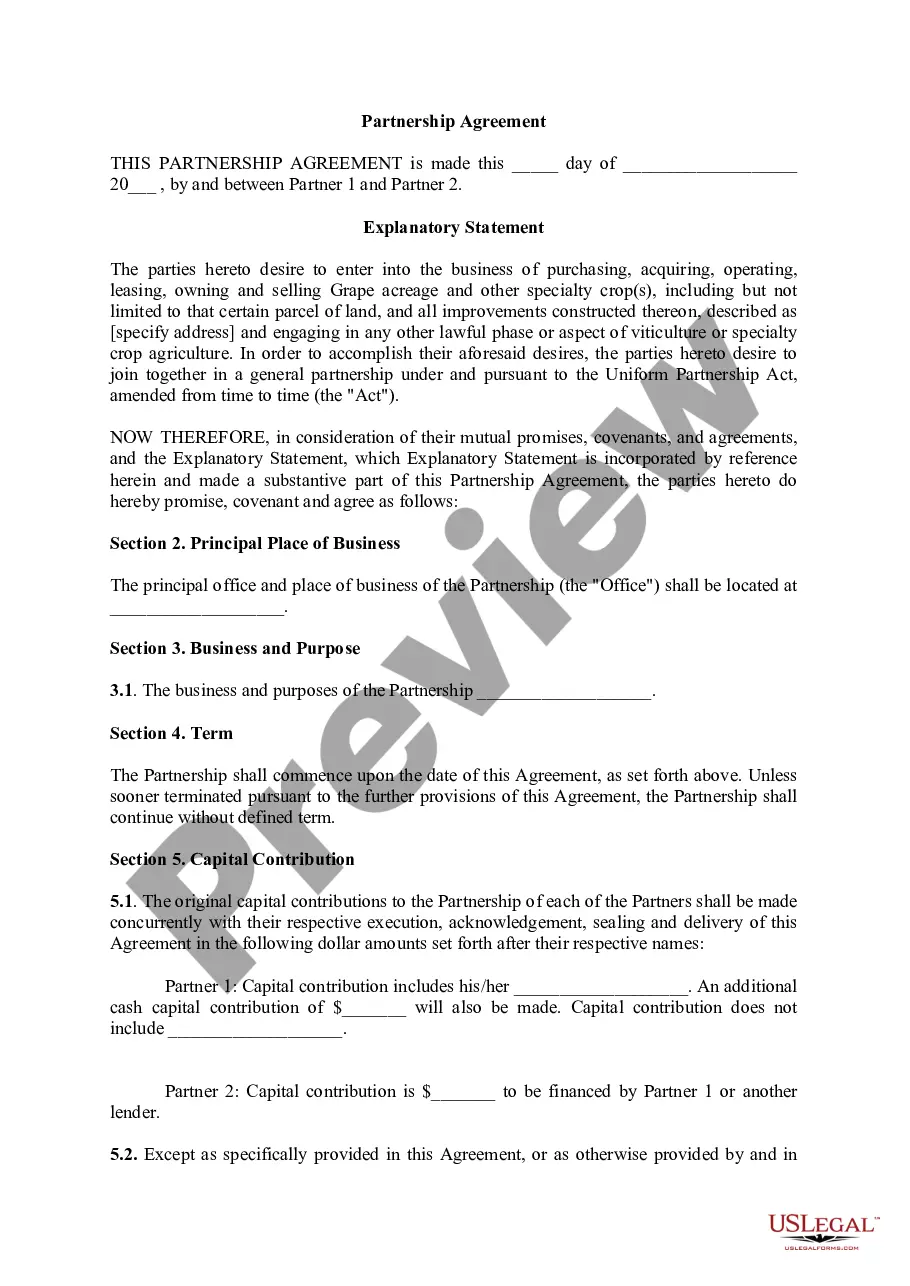

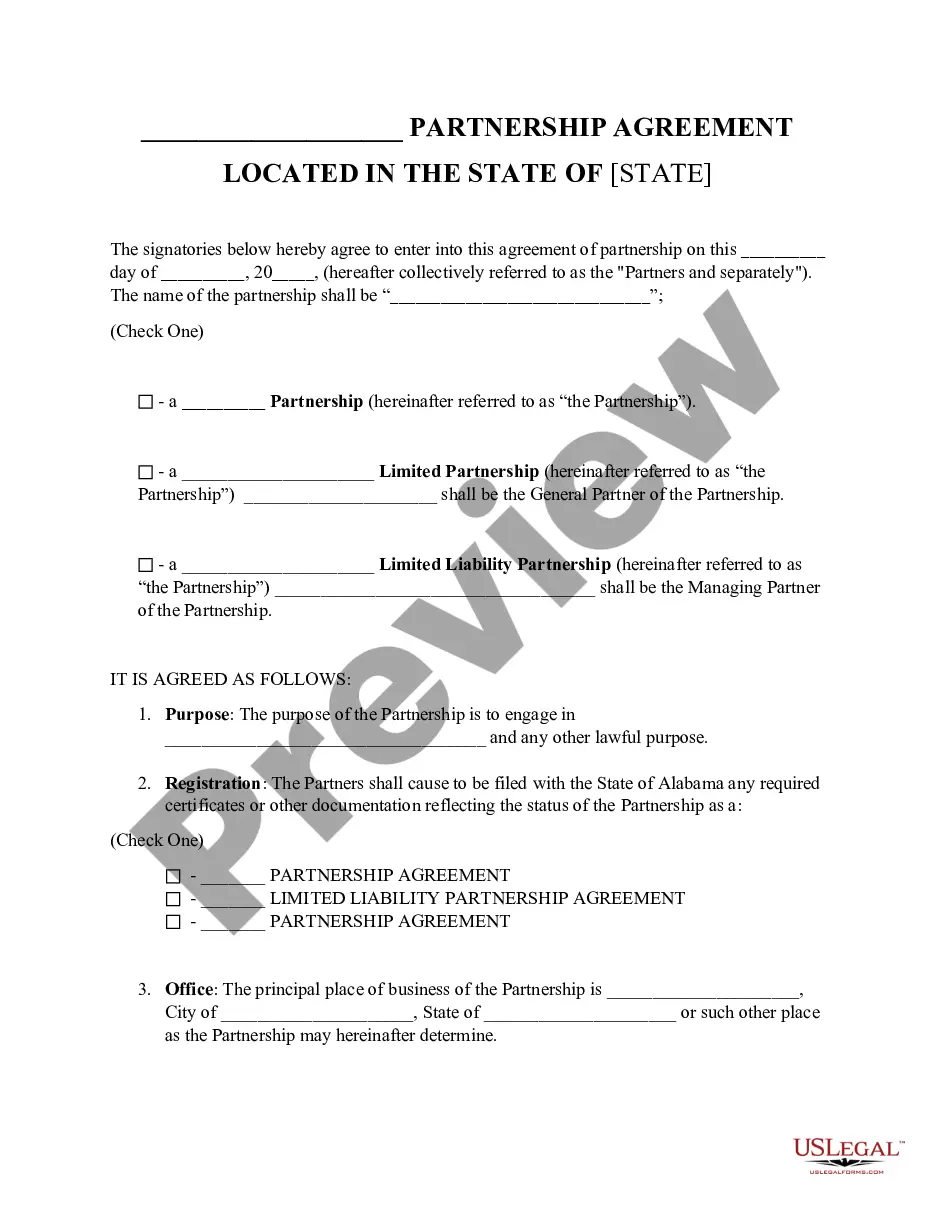

Partnership Agreement for LLC

Understanding this form

The Partnership Agreement for LLC is a legal document that establishes the terms of the partnership among members of a Limited Liability Company (LLC). It outlines the ownership shares of each partner, the contributions they make, and the management structure of the partnership. This form is essential for ensuring that all partners are in agreement regarding their roles and responsibilities, thereby preventing disputes in the future. Unlike general partnership agreements, this one is tailored specifically for LLCs, taking into account their unique legal and operational characteristics.

Key parts of this document

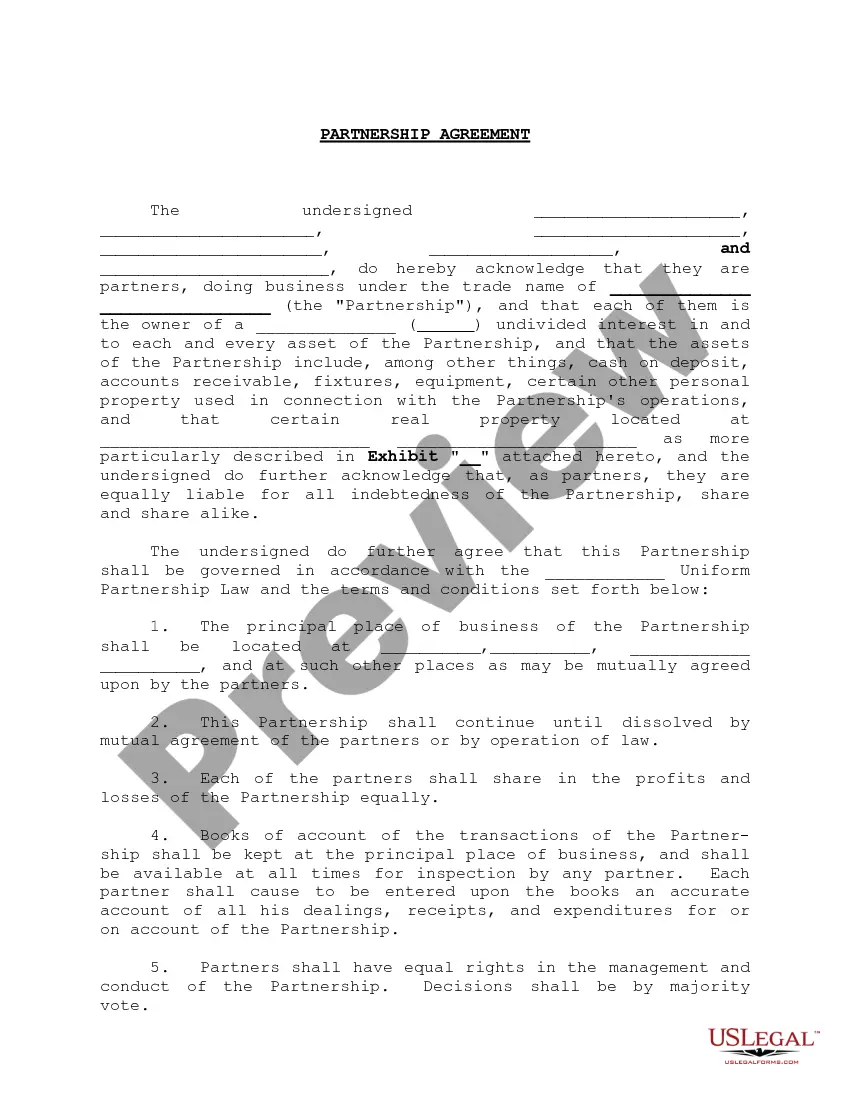

- Identification of partners and the trade name of the partnership.

- Details of ownership percentages and the investment contributions of each partner.

- Management rights and decision-making processes among partners.

- Profit and loss sharing arrangements.

- Conditions for the continuation and dissolution of the partnership.

- Buy-sell agreement stipulations for transferring partnership interests.

When to use this document

This Partnership Agreement is ideal for LLC members who are entering into a partnership. Use this form when you want to formalize the terms of the partnership, define each partner's role, or clarify contributions and ownership percentages. It is also necessary when partners wish to establish protocols for buying or selling their interests in the partnership upon exit events such as retirement or death.

Who needs this form

This form is suitable for:

- Individuals forming a partnership under an LLC structure.

- Business partners who require a clear and formal written agreement to govern their partnership.

- Entrepreneurs seeking protection and clarity in their business relationships.

- Existing LLC members who want to update or formalize their partnership terms.

Completing this form step by step

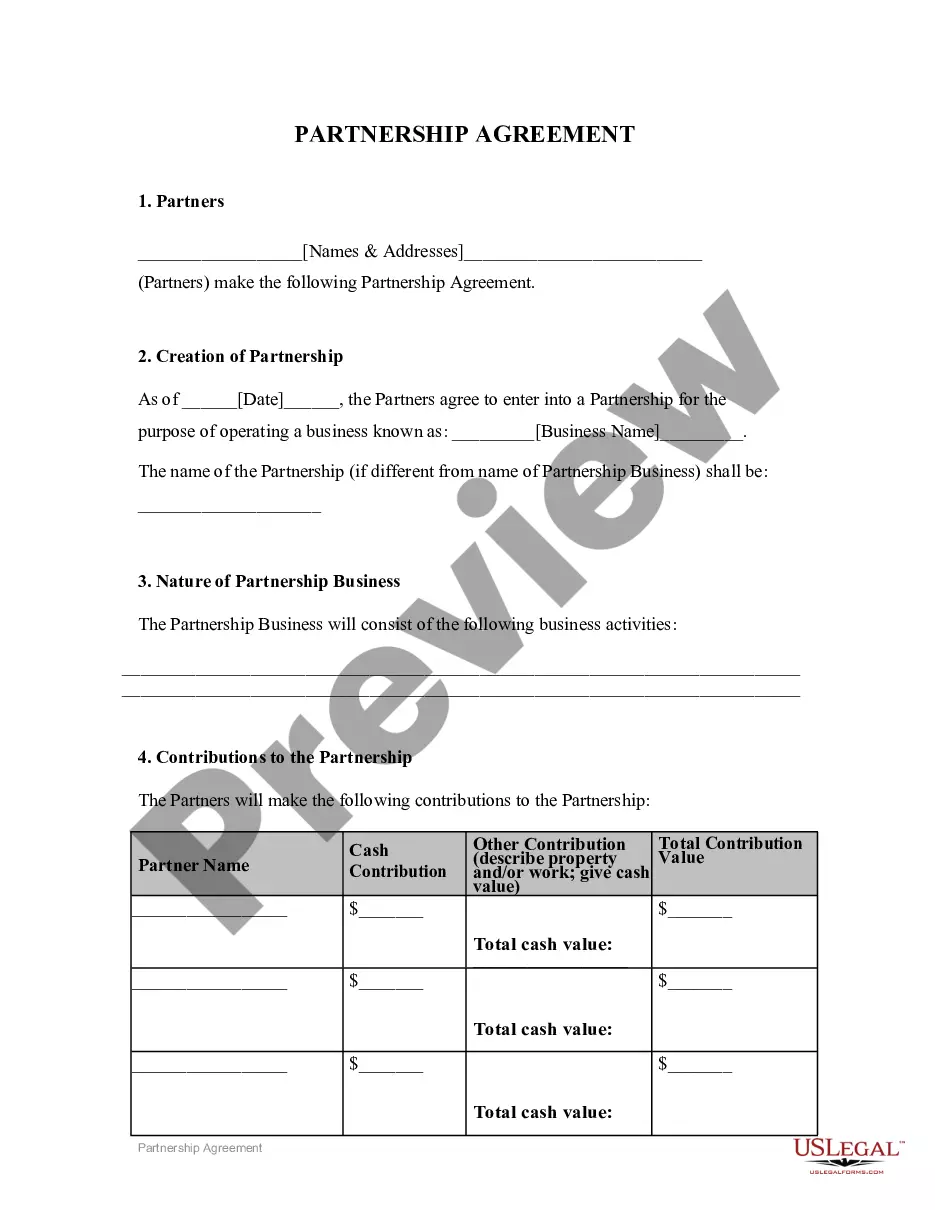

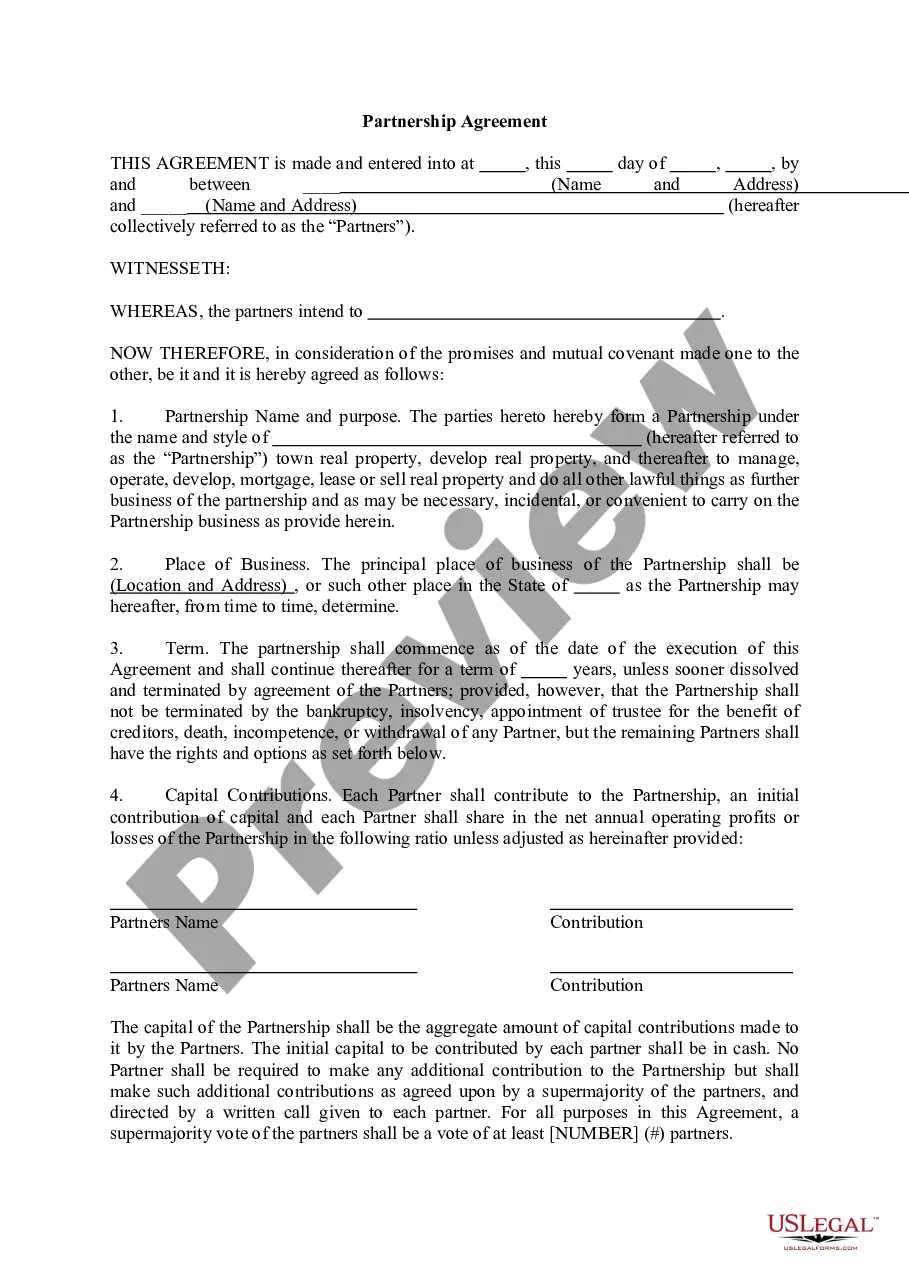

- Identify and list all partners involved in the LLC and their respective contributions.

- Specify the agreed ownership percentage for each partner based on their investment.

- Outline the principal place of business for the partnership.

- Define the terms for profit and loss sharing among partners.

- Include a buy-sell agreement to dictate how interests are transferred in specific circumstances.

Notarization guidance

This form does not typically require notarization unless specified by local law. Ensure to check your state regulations for any specific requirements regarding notarization of partnership agreements.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to clearly specify each partner's ownership percentage and contributions.

- Neglecting to outline management decision-making processes.

- Overlooking the inclusion of a buy-sell agreement for partnership interest transfers.

- Not reviewing the agreement to ensure compliance with state-specific laws.

Benefits of completing this form online

- Convenience of immediate access to downloadable forms available 24/7.

- Editability allows customization to meet specific partnership needs.

- Reliability of forms drafted by licensed attorneys to ensure legal compliance.

Looking for another form?

Form popularity

FAQ

Name of your partnership. Contributions to the partnership and percentage of ownership. Division of profits, losses and draws. Partners' authority. Withdrawal or death of a partner.

A Limited Liability Company (LLC) is an entity created by state statute.A domestic LLC with at least two members is classified as a partnership for federal income tax purposes unless it files Form 8832 and elects to be treated as a corporation.

Pursuant to the entity classification rules, a domestic entity that has more than one member will default to a partnership. Thus, an LLC with multiple owners can either accept its default classification as a partnership, or file Form 8832 to elect to be classified as an association taxable as a corporation.

Partners in an LLC can take their earnings as draws, much like a single-member LLC.Meaning, while it reports its income to the IRS with IRS Form 1065, the partnership isn't taxed. Instead, each member pays a portion of the total income tax on the partnership's earnings.

Most states do not require LLCs to have this document, so many LLCs choose not to draft one. While it may not be a requirement to have an operating agreement, it's actually in the best interest of an LLC to draft one.

A multi-member LLC is a limited liability company with two or more members. Like a single-member LLC, a multi-member LLC (MMLLC) is a lightweight business entity that combines the flexibility of a partnership with the limited liability of a corporation.

They both offer "pass-through" taxation, which means that the owners report business income or losses on their individual tax returns; the partnership or LLC itself does not pay taxes. And both are eligible for the 20% pass-through deduction established by the Tax Cuts and Jobs Act.

Owners are exposed to liability as a partner, so they form an LLC and conduct their partnership business as an LLC. The LLC takes the full liability but shields the owners from personal liability. An LLC can choose to be taxed as a corporation if it does not want to be taxed as a partnership.

Partners in a limited liability company (LLC), also known as members, aren't considered employees. Given this, a partner generally cannot receive a salary.