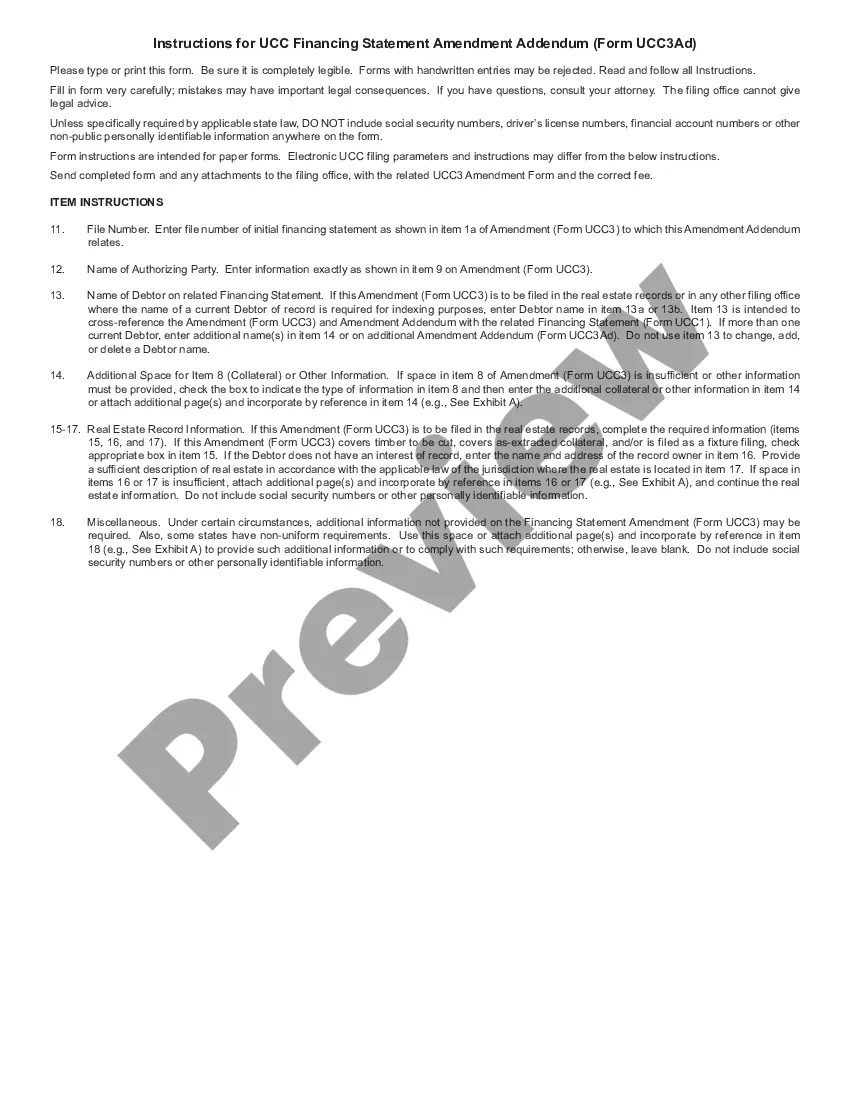

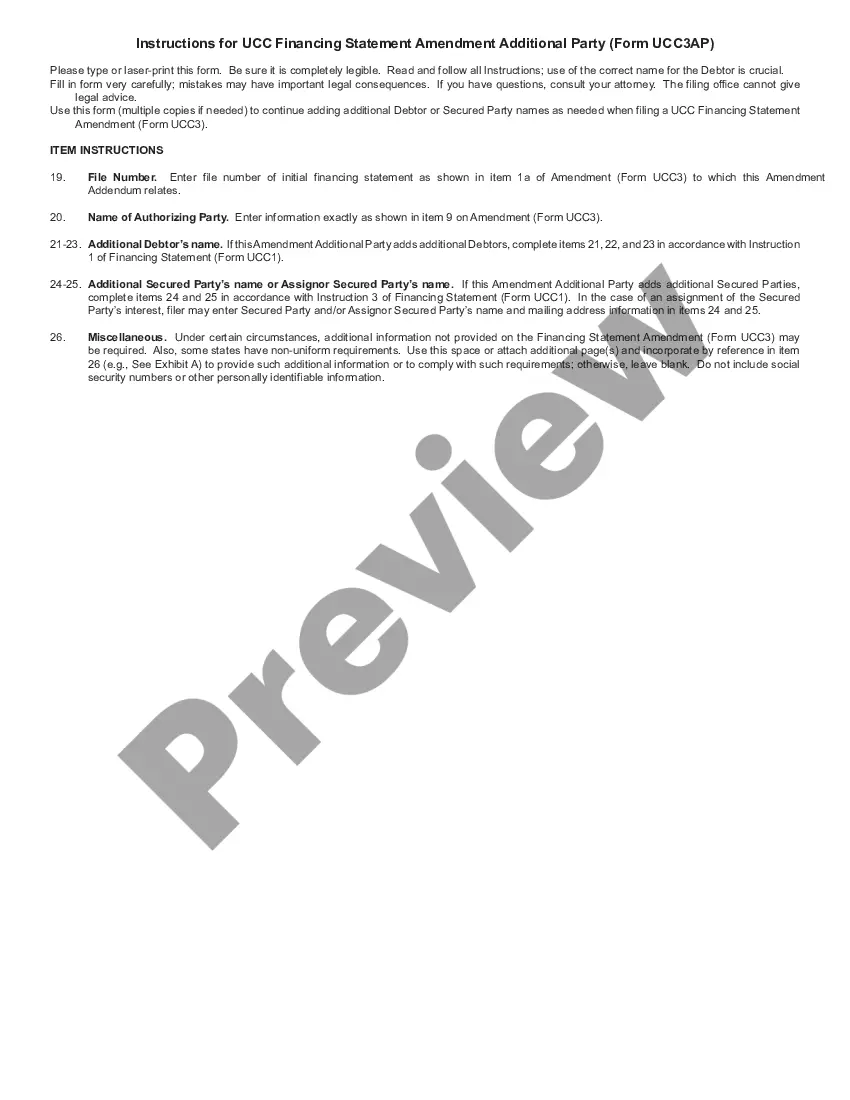

Financing Statement Amendment Additional Party form for adding additional Debtors or Secured Parties to Financing Statement Amendment (Form UCC3) filed with the Maine filing office.

Maine UCC3 Financing Statement Amendment Additional Party

State:

Maine

Control #:

ME-UCC3-AP

Format:

PDF

Instant download

This website is not affiliated with any governmental entity

Public form

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Maine UCC3 Financing Statement Amendment Additional Party?

Obtain any template from 85,000 legal documents, including the Maine UCC3 Financing Statement Amendment Additional Party, online through US Legal Forms.

Each template is crafted and refreshed by state-approved attorneys.

If you are already a subscriber, Log In. Once you are on the form’s page, press the Download button and navigate to My documents to access it.

With US Legal Forms, you'll always have immediate access to the suitable downloadable sample. The platform provides access to documents and organizes them into categories to streamline your search. Utilize US Legal Forms to acquire your Maine UCC3 Financing Statement Amendment Additional Party with ease and speed.

- Confirm the state-specific prerequisites for the Maine UCC3 Financing Statement Amendment Additional Party you wish to utilize.

- Examine the description and inspect the sample.

- As soon as you are certain the template meets your needs, simply click Buy Now.

- Choose a subscription plan that fits your financial plan.

- Establish a personal account.

- Make your payment in one of two acceptable methods: via credit card or through PayPal.

- Select a format to download the document in; two formats are offered (PDF or Word).

- Download the file to the My documents section.

- After your reusable form is downloaded, print it or save it to your device.

Form popularity

FAQ

Yes, a UCC financing statement can be assigned through the use of a UCC-3 assignment form. This allows the initial secured party to transfer their rights to another party, thereby enabling the new party to hold the security interest. If you're navigating the complexities of a Maine UCC3 Financing Statement Amendment Additional Party, utilizing the UCC-3 assignment ensures that all legal interests are correctly represented.

To terminate a UCC financing statement, you must file a UCC-3 form, specifically noting the termination. This process involves providing the details of the original UCC statement, including the debtor's name and details of the secured party. By officially marking the financing statement as terminated, you effectively release any claims on the asset, ensuring clarity in property interests in Maine.

In the state of Maine, a UCC financing statement must be filed with the Secretary of State’s office, ensuring it is part of the public record. This location is essential for maintaining the integrity of the information regarding secured interests. Utilizing the uslegalforms platform simplifies the filing process, allowing you to easily manage and file your Maine UCC3 Financing Statement Amendment Additional Party, streamlining your experience and ensuring compliance.

Section 9-503 of the UCC provides various, more specific rules regarding the sufficiency of a debtor's name on a financing statement.However, unlike with a security agreement, on a financing statement it is acceptable to use a supergeneric description of collateral.

To continue the effectiveness of a UCC-1 financing statement beyond its initial 5-year effective period, a secured party must file a Continuation. A Continuation extends the life of the financing statement for an additional five years.Each Continuation must identify, by its file number, the UCC-1 to which it relates.

A UCC-3 termination statement (a Termination) is a required filing that terminates a security interest that has been perfected by a UCC-1 filing. 1. A Termination for personal property is accomplished by completing and filing form UCC-3 with the Secretary of State's office in the appropriate state.

The secured party has 20 days to either terminate the filing or send a termination statement to the debtor that the debtor can then file. If this does not happen within the 20-day time frame, the debtor may file a UCC-3 termination statement.

The secured party has 20 days to either terminate the filing or send a termination statement to the debtor that the debtor can then file. If this does not happen within the 20-day time frame, the debtor may file a UCC-3 termination statement.

When the debtor has satisfied all amounts owed to the lender, a UCC-3 termination statement (now called a UCC termination statement) is routinely filed to terminate the security interest perfected by the UCC-1 financing statement.