Minnesota Statement of Current Monthly Income and Disposable Income Calculation for Use in Chapter 13 - Post 2005

Description

How to fill out Statement Of Current Monthly Income And Disposable Income Calculation For Use In Chapter 13 - Post 2005?

You may spend hrs on the Internet attempting to find the lawful papers template that fits the federal and state specifications you require. US Legal Forms offers thousands of lawful types which are examined by specialists. It is possible to acquire or printing the Minnesota Statement of Current Monthly Income and Disposable Income Calculation for Use in Chapter 13 - Post 2005 from my service.

If you have a US Legal Forms bank account, you may log in and click on the Acquire key. Next, you may full, edit, printing, or indication the Minnesota Statement of Current Monthly Income and Disposable Income Calculation for Use in Chapter 13 - Post 2005. Every lawful papers template you purchase is the one you have permanently. To get an additional duplicate of the bought type, visit the My Forms tab and click on the corresponding key.

If you use the US Legal Forms web site initially, keep to the simple recommendations listed below:

- Initial, be sure that you have chosen the right papers template to the area/area of your liking. Browse the type information to ensure you have selected the correct type. If available, utilize the Preview key to look from the papers template also.

- If you want to get an additional edition from the type, utilize the Research industry to get the template that meets your requirements and specifications.

- After you have discovered the template you need, click Acquire now to continue.

- Pick the pricing prepare you need, enter your references, and register for an account on US Legal Forms.

- Complete the transaction. You may use your bank card or PayPal bank account to pay for the lawful type.

- Pick the formatting from the papers and acquire it to the system.

- Make modifications to the papers if possible. You may full, edit and indication and printing Minnesota Statement of Current Monthly Income and Disposable Income Calculation for Use in Chapter 13 - Post 2005.

Acquire and printing thousands of papers web templates making use of the US Legal Forms website, that provides the greatest selection of lawful types. Use expert and condition-certain web templates to take on your small business or person requirements.

Form popularity

FAQ

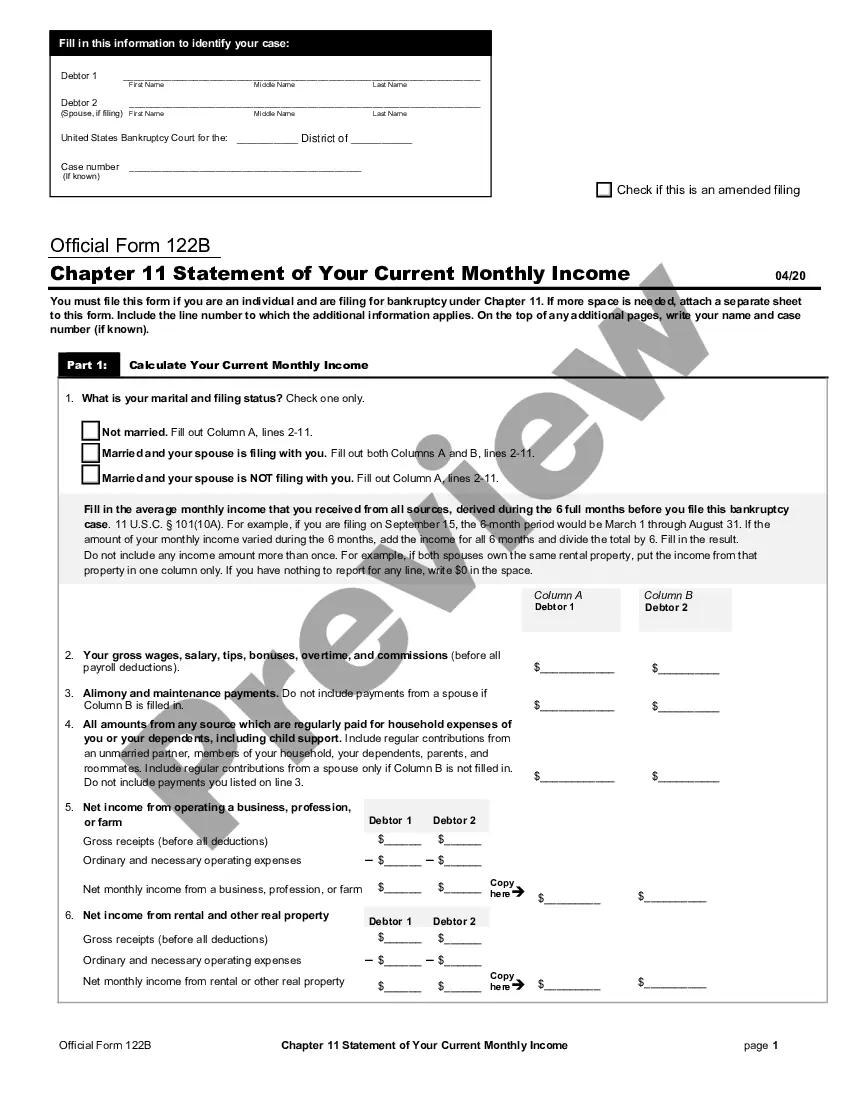

What is Disposable Personal Income? After-tax income. The amount that U.S. residents have left to spend or save after paying taxes is important not just to individuals but to the whole economy. The formula is simple: personal income minus personal current taxes.

You can't pay more than your disposable income in Chapter 13, because your disposable income represents all earnings that remain after paying required debts. However, there is another step in the Chapter 13 payment calculation, and if you don't meet the criteria, the judge won't approve your plan.

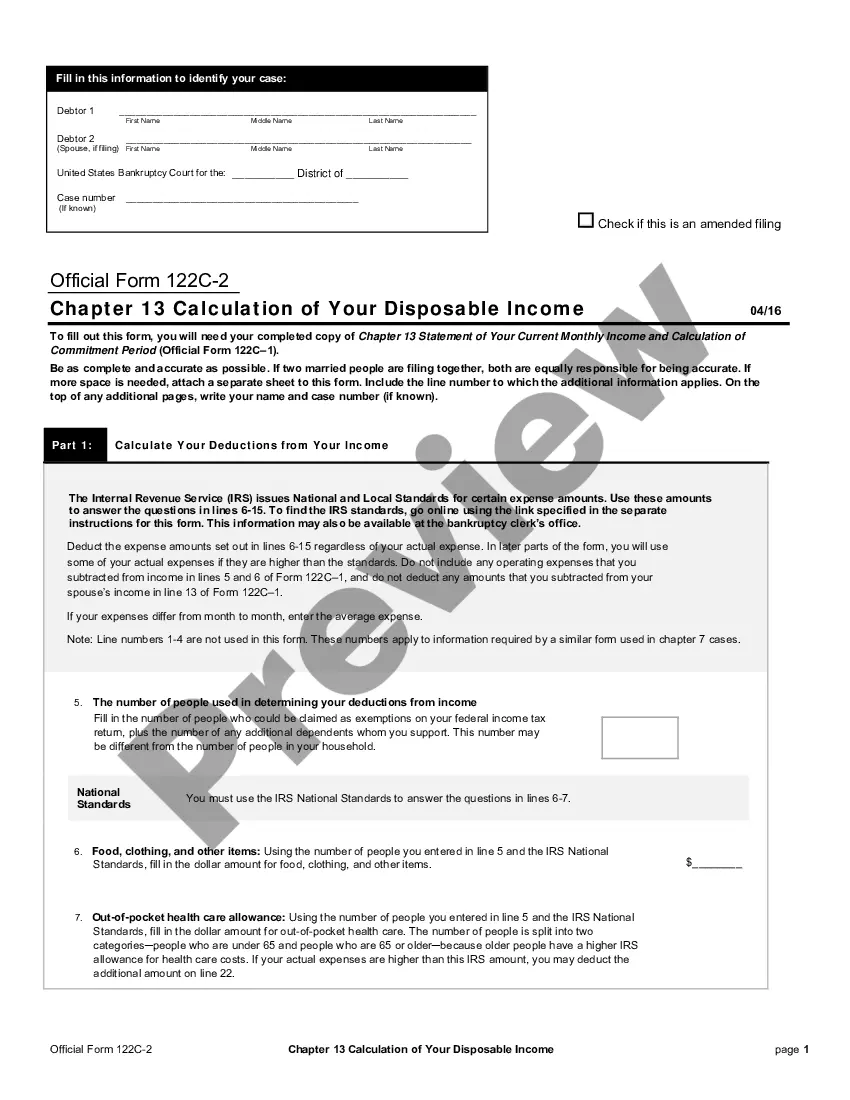

To calculate your monthly payment amount in a Chapter 13 bankruptcy, calculate your income for the six months before your bankruptcy filing. Deduct allowable expenses to determine your disposable income. Pay your priority debtors and any secured debts that you want to keep after the bankruptcy.

All debts other than priority and secured obligations are general unsecured debt?and the amount you'll pay to your unsecured creditors in Chapter 13 bankruptcy will be the greater of your disposable income or the amount your creditors would have received had you filed for Chapter 7 bankruptcy. Disposable income.

How Is Disposable Income Calculated? Your last six months of income divided by six to get average monthly income. If you own a business or work for yourself, you must calculate average monthly income. Any money you get from rent on an asset you own, interests, dividends or royalties.

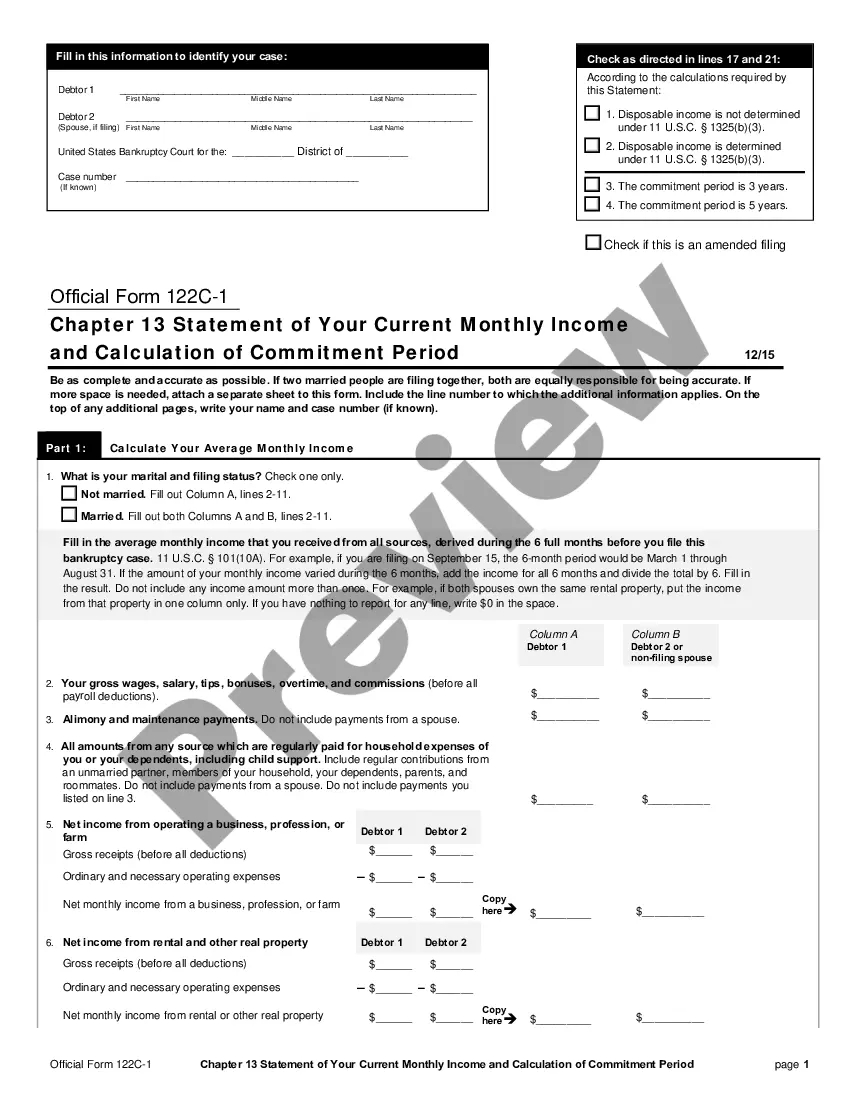

For a Chapter 13, the ?Chapter 13 Statement of Your Current Monthly Income and Calculation of Commitment Period? (Form 122C-1) tells the court your average monthly income. Your income is compared to the median income for your state, which will assist in calculating your disposable income.

A debtor must have enough income, after deducting allowable expenses, for all debt obligations. A debtor may include income from a working spouse even if the spouse has not filed jointly for bankruptcy, wages and salary, self-employment income, Social Security benefits, and unemployment benefits.

To calculate the total average monthly payment, add all amounts that are contractually due to each secured creditor in the 60 months after you file for bankruptcy. Then divide by 60.