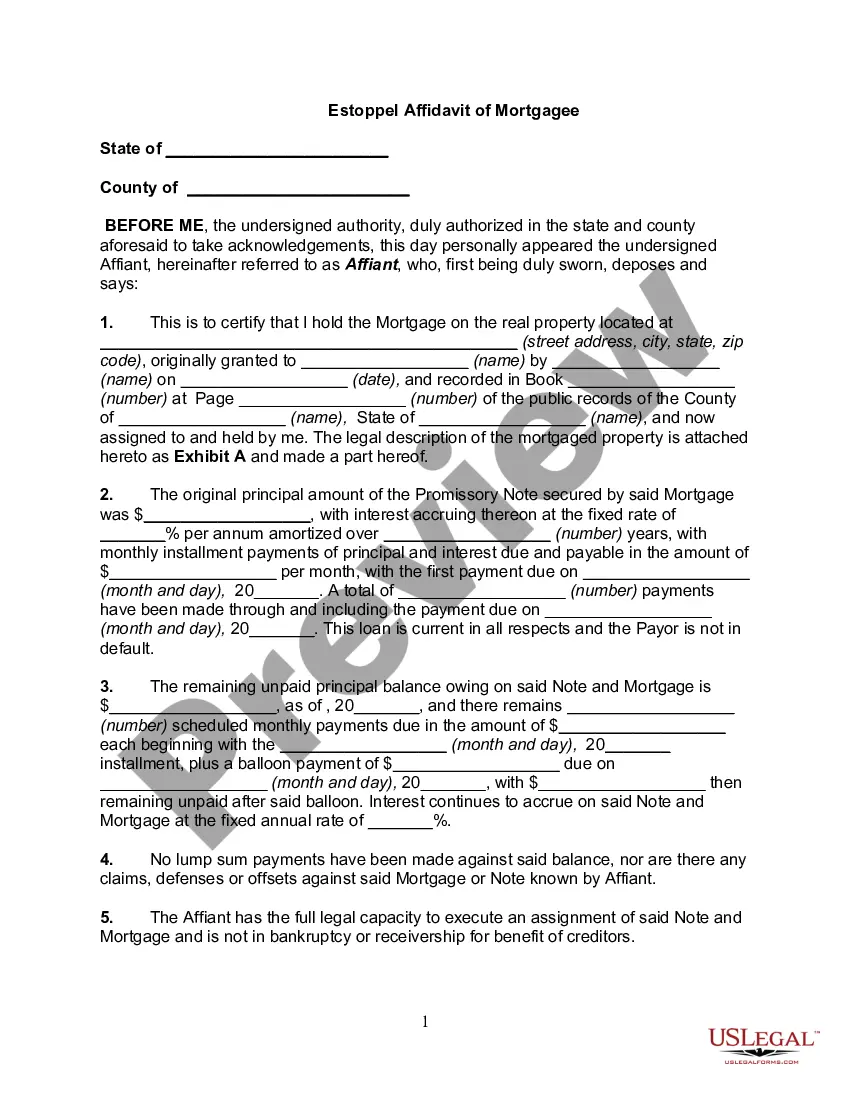

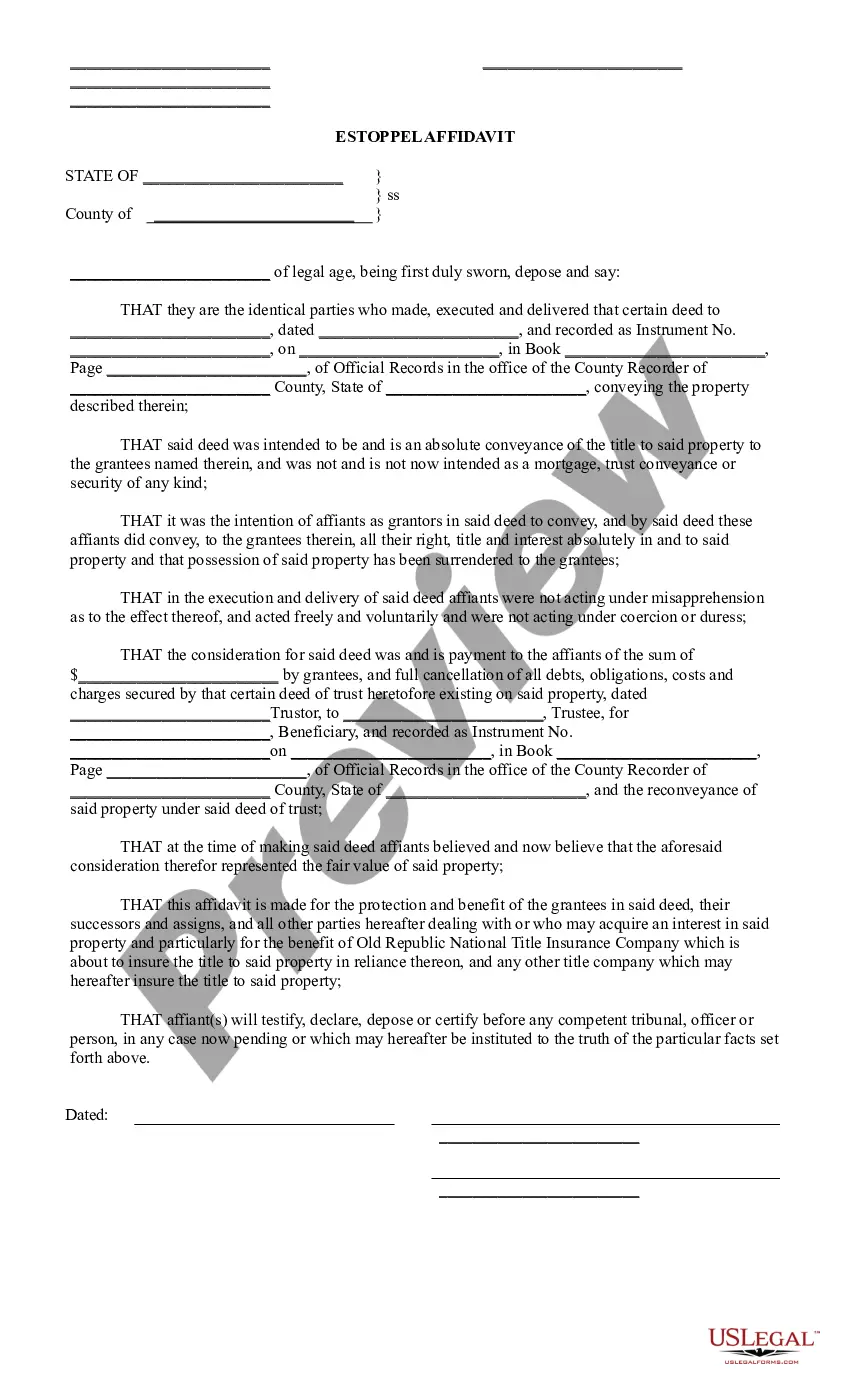

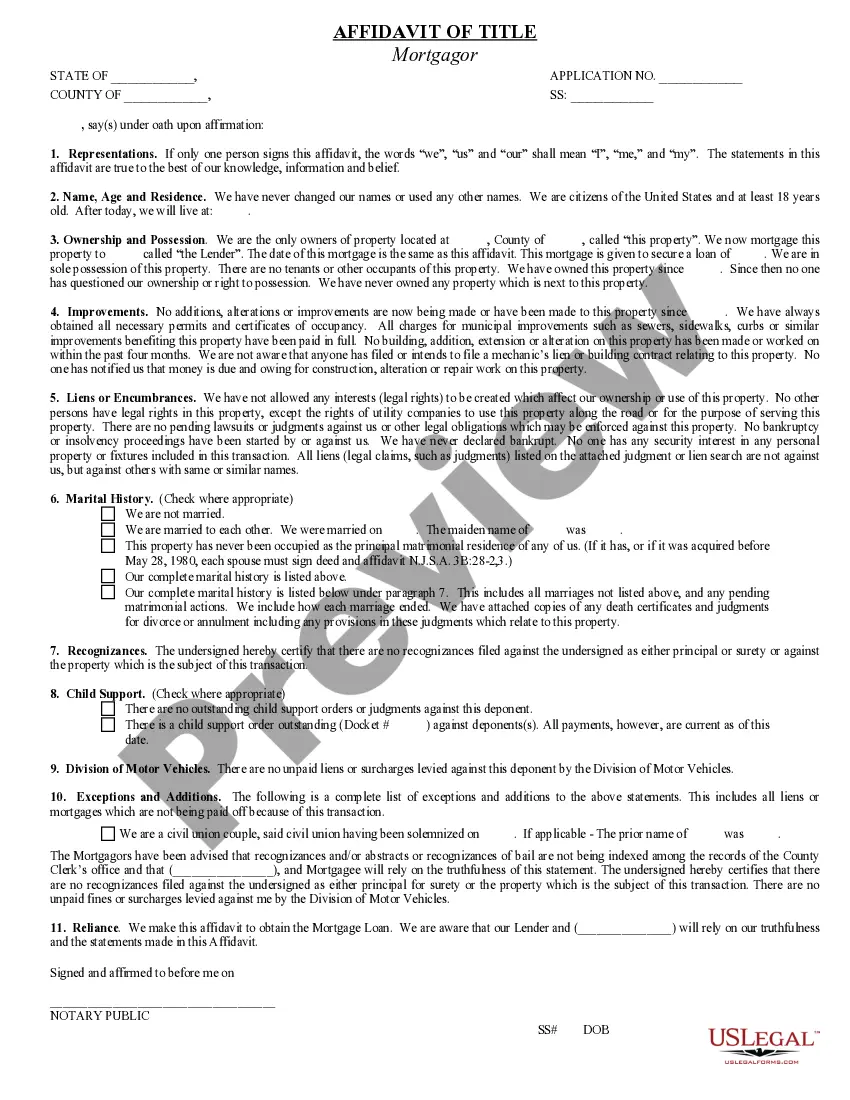

Missouri Estoppel Affidavit of Mortgagor

Description

How to fill out Estoppel Affidavit Of Mortgagor?

US Legal Forms - one of the largest compilations of legal documents in the United States - offers a broad selection of legal document templates you can obtain or create.

By utilizing the site, you can access thousands of forms for business and individual purposes, categorized by types, states, or keywords.

You can obtain the latest versions of documents such as the Missouri Estoppel Affidavit of Mortgagor in just a few minutes.

Check the document description to confirm that you have chosen the right document.

If the document does not meet your requirements, utilize the Search field at the top of the screen to find the one that does.

- If you are a registered user, Log In and obtain the Missouri Estoppel Affidavit of Mortgagor from the US Legal Forms library.

- The Download button will appear on each document you view.

- You can access all previously saved documents in the My documents section of your profile.

- If you are new to using US Legal Forms, here are straightforward instructions to help you begin.

- Ensure you have selected the correct document for your locality/region.

- Click on the Preview button to review the document's content.

Form popularity

FAQ

One clear disadvantage of a deed in lieu of foreclosure is that it may not resolve all financial obligations tied to the property. Homeowners may still be responsible for existing liens or unsecured debts. Using a resource like a Missouri Estoppel Affidavit of Mortgagor can clarify what you owe, helping you avoid surprises down the line.

A deed in lieu of foreclosure typically results in a negative impact on your credit score, although it may be less severe than a full foreclosure. This record can stay on your credit report for up to seven years, affecting your ability to obtain loans. Knowing the details can help you navigate this better, and having a Missouri Estoppel Affidavit of Mortgagor may demonstrate your willingness to move forward responsibly.

A major disadvantage for lenders accepting a deed in lieu of foreclosure is the risk of underlying liens or claims against the property. If these are not disclosed, lenders may face legal and financial issues down the road. This is why lenders often prefer a well-documented option like a Missouri Estoppel Affidavit of Mortgagor, which can provide clearer information on the property's status.

One significant disadvantage of a deed in lieu of foreclosure is the impact it has on your credit score. This option may still leave a mark on your credit report, making future borrowing more challenging. It’s crucial to understand the implications fully and consider using a Missouri Estoppel Affidavit of Mortgagor to make your financial standing clear.

Lenders often prefer a deed in lieu of foreclosure because it simplifies the process. It allows them to avoid the lengthy and costly legal proceedings associated with foreclosure. By accepting a deed in lieu, they quickly reclaim the property and can minimize losses, especially when a Missouri Estoppel Affidavit of Mortgagor outlines clear terms.

Yes, you can buy a house after a deed in lieu of foreclosure, but it may take some time. Generally, lenders may require a waiting period before you can qualify for a new mortgage. Additionally, using a Missouri Estoppel Affidavit of Mortgagor can help clarify your financial situation and improve your standing for future home purchases.

In Virginia, similar to Missouri, a deed in lieu of foreclosure serves as a means for borrowers to willingly relinquish their property to the lender to settle mortgage issues. This can provide an efficient way to avoid foreclosure, minimizing the negative impact on one's credit record. If you're navigating this option, consider the benefits of a Missouri Estoppel Affidavit of Mortgagor, as it helps outline any remaining responsibilities after the property transfer. Platforms like US Legal Forms can assist you in drafting the necessary documents to ensure everything is completed correctly.

A deed in lieu of foreclosure is a legal agreement where a borrower transfers ownership of their property to the lender to avoid foreclosure. This process may be subject to terms related to the existing mortgage, including liens or other obligations. It is important to understand how this transfer affects your financial situation and credit standing. Users can benefit from a Missouri Estoppel Affidavit of Mortgagor to clarify any outstanding issues and ensure a smooth transaction.