Mississippi Limited Partnership Agreement

Understanding this form

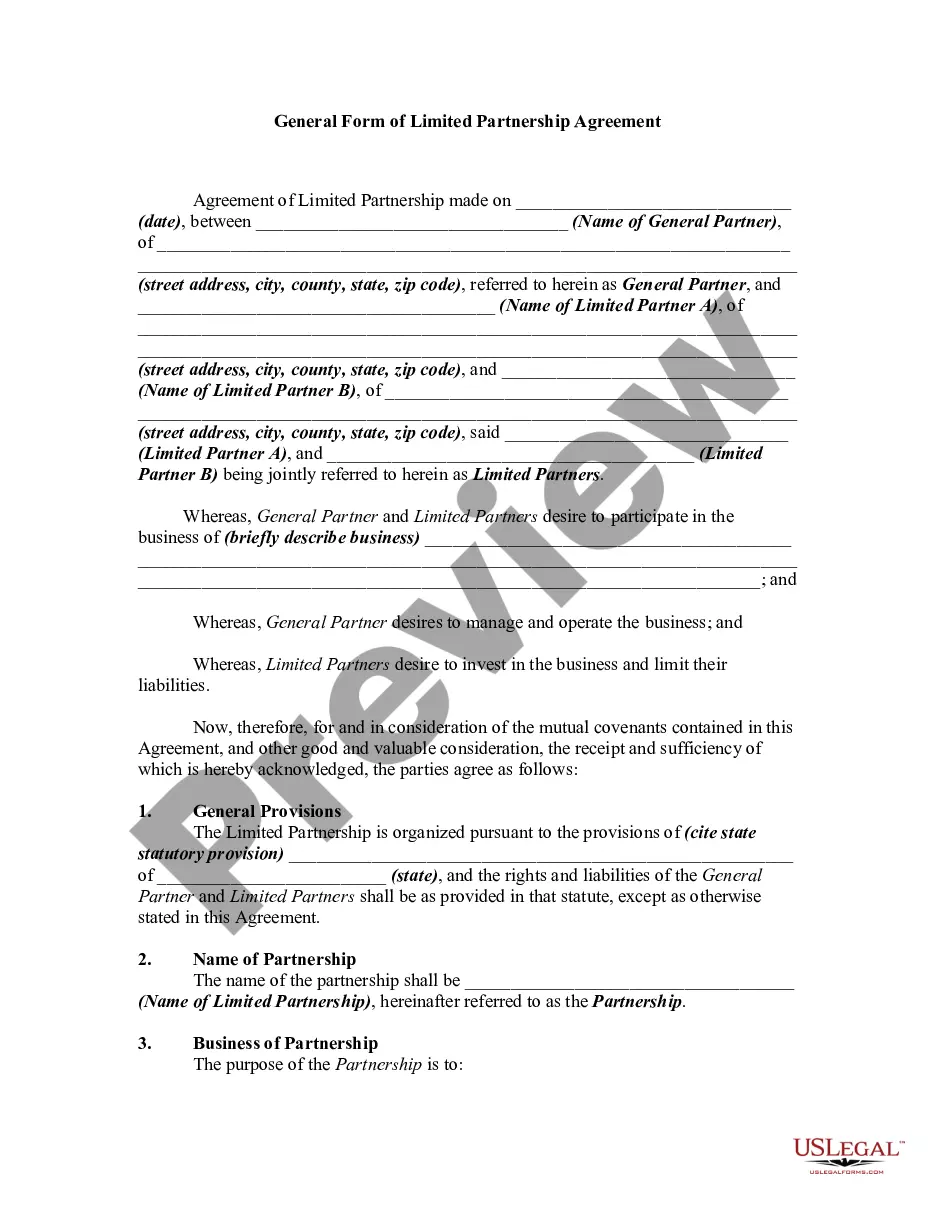

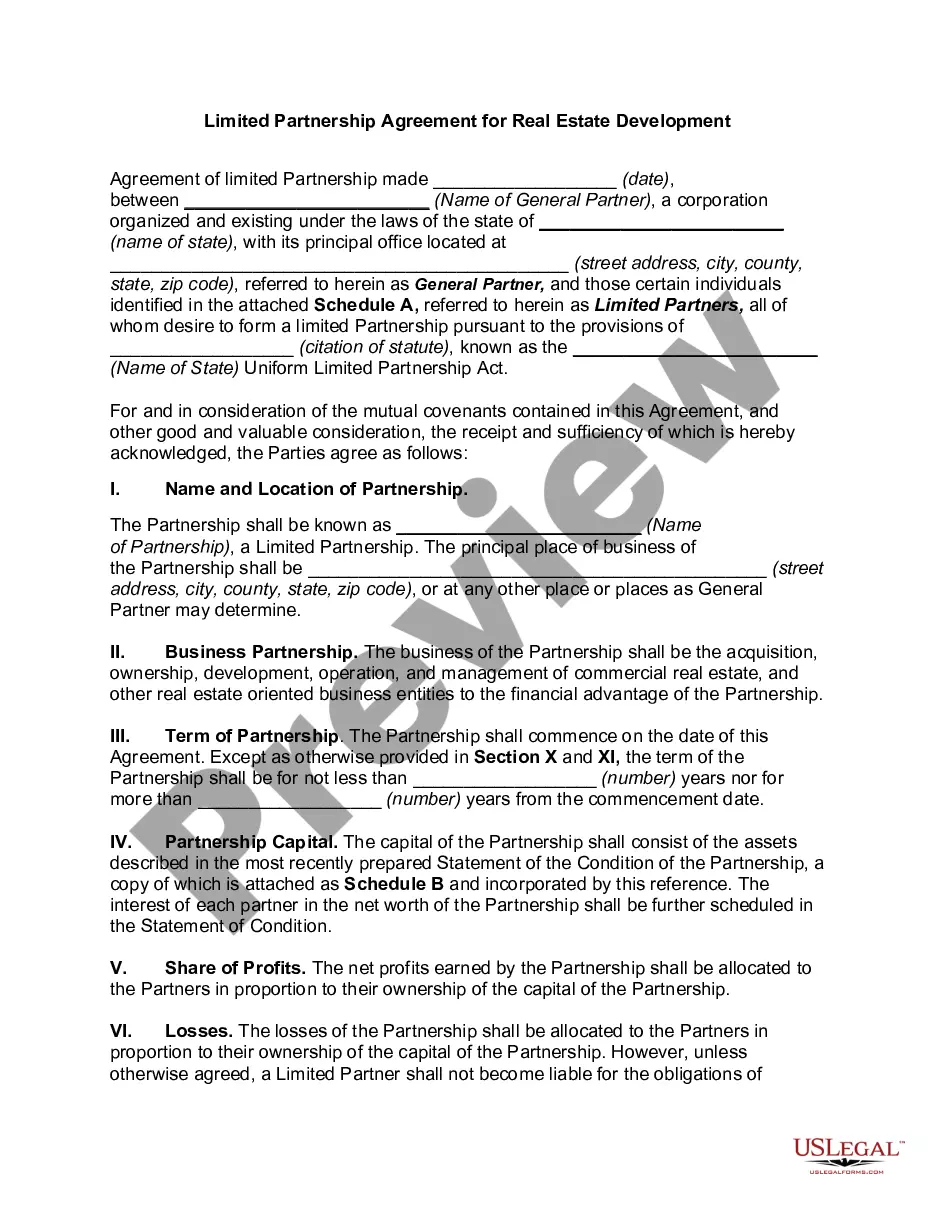

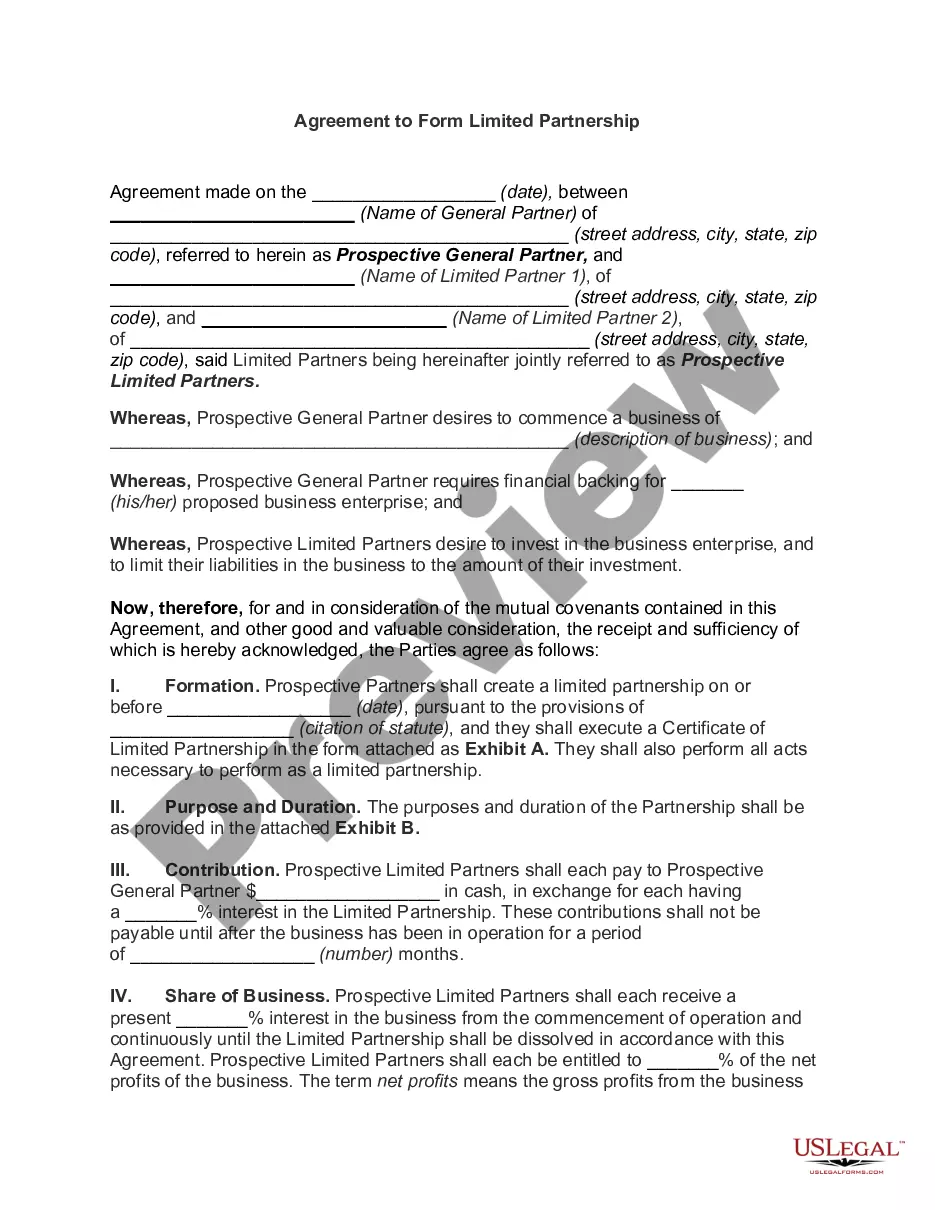

The Limited Partnership Agreement is a legal document that establishes a limited partnership under the Mississippi Uniform Limited Partnership Act. This form outlines the rights and responsibilities of general and limited partners, including provisions for capital contributions, profit distribution, and management structure. Unlike general partnership agreements, this form provides limited partners with protection against liabilities beyond their investment in the partnership.

Key parts of this document

- Formation details, including the name and principal place of business of the limited partnership.

- Capital contributions, outlining initial investments and policies for withdrawals or loans.

- Profit and loss allocation, specifying how earnings and losses are distributed among partners.

- Management responsibilities, detailing the roles of general partners and limitations on the liability of limited partners.

- Transfer of partnership interest, addressing conditions under which interests can be bought or sold.

- Dissolution procedures for terminating the partnership and distributing assets.

When to use this form

This form is necessary when individuals or entities wish to establish a limited partnership in Mississippi. It is particularly useful for businesses seeking to limit the liability of some partners while allowing others to manage the company. Scenarios include forming a real estate investment group or pooling resources for a business venture where some investors desire limited involvement.

Who this form is for

- Business owners looking to form a limited partnership in Mississippi.

- Individuals who want to invest in a business but limit their liability exposure.

- Partners who will manage the business and seek a formal agreement detailing roles and responsibilities.

- Investors who require a clear understanding of profit sharing and asset distribution before committing funds.

Completing this form step by step

- Identify the partners involved, including general and limited partners.

- Specify the name of the partnership and its principal place of business.

- Outline initial capital contributions from each partner and any conditions for withdrawal.

- Detail how profits and losses will be calculated and allocated among the partners.

- Include provisions for the transfer of partnership interests and the process for dissolution.

Is notarization required?

This form does not typically require notarization unless specified by local law. It is advisable to check with a legal professional regarding any specific requirements for your partnership agreement in Mississippi.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to properly outline the roles and responsibilities of general and limited partners.

- Not specifying how profits and losses are to be distributed, leading to potential disputes.

- Omitting necessary details related to the transfer of partnership interests.

- Neglecting to comply with state-specific laws regarding limited partnerships.

Benefits of using this form online

- Convenient access to professionally drafted legal templates tailored to Mississippi law.

- Editable format, allowing users to customize the agreement to meet specific partnership needs.

- Secure and instant download, enabling quick establishment of the partnership arrangement.

The Limited Partnership Agreement is enforceable in Mississippi as long as it complies with the stateâs regulations. It is essential to ensure that all partners understand their rights and obligations defined in the agreement to prevent disputes.

Key takeaways

- The Limited Partnership Agreement outlines the structure and operational guidelines for a limited partnership in Mississippi.

- Properly completing this form helps protect personal assets while engaging in business with partners.

- Understanding the roles of general and limited partners is crucial for effective partnership management.

- Limited Partnership: A partnership consisting of at least one general partner and one limited partner.

- General Partner: A partner responsible for managing the partnership's operations and is liable for its debts.

- Limited Partner: A partner who invests capital in the partnership but has limited liability and does not participate in management.

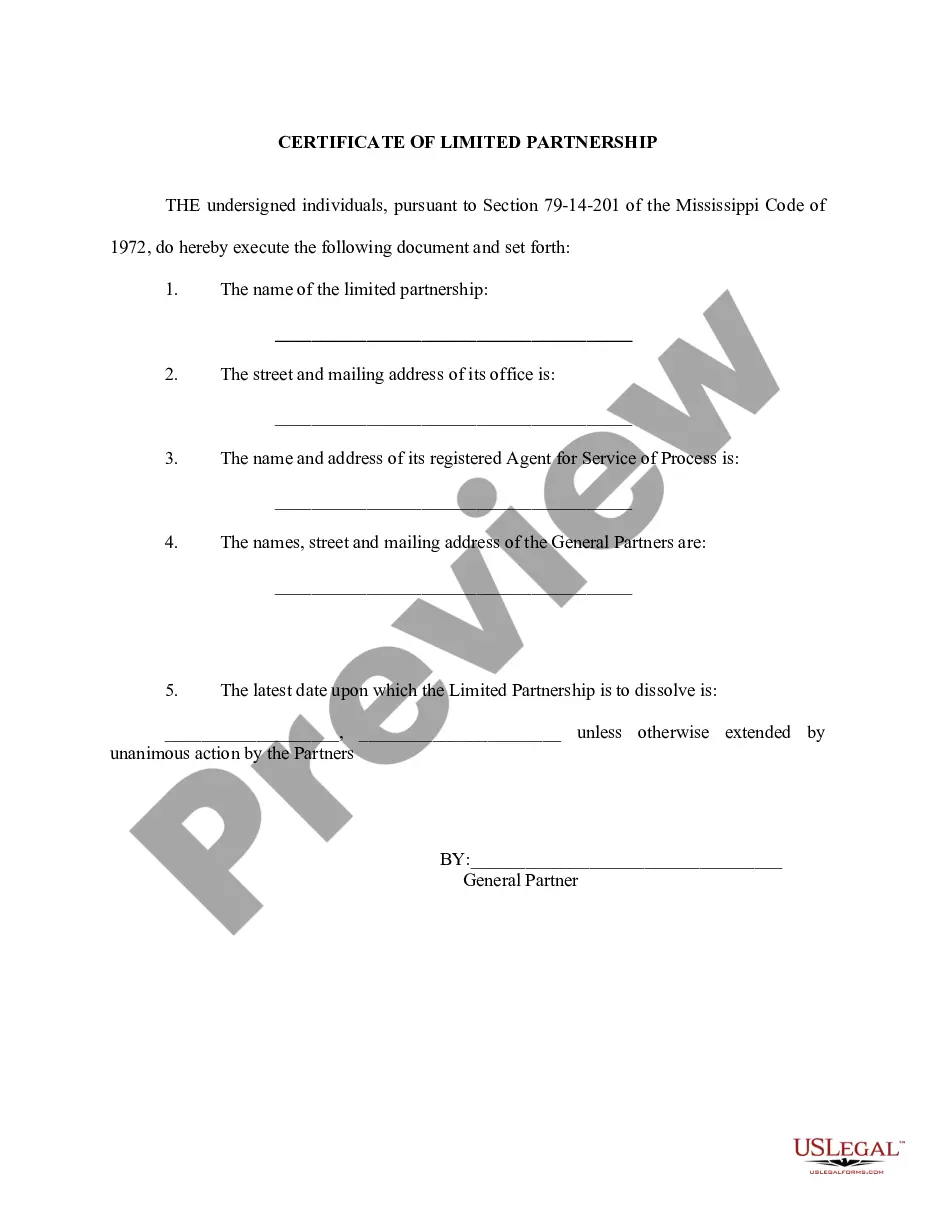

- Certificate of Limited Partnership: Official documents filed with the state to register a limited partnership.

Looking for another form?

Form popularity

FAQ

Any type of business agreement between two or more people can be considered a partnership.Typically, the terms general partner and limited partner in all types of partnerships will refer to liability, with general partners pledging their own personal assets while limited partners having limited liabilities.

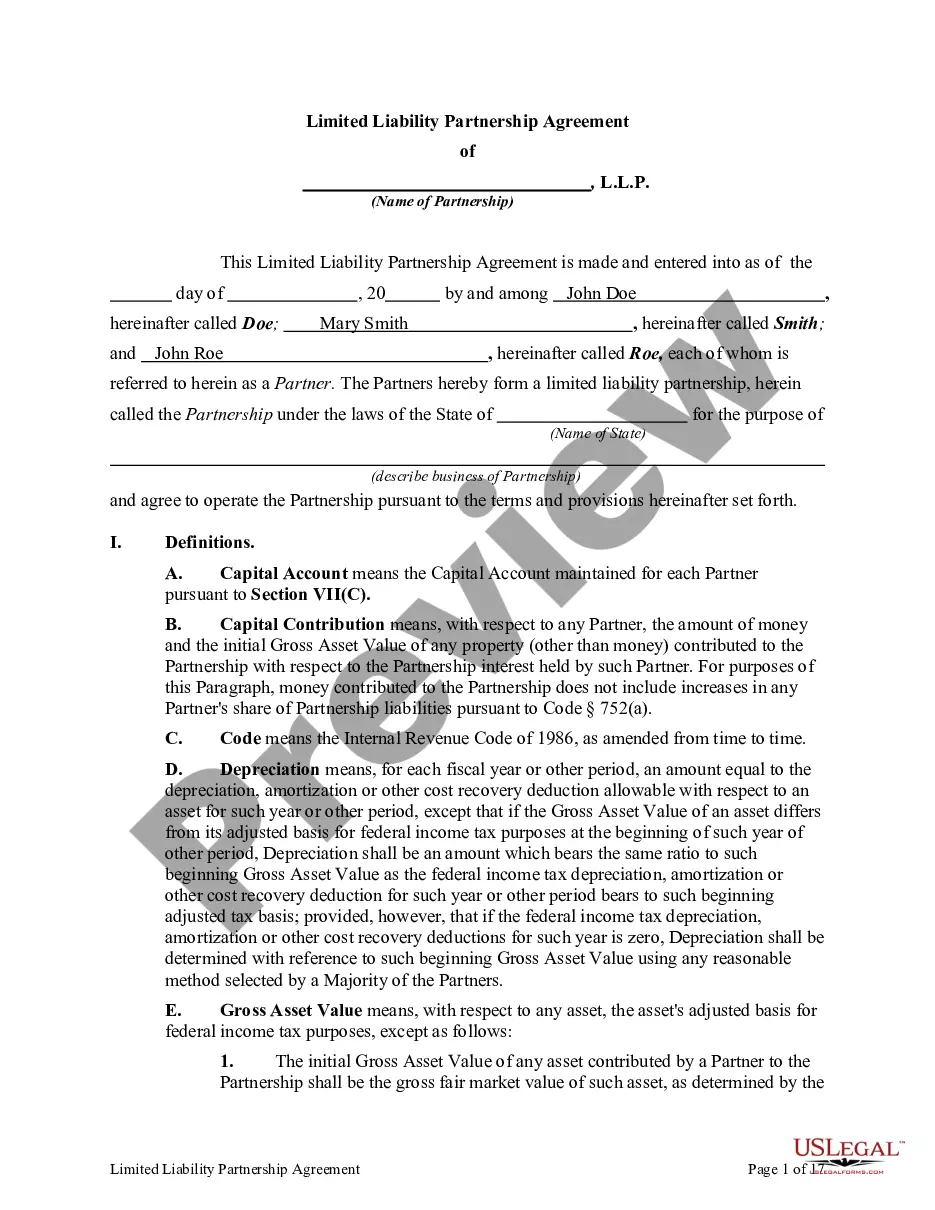

A limited liability partnership (LLP) is a type of partnership where all partners have limited liability. All partners can also partake in management activities. This is unlike a limited partnership, where at least one general partner must have unlimited liability and limited partners cannot be part of management.

In limited partnerships (LPs), at least one of the owners is considered a "general" partner who makes business decisions and is personally liable for business debts.The limited liability partnership (LLP) is a similar business structure but it has no general partners.

A partnership operating agreement is a document that outlines the roles, responsibilities, and rights of the owners and managers of a partnership. It states the rules and regulations governing many aspects of the organization, ranging from voting powers to profit and loss distribution.

An LLC member can enjoy limited liability and yet still participate actively in the LLC's management. This situation was never contemplated when Congress created the self-employment tax limited partner exception, because at that time active participation by a partner would always mean unlimited liability.

Corporations are required by law to file their articles of incorporation with the secretary of state or similar business filing authority.Limited liability companies, on the other hand, are not always required by law to have an operating agreement or file the agreement with the business filing authority.

A partnership agreement is used for partnerships whereas an operating agreement is used for Limited Liability Companies (LLC's). A corporation has minutes. These determinations are made under State law and how the entity is treated for federal income tax purposes does not matter.

Extensive Documentation Required. Lack of Legal Distinction for General Partners. General Partners' Personal Assets Unprotected. General Partners Liable for Each Others' Actions. Less Protection from Excessive Taxation.

An LLP can have two partners or 2,000 partners. A two-person LLP can operate informally with the partners discussing operational items on a case-by-case basis. Larger firms cannot. For example, Grant Thornton LLP, the U.S. division of an international accounting firm, has over 2,600 partners.