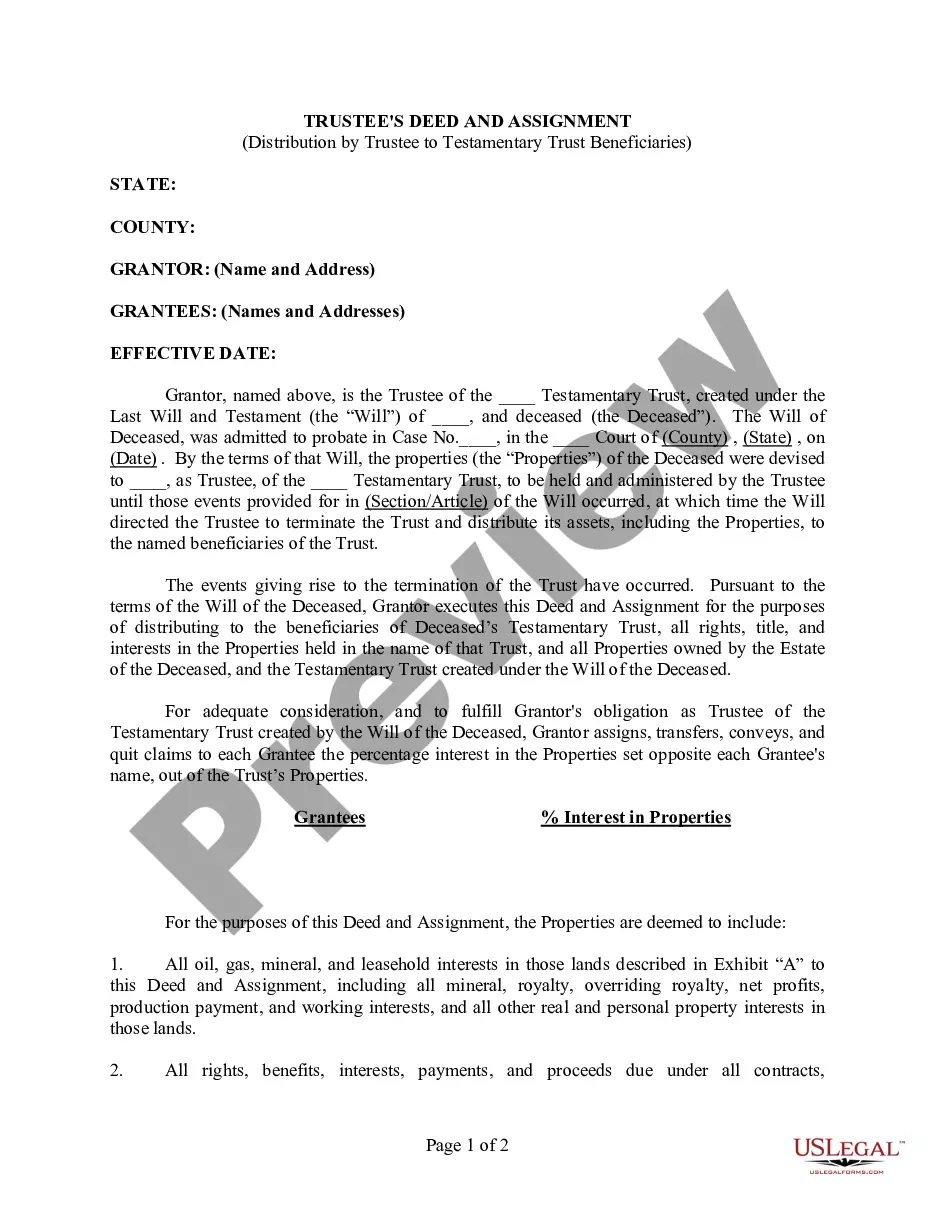

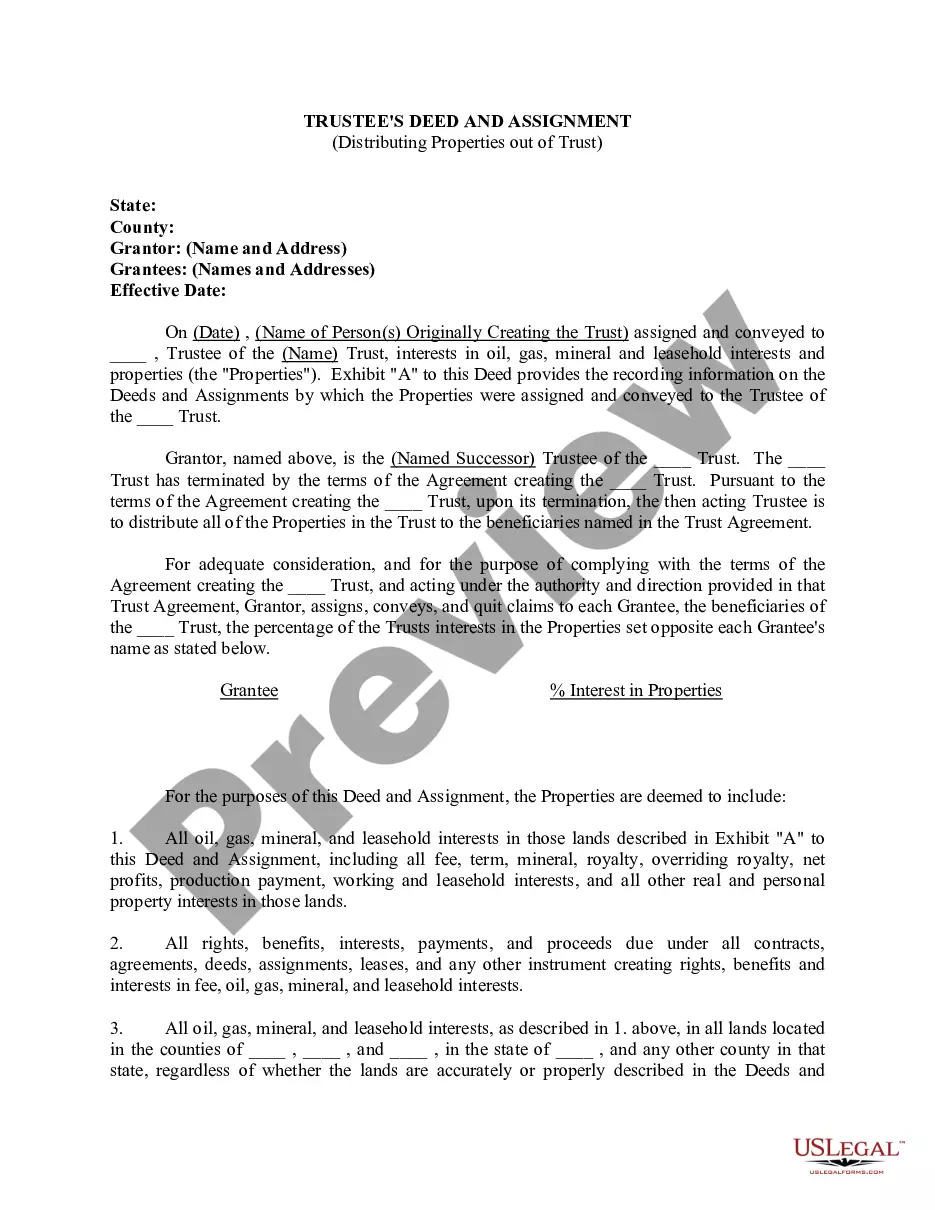

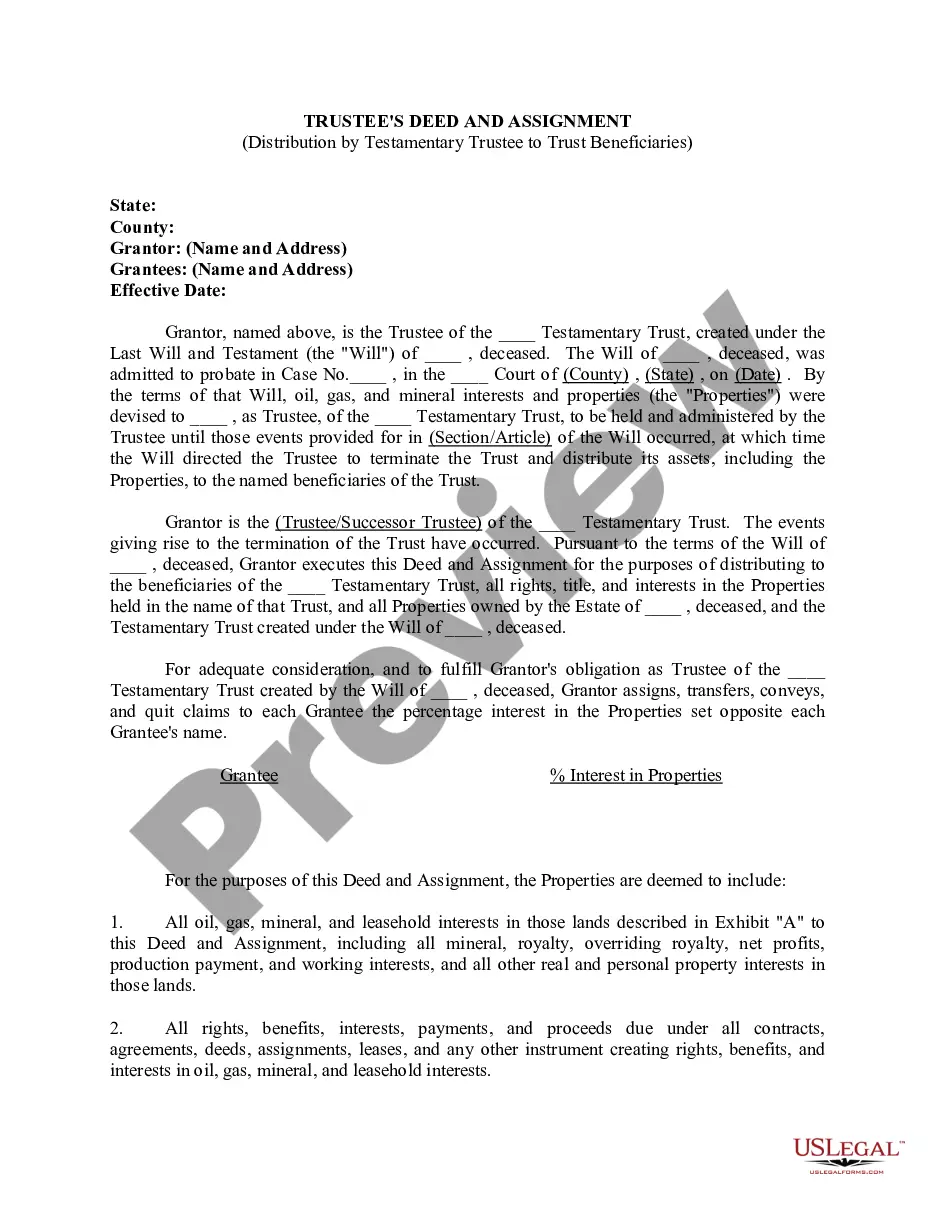

Minnesota Deed and Assignment from Trustee to Trust Beneficiaries

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Deed And Assignment From Trustee To Trust Beneficiaries?

Discovering the right legal record web template can be a battle. Naturally, there are a lot of templates available online, but how would you discover the legal type you will need? Make use of the US Legal Forms site. The services provides a large number of templates, such as the Minnesota Deed and Assignment from Trustee to Trust Beneficiaries, which you can use for organization and private demands. Every one of the forms are checked by pros and meet federal and state demands.

If you are already signed up, log in in your accounts and click on the Obtain switch to get the Minnesota Deed and Assignment from Trustee to Trust Beneficiaries. Use your accounts to look through the legal forms you have acquired previously. Check out the My Forms tab of the accounts and acquire yet another copy in the record you will need.

If you are a brand new customer of US Legal Forms, allow me to share basic directions so that you can stick to:

- First, ensure you have chosen the right type for your metropolis/state. You are able to look over the form making use of the Review switch and read the form outline to ensure it is the best for you.

- In case the type fails to meet your expectations, utilize the Seach field to discover the proper type.

- When you are certain the form would work, select the Get now switch to get the type.

- Choose the pricing strategy you want and enter in the essential details. Design your accounts and buy an order making use of your PayPal accounts or bank card.

- Choose the file formatting and acquire the legal record web template in your system.

- Complete, modify and produce and sign the received Minnesota Deed and Assignment from Trustee to Trust Beneficiaries.

US Legal Forms is the largest catalogue of legal forms in which you will find various record templates. Make use of the company to acquire skillfully-made paperwork that stick to express demands.

Form popularity

FAQ

The transferee must have been a beneficiary of the trust when the property was acquired and became an asset of the trust (i.e. the relevant time). There must be no consideration for the transfer and the transfer of property from trustee to beneficiary must not be part of a sale or other arrangement.

A trust agreement is a legal document containing, terms, conditions and provisions that allows the trustor to transfer the ownership of assets to the trustee to be held for the trustor's beneficiaries. The trustees will manage the property and assets on behalf of the beneficiary.

The trustee is the legal owner of trust property, who holds it for the benefit of the beneficiaries. Legal title to, and responsibility for, the management of the trust property resides in the trustee. Trusts Flashcards - Quizlet Quizlet ? Social Science ? Law ? Civil Law Quizlet ? Social Science ? Law ? Civil Law

So can a trustee also be a beneficiary? The short answer is yes, but the trustee will have to be exceedingly careful to never engage in any actions that would constitute a breach of trust, including placing their personal interests above those of the other beneficiaries. Can a Trustee Be a Beneficiary? - Keystone Law Group keystone-law.com ? can-trustee-be-beneficiary keystone-law.com ? can-trustee-be-beneficiary

If you borrow from a commercial lender, it is most likely that the lender will determine the trustee, which is typically a title company, professional escrow company, or other company in the business of serving as a real estate trustee. Sometimes a real estate broker or an attorney serves in this role.

Equitable titles in trust property are held by the beneficiaries of the trust assets. Legal vs. Equitable Title | Definition, Rights & Applications Study.com ? academy ? lesson ? legal-equitable... Study.com ? academy ? lesson ? legal-equitable...

When property is ?held in trust,? there is a divided ownership of the property, ?generally with the trustee holding legal title and the beneficiary holding equitable title.? The trust itself owns nothing because it is not an entity capable of owning property.

The legal title of a property refers to the legal ownership which comes with the right to control the property in compliance with the law. An equitable title gives a person the right to enjoy the benefits that come with the ownership of a property despite them not being the legal titleholders. Legal vs. Equitable Title | Definition, Rights & Applications - Study.com study.com ? learn ? lesson ? legal-vs-equitable-titl... study.com ? learn ? lesson ? legal-vs-equitable-titl...