person Other Than Consumer Reporting Agency?

You may invest hrs on-line looking for the legitimate record web template that fits the federal and state requirements you need. US Legal Forms supplies a large number of legitimate forms which are examined by professionals. You can actually obtain or print out the Mississippi Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency from my services.

If you have a US Legal Forms accounts, you may log in and click on the Acquire button. Next, you may complete, edit, print out, or indication the Mississippi Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency. Each legitimate record web template you buy is the one you have permanently. To obtain yet another duplicate associated with a purchased form, visit the My Forms tab and click on the corresponding button.

If you work with the US Legal Forms website the first time, adhere to the straightforward recommendations below:

- Initially, ensure that you have chosen the right record web template to the state/metropolis of your liking. Read the form information to make sure you have picked the proper form. If accessible, utilize the Preview button to search through the record web template at the same time.

- If you want to find yet another version from the form, utilize the Look for discipline to get the web template that meets your needs and requirements.

- After you have identified the web template you need, click Get now to carry on.

- Find the pricing plan you need, enter your accreditations, and register for a free account on US Legal Forms.

- Comprehensive the transaction. You should use your bank card or PayPal accounts to fund the legitimate form.

- Find the formatting from the record and obtain it in your system.

- Make alterations in your record if needed. You may complete, edit and indication and print out Mississippi Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency.

Acquire and print out a large number of record templates while using US Legal Forms site, which provides the biggest assortment of legitimate forms. Use professional and status-particular templates to handle your company or personal requirements.

Form popularity

FAQ

A Credit Score Disclosure alerts a consumer of their FICO scores, defines what a FICO is, informs how FICO scores affect their access to consumer credit and provides contact information for the bureaus.

Risk-based pricing occurs when lenders offer different interest rates and loan terms to borrowers, based on individual creditworthiness. The Risk-Based Pricing Rule requires you to notify consumers if they are getting worse terms because of information in their credit report.

These higher rates increase the burden of any given level of debt, making it more difficult to repay and, therefore, increasing the likelihood of default. Risk-based pricing is often a self-fulfilling prophecy. The feedback loop created by risk-based pricing is destabilizing to financial markets.

With risk-based pricing, you pay more or less interest depending on the lender's evaluation of the risk they would be exposed to by lending to you. If you're a safe bet and the lender is all but certain you'll repay, you'll qualify for the best products and lower interest rates.

Duty to Promptly Correct and Update Information. Section 623(a) of the FCRA also requires a person who regularly furnishes information to CRAs to promptly notify a CRA if the person determines the previously furnished information is not complete or accurate.

Common violations of the FCRA include: Creditors give reporting agencies inaccurate financial information about you. Reporting agencies mixing up one person's information with another's because of similar (or same) name or social security number.

Risk-based pricing refers to the practice of setting or adjusting the interest rate and other terms of credit provided to a particular consumer based on the consumer's credit data and other factors used to measure risk.

Risk-based pricing occurs when lenders offer different consumers different interest rates or other loan terms, based on the estimated risk that the consumers will fail to pay back their loans.