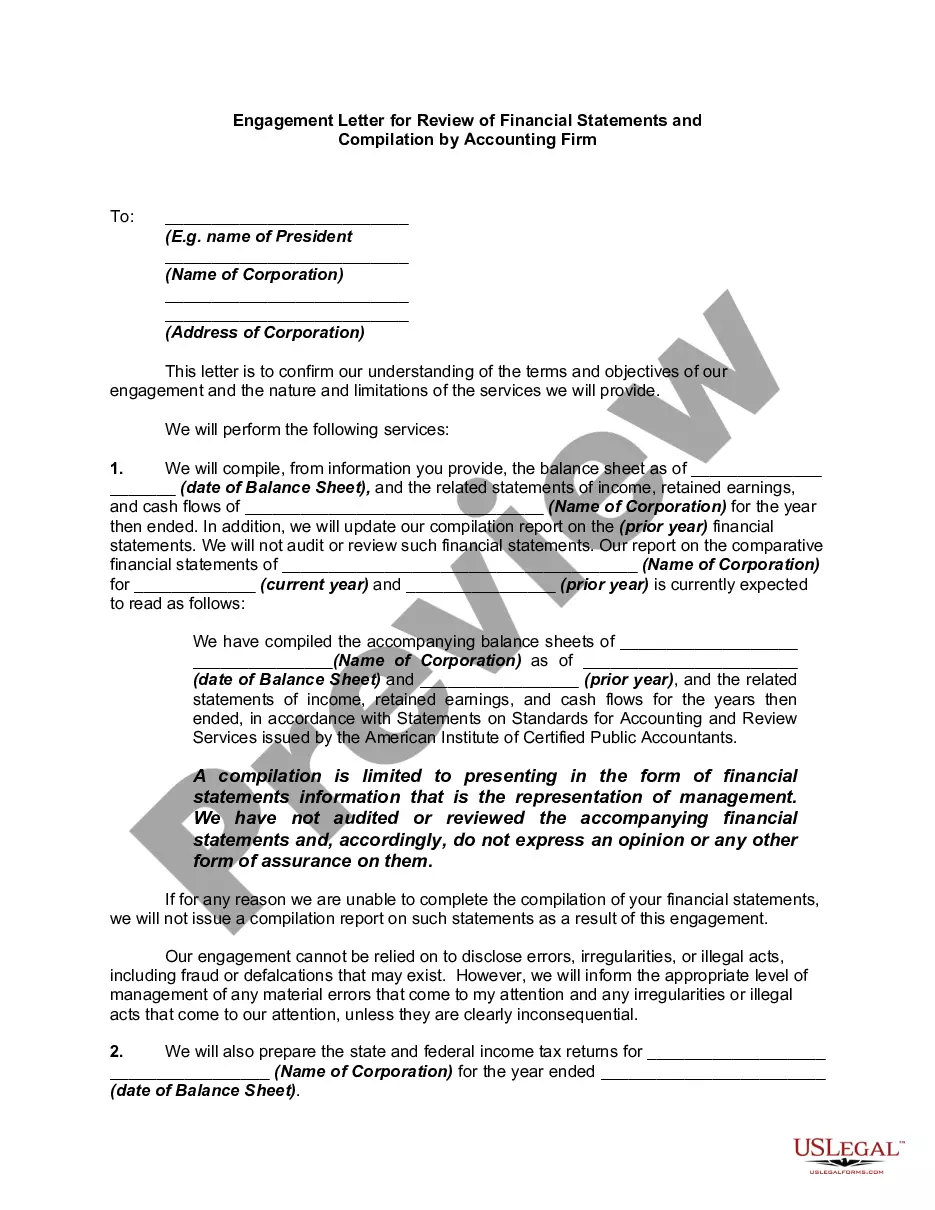

In a compilation engagement, the accountant presents in the form of financial statements information that is the representation of management (owners) without undertaking to express any assurance on the statements. In other words, using management's records, the accountant creates financial statements without gathering evidence or opining about the validity of those underlying records. Because compiled financial statements provide the reader no assurance regarding the statements, they represent the lowest level of financial statement service accountants can provide to their clients. Accordingly, standards governing compilation engagements require that financial statements presented by the accountant to the client or third parties must at least be compiled.

Michigan Report from Review of Financial Statements and Compilation by Accounting Firm

Description

How to fill out Report From Review Of Financial Statements And Compilation By Accounting Firm?

US Legal Forms - one of the most prominent collections of legal documents in the United States - offers a comprehensive selection of legal form templates available for purchase or printing.

While browsing the website, you will find thousands of forms for business and personal purposes, organized by categories, claims, or keywords.

You can quickly locate the latest versions of forms such as the Michigan Report from Review of Financial Statements and Compilation by Accounting Firm.

Click the Preview button to examine the content of the form.

Review the form overview to confirm you have selected the correct one.

- If you have a subscription, Log In to download the Michigan Report from Review of Financial Statements and Compilation by Accounting Firm from the US Legal Forms library.

- The Download button will appear on every form you view.

- You can access all previously saved forms in the My documents section of your account.

- To use US Legal Forms for the first time, here are straightforward instructions to help you begin.

- Ensure you have selected the correct form for your city/state.

Form popularity

FAQ

To evaluate audited financial statements, examine the auditor's report, management discussion, and financial disclosures. Consider the established accounting principles and the auditor's opinion on the financial statements' fairness. A detailed Michigan Report from Review of Financial Statements and Compilation by Accounting Firm offers insights that facilitate a deeper understanding of the audit results.

A CPA must understand the entity's business environment, including its risks, operations, and financial reporting requirements. This comprehensive understanding helps tailor the audit process to meet specific needs. Utilizing a professional CPA for your Michigan Report from Review of Financial Statements and Compilation by Accounting Firm can align your financial strategy with regulatory expectations.

No, a non-CPA should not perform a financial review as it does not meet the professional standards set by regulatory bodies. A review requires expertise in accounting and finance that only a licensed CPA possesses. Relying on a CPA for your Michigan Report from Review of Financial Statements and Compilation by Accounting Firm provides peace of mind and assurance.

An auditor conducts a comprehensive examination of financial statements by verifying the correctness of records and testing internal controls. They gather sufficient evidence to form an opinion on the truthfulness of the statements. Having a solid Michigan Report from Review of Financial Statements and Compilation by Accounting Firm can make this audit process smoother and more effective.

The CPA is required to obtain an understanding of the entity's internal controls and assess the overall environment in which the financial statements are prepared. They must perform inquiries and analytical procedures to evaluate financial information. This is essential in the context of a Michigan Report from Review of Financial Statements and Compilation by Accounting Firm to ensure accuracy and completeness.

Yes, independence is a crucial factor for a CPA performing a review of financial statements. This independence ensures that the CPA's judgment remains unbiased and transparent throughout the process. When you seek a Michigan Report from Review of Financial Statements and Compilation by Accounting Firm, choosing an independent CPA can enhance trust in the results.

A CPA specializes in conducting thorough reviews of financial statements for various entities, enhancing the credibility of financial reports. They compare records against industry standards and ensure all reporting guidelines are met. Engaging with a CPA for your Michigan Report from Review of Financial Statements and Compilation by Accounting Firm is an essential step toward maintaining financial integrity.

A CPA review of financial statements provides a higher level of assurance than an assembly but lower than an audit. The process involves the CPA analyzing the entity’s financial data, assessing compliance with accounting standards, and providing a report. This Michigan Report from Review of Financial Statements and Compilation by Accounting Firm ensures that stakeholders receive reliable financial information.

No, a compilation is not the same as a review. A compilation report presents financial information without performing detailed analysis or verification, while a review involves a more systematic examination of the data and provides limited assurance. For businesses that want their financial statements to be clearly understood, the Michigan Report from Review of Financial Statements and Compilation by Accounting Firm can be an ideal choice.

Financial review and compilation serve distinct purposes in financial reporting. A financial review includes analytical procedures and offers a moderate level of assurance, while a compilation primarily organizes data without assessing its accuracy. Companies seeking comprehensive insights often opt for the Michigan Report from Review of Financial Statements and Compilation by Accounting Firm for a balanced perspective.