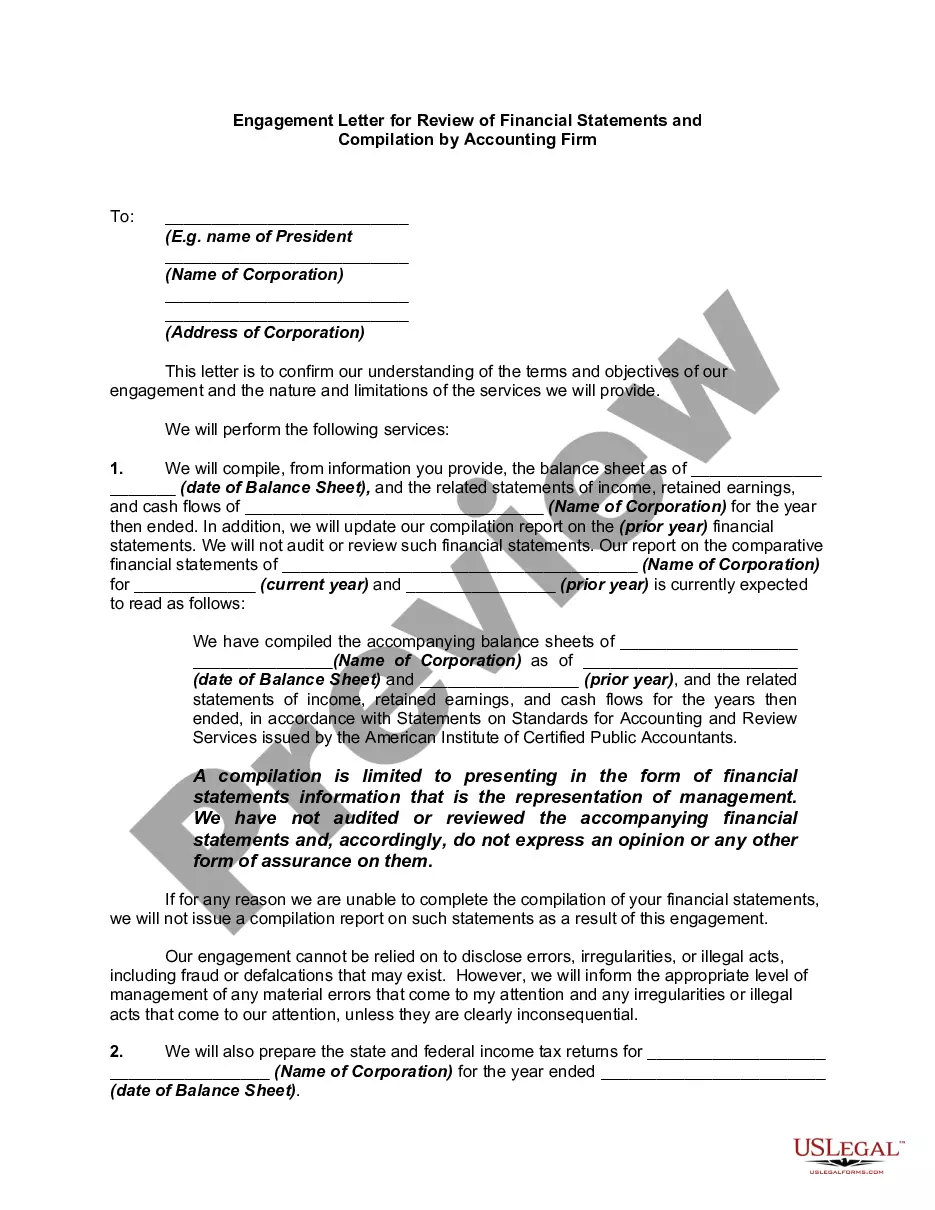

In a compilation engagement, the accountant presents in the form of financial statements information that is the representation of management (owners) without undertaking to express any assurance on the statements. In other words, using management's records, the accountant creates financial statements without gathering evidence or opining about the validity of those underlying records. Because compiled financial statements provide the reader no assurance regarding the statements, they represent the lowest level of financial statement service accountants can provide to their clients. Accordingly, standards governing compilation engagements require that financial statements presented by the accountant to the client or third parties must at least be compiled.

Minnesota Report from Review of Financial Statements and Compilation by Accounting Firm

Description

How to fill out Report From Review Of Financial Statements And Compilation By Accounting Firm?

In case you need to thorough, download, or create legal document formats, utilize US Legal Forms, the largest collection of legal templates, available online.

Leverage the site’s user-friendly and convenient search function to find the documents you require.

Various formats for both commercial and personal use are organized by categories and jurisdictions, or keywords.

Step 4. Once you have found the form you need, click on the Get now button. Choose the pricing plan you prefer and enter your details to register for an account.

Step 5. Complete the transaction. You can use your credit card or PayPal account to finalize the purchase.

- Access US Legal Forms to fetch the Minnesota Report from Review of Financial Statements and Compilation by Accounting Firm within a few clicks.

- If you are already a US Legal Forms customer, sign in to your account and click on the Download button to locate the Minnesota Report from Review of Financial Statements and Compilation by Accounting Firm.

- You can also reach forms you have previously acquired from the My documents section of your account.

- If this is your first time using US Legal Forms, follow the steps outlined below.

- Step 1. Confirm you have selected the form for the correct city/state.

- Step 2. Use the Review option to examine the form’s details. Remember to read the summary.

- Step 3. If you are unsatisfied with the template, use the Search field at the top of the screen to find other versions of the legal form template.

Form popularity

FAQ

No, a compilation is not the same as a review. While a compilation simply presents financial data provided by the client without offering assurance, a review involves a more thorough examination that provides limited assurance to stakeholders. Recognizing this distinction is essential for understanding the services offered in the Minnesota Report from Review of Financial Statements and Compilation by Accounting Firm.

Yes, a CPA can perform a compilation without undergoing a peer review, as it does not require an extensive evaluation process. However, it's crucial to ensure that the CPA operates within the applicable ethical standards to maintain credibility. For services like the Minnesota Report from Review of Financial Statements and Compilation by Accounting Firm, transparency in the compilation process is vital to ensure stakeholders remain informed.

A financial compilation report is a document prepared by a CPA based on information provided by the client. It assembles the financial statements without any assurance regarding their accuracy or completeness. This type of report is commonly used in the Minnesota Report from Review of Financial Statements and Compilation by Accounting Firm to streamline financial reporting for small businesses.

A review by a CPA includes the evaluation of financial statements through analytical procedures and inquiries. It aims to provide limited assurance that no material modifications are needed for the statements to be in accordance with the applicable financial reporting framework. For a Minnesota Report from Review of Financial Statements and Compilation by Accounting Firm, this process fosters trust and credibility in financial reporting.

The Minnesota Report from Review of Financial Statements and Compilation by Accounting Firm essentially highlights the differing levels of assurance provided by each service. A CPA review offers limited assurance, meaning the accountant performs analytical procedures to identify any potential issues. In contrast, a compilation involves merely presenting financial information provided by the client without providing any assurance.

Yes, a CPA can both prepare and review financial statements, provided they maintain the required independence during the review phase. This dual capability allows them to offer comprehensive services while ensuring transparency and trust. Utilizing a CPA for these tasks can enhance the integrity of your Minnesota Report from Review of Financial Statements and Compilation by Accounting Firm.

A CPA must understand the entity's internal controls, operations, and industry as part of planning a financial statement audit. This understanding helps tailor the audit procedures effectively. Ultimately, this thorough preparation is essential for producing a reliable Minnesota Report from Review of Financial Statements and Compilation by Accounting Firm.

While a non-CPA can perform certain types of reviews, they may not be able to provide the same level of assurance as a licensed CPA. The absence of a CPA may limit the acceptance of the review in formal settings. Using a CPA ensures adherence to standards and can enhance the value of the Minnesota Report from Review of Financial Statements and Compilation by Accounting Firm.

Yes, a CPA must maintain independence when conducting a review of financial statements. Independence allows the CPA to provide an unbiased opinion on the statements. This integrity is crucial for the credibility of the Minnesota Report from Review of Financial Statements and Compilation by Accounting Firm.

Reviewed financial statements can be prepared by Certified Public Accountants (CPAs) who possess the necessary knowledge and expertise in financial reporting. These professionals conduct an objective assessment to provide reasonable assurance on the statements. If you need assistance, consider using USLegalForms to streamline this process.