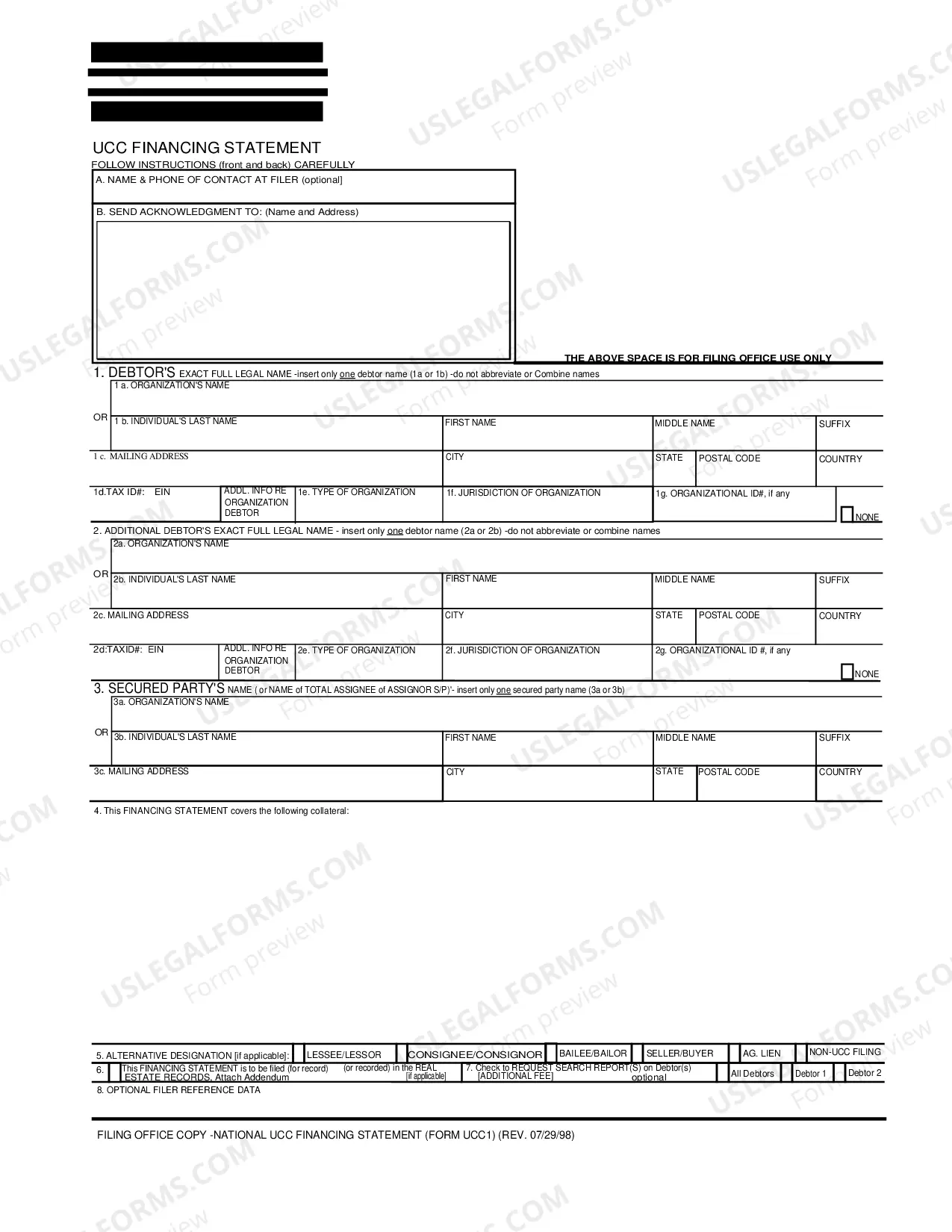

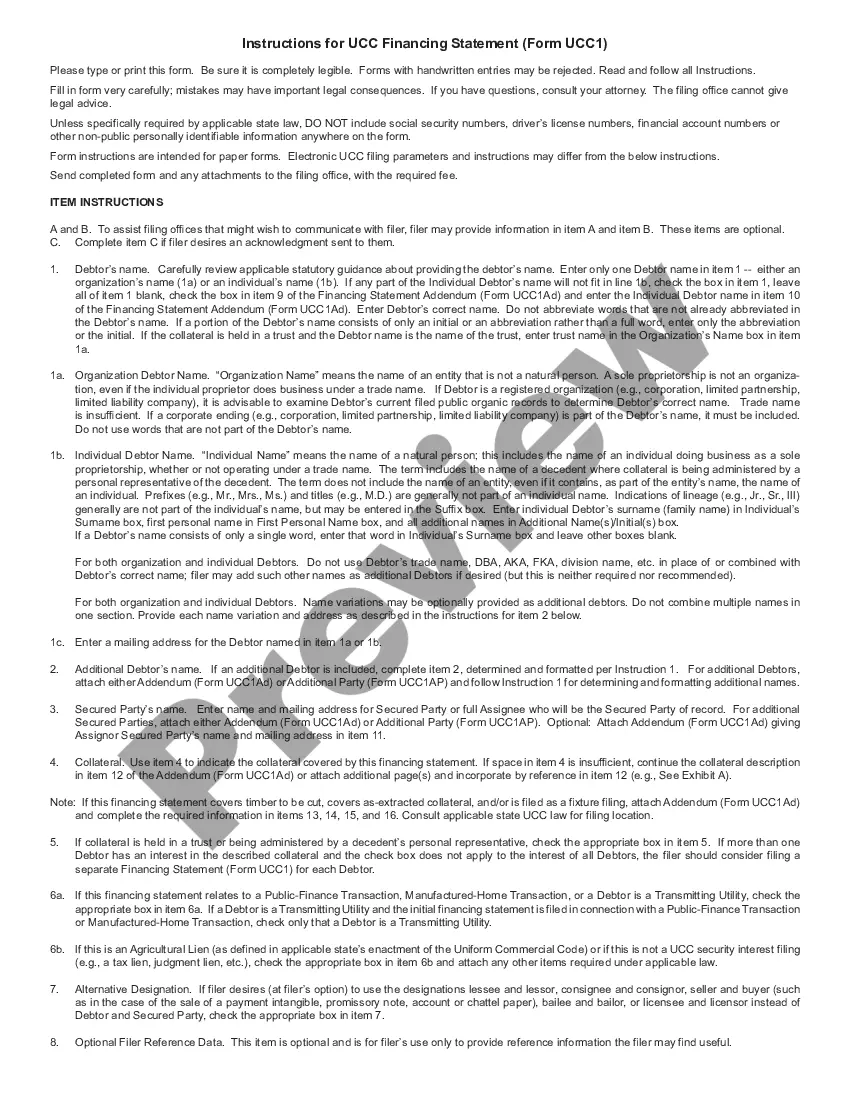

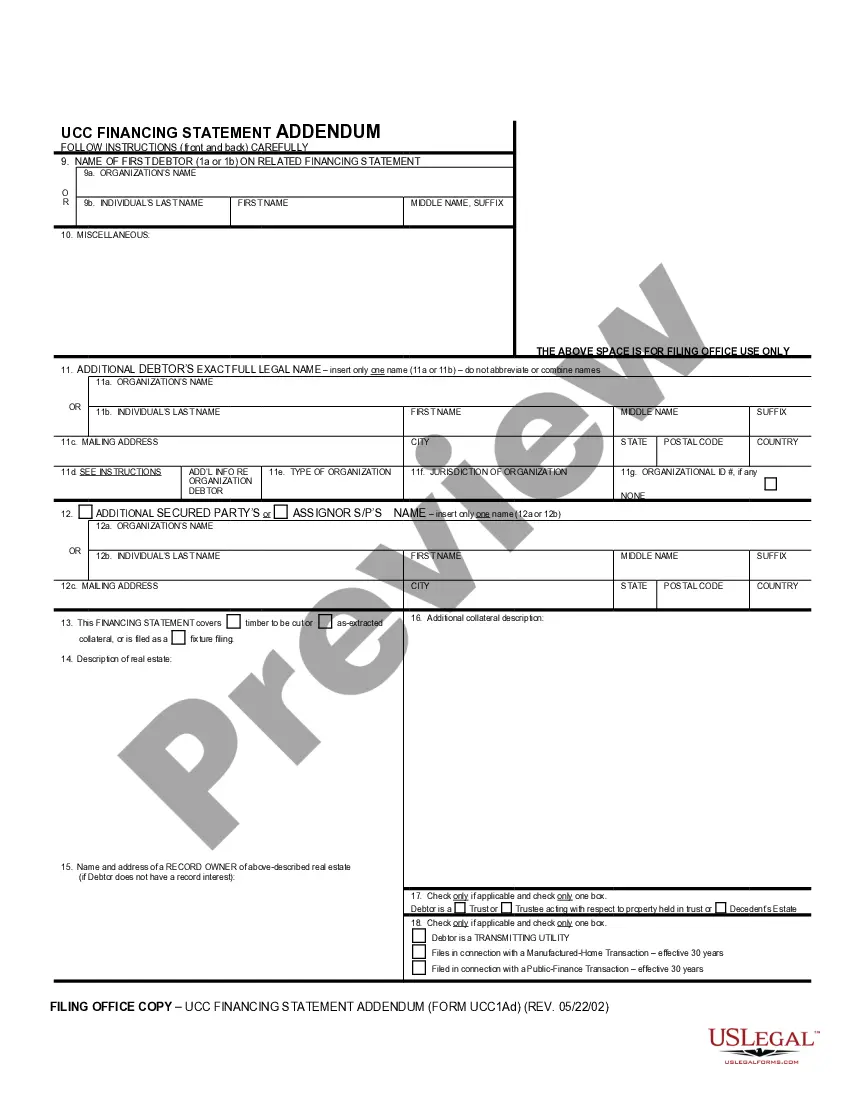

UCC1 - Financing Statement Addendum - Maine - For use after July 1, 2001. This form permits you to add an additional debtor if necessary to cover collateral as specified in the statement.

Maine UCC1 Financing Statement Addendum

State:

Maine

Control #:

ME-UCC1-A

Format:

PDF

Instant download

This website is not affiliated with any governmental entity

Public form

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Maine UCC1 Financing Statement Addendum?

Obtain any version from 85,000 legal documents like the Maine UCC1 Financing Statement Addendum online with US Legal Forms. Each template is crafted and refreshed by attorneys licensed in the state.

If you already have a membership, sign in. When you are on the form's page, press the Download button and navigate to My documents to gain access to it.

If you have not subscribed yet, follow the guidelines listed below.

With US Legal Forms, you will always have instant access to the appropriate downloadable template. The service gives you access to documents and categorizes them to make your search easier. Utilize US Legal Forms to acquire your Maine UCC1 Financing Statement Addendum quickly and effortlessly.

- Review the state-specific criteria for the Maine UCC1 Financing Statement Addendum you intend to utilize.

- Browse through the description and preview the template.

- Once you are certain the sample meets your needs, click Buy Now.

- Choose a subscription plan that fits your budget.

- Set up a personal account.

- Make the payment through either of the two available methods: by credit card or via PayPal.

- Choose a format to download the document in; two options are available (PDF or Word).

- Save the file to the My documents section.

- When your reusable template is prepared, print it or store it on your device.

Form popularity

FAQ

A financing statement is not exactly the same as a UCC; rather, it is a document filed under the Uniform Commercial Code (UCC). The Maine UCC1 Financing Statement Addendum serves to perfect a security interest in personal property. This means the UCC governs how these statements are structured and submitted. Therefore, understanding the relationship between financing statements and the UCC is essential for securing your interests.

A UCC financing statement is generally filed at the Secretary of State's office in the state where the debtor is based. It's important to verify the filing methods available, which may include electronic submissions. Using the Maine UCC1 Financing Statement Addendum can enhance your filing, providing a clear and organized approach to all relevant details. This ensures that your financing statement is both effective and compliant with state laws.

You file a UCC 1 financing statement with the appropriate state office, typically the Secretary of State's office, where the debtor is located or where the collateral is situated. Consult your state's guidelines for the exact filing process. For added clarity on your financing situation, utilize the Maine UCC1 Financing Statement Addendum. This can simplify the filing process by detailing any additional information.

To terminate a UCC financing statement, you need to file a termination statement with the appropriate state authority where the original statement was filed. Ensure that you have completed all forms accurately and provided any requisite fees. By using the Maine UCC1 Financing Statement Addendum, you can clarify what changes led to the termination. This helps maintain clear records.

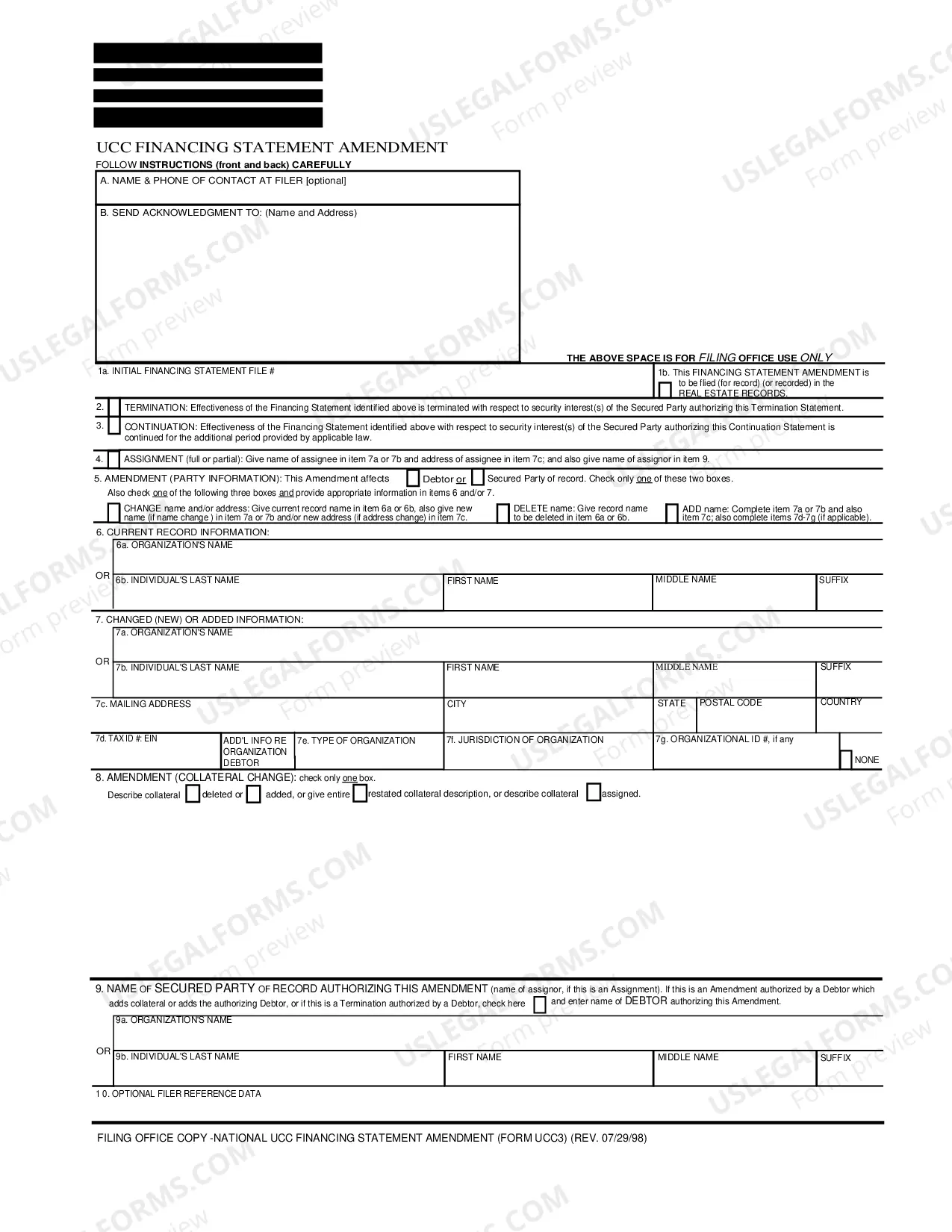

To file a UCC financing statement amendment, first obtain the necessary form from your state’s filing office. Fill in the required sections to capture the changes you want to make. When you modify details related to your financing statement, referencing the Maine UCC1 Financing Statement Addendum can enhance clarity in your documentation. Submit the amendment file promptly to update public records.

It should be noted that UCC financing statements filed now generally do not contain a grant of the security interest and generally are not signed or otherwise authenticated by the Debtor and therefore would not satisfy the requirement of a security agreement.

Rules vary by State around releasing a UCC lien after a borrower satisfied the debt. Primarily there are two main ways to remove them. One way is by having the lender file a UCC-3 Financing Statement Amendment. Another way to remove a UCC filing is by swearing an oath of full payment at the secretary of state office.

The secured party has 20 days to either terminate the filing or send a termination statement to the debtor that the debtor can then file. If this does not happen within the 20-day time frame, the debtor may file a UCC-3 termination statement.

Form UCC3 is used to amend (make changes to) a UCC1 filing.However, it is important to note that for a UCC1 filing a termination is only an amendment and that the UCC1 filing may be amended further, even after a termination has been filed. Box 3 Continuation A UCC1 filing is good for five years.

If you're approved for a small-business loan, a lender might file a UCC financing statement or a UCC-1 filing. This is just a legal form that allows for the lender to announce lien on a secured loan. This allows for the lender to seize, foreclose or even sell the underlying collateral if you fail to repay your loan.