Under the Equal Credit Opportunity Act, a creditor may design its own application forms, use forms prepared by another person, or use the appropriate model application forms contained in 12 C.F.R. Part 202, Appendix B. If a creditor chooses to use an Appendix B form, it may change the form by: (1) asking for additional information not prohibited by 12 C.F.R. § 202.5; (2) by deleting any information request; or (3) by rearranging the format without modifying the substance of the inquiries; provided that in each of these three instances the appropriate notices regarding the optional nature of courtesy titles, the option to disclose alimony, child support, or separate maintenance, and the limitation concerning marital status inquiries are included in the appropriate places if the items to which they relate appear on the creditor's form.

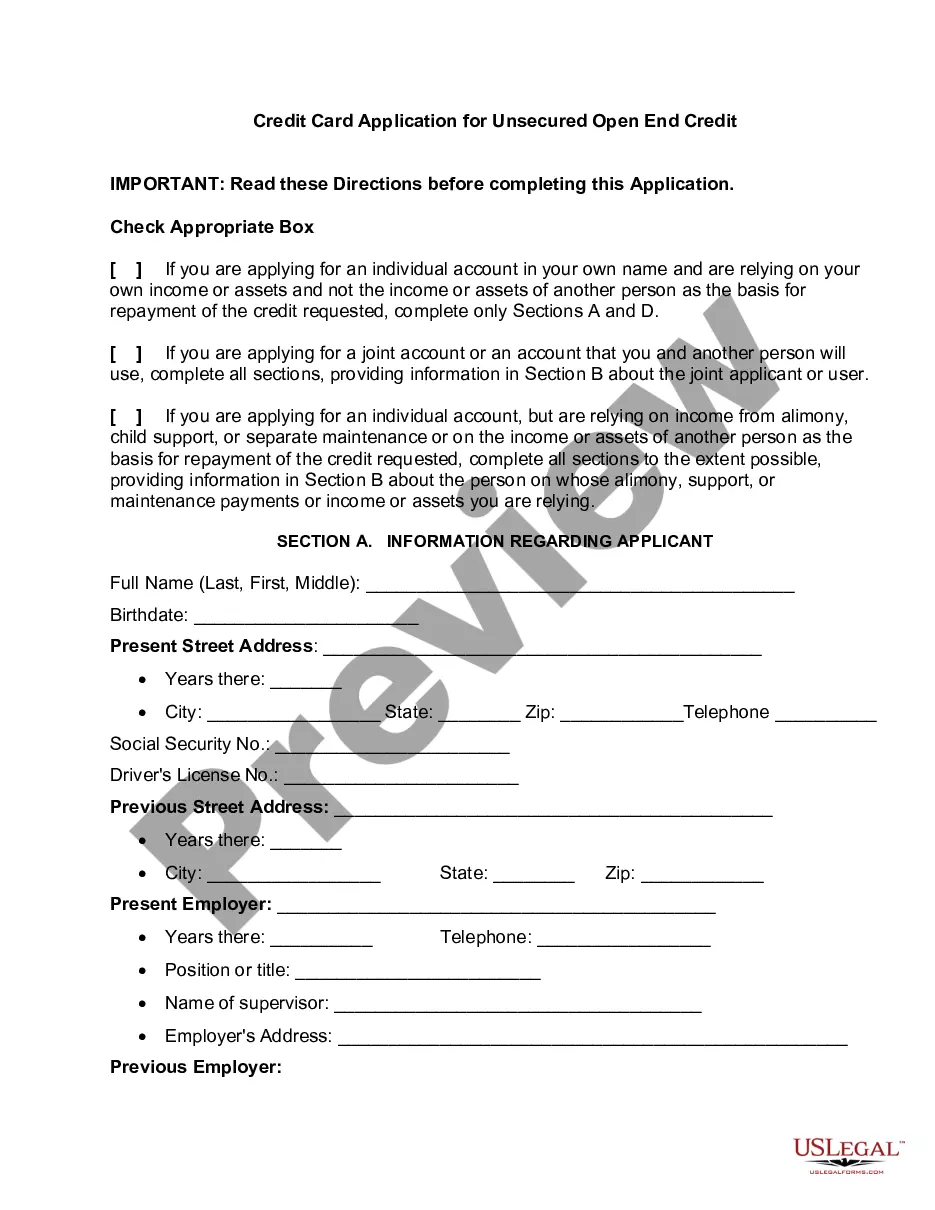

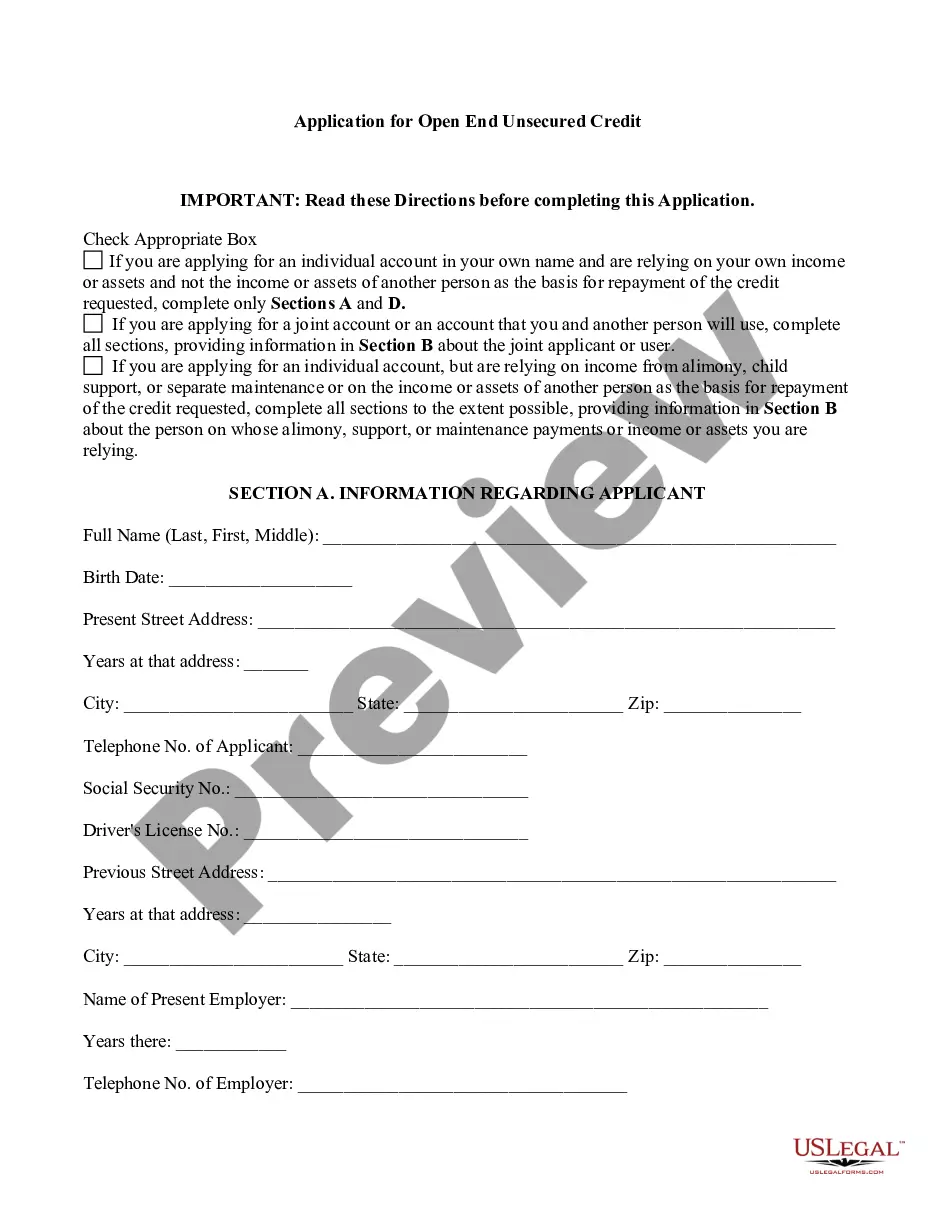

Minnesota Application for Open End Unsecured Credit - Signature Loan

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Application For Open End Unsecured Credit - Signature Loan?

You can allocate time online searching for the sanctioned document template that aligns with the state and federal requirements you require.

US Legal Forms provides a vast array of legal documents that can be assessed by professionals.

You can effortlessly download or print the Minnesota Application for Open End Unsecured Credit - Signature Loan from my services.

If available, utilize the Preview button to review the document template as well. If you wish to find another variation of the form, use the Search field to locate the template that suits your needs and criteria. Once you have identified the template you desire, click Buy now to continue. Select the pricing plan you require, enter your credentials, and register for an account on US Legal Forms. Complete the transaction. You can use your credit card or PayPal account to pay for the legal form. Choose the format of the document and download it to your device. Make adjustments to the document if necessary. You can fill out, alter, and sign and print the Minnesota Application for Open End Unsecured Credit - Signature Loan. Download and print a multitude of document templates using the US Legal Forms website, which offers the most comprehensive selection of legal forms. Utilize professional and state-specific templates to address your business or personal needs.

- If you already possess a US Legal Forms account, you can Log In and click on the Download button.

- Then, you can fill out, amend, print, or sign the Minnesota Application for Open End Unsecured Credit - Signature Loan.

- Each legal document template you obtain is yours permanently.

- To acquire another copy of the purchased form, visit the My documents section and click on the relevant button.

- If you are using the US Legal Forms website for the first time, follow the simple guidelines outlined below.

- First, ensure you have selected the correct document template for the region/area of your choice.

- Review the form details to confirm you have chosen the appropriate form.

Form popularity

FAQ

Of course as with any form of credit, irresponsible use of a personal loan can have a negative impact on your credit score. And much like with any other loan, mortgage, or credit card application, applying for a personal loan can cause a slight dip in your credit score.

To determine whether to grant a signature loan, a lender typically looks for a solid credit history and sufficient income to repay the loan. In some cases, the lender may require a co-signer on the loan, but the co-signer is only called upon in the event the original lender defaults on payments.

Some of the easiest loans to get approved for include payday loans, no-credit-check loans, and pawnshop loans. Personal loans with essentially no approval requirements typically charge the highest interest rates and loan fees.

But signature loans are not the same as installment loans. Usually installment loans offer larger loan amounts than signature loans, which usually offer smaller loan amounts. Signature loans usually come with a shorter loan term and a shorter payment plan.

Open-end credit is a loan from a bank or other financial institution that the borrower can draw on repeatedly, up to a certain pre-approved amount, and that has no fixed end date for full repayment. Open-end credit is also referred to as revolving credit.

A signature loan, which does not require collateral, is simply an unsecured personal loan.

Personal Loan Speed Based On Lender Type Financial institutionApproval timeFunding timeOnline lender1 ? 3 business days1 ? 5 business daysTraditional bank1 ? 7 business days1 ? 7 business daysCredit union1 ? 7 business days1 ? 7 business days

You'll likely be asked to submit personal and financial information, such as your name, employer, social security number (SSN), income and bank statements. Sign the loan agreement and receive funds. If your application is approved, a lender will send you a loan agreement to sign.