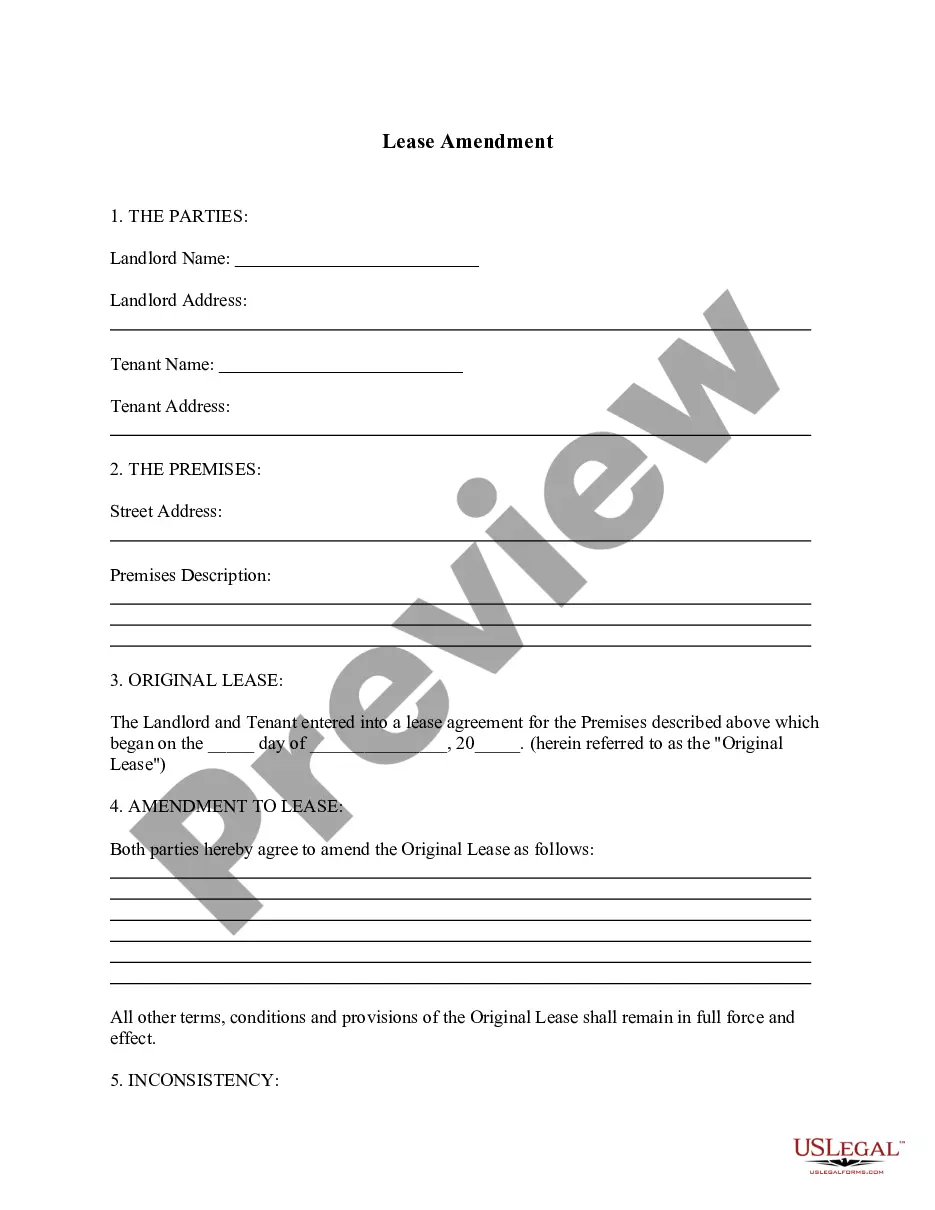

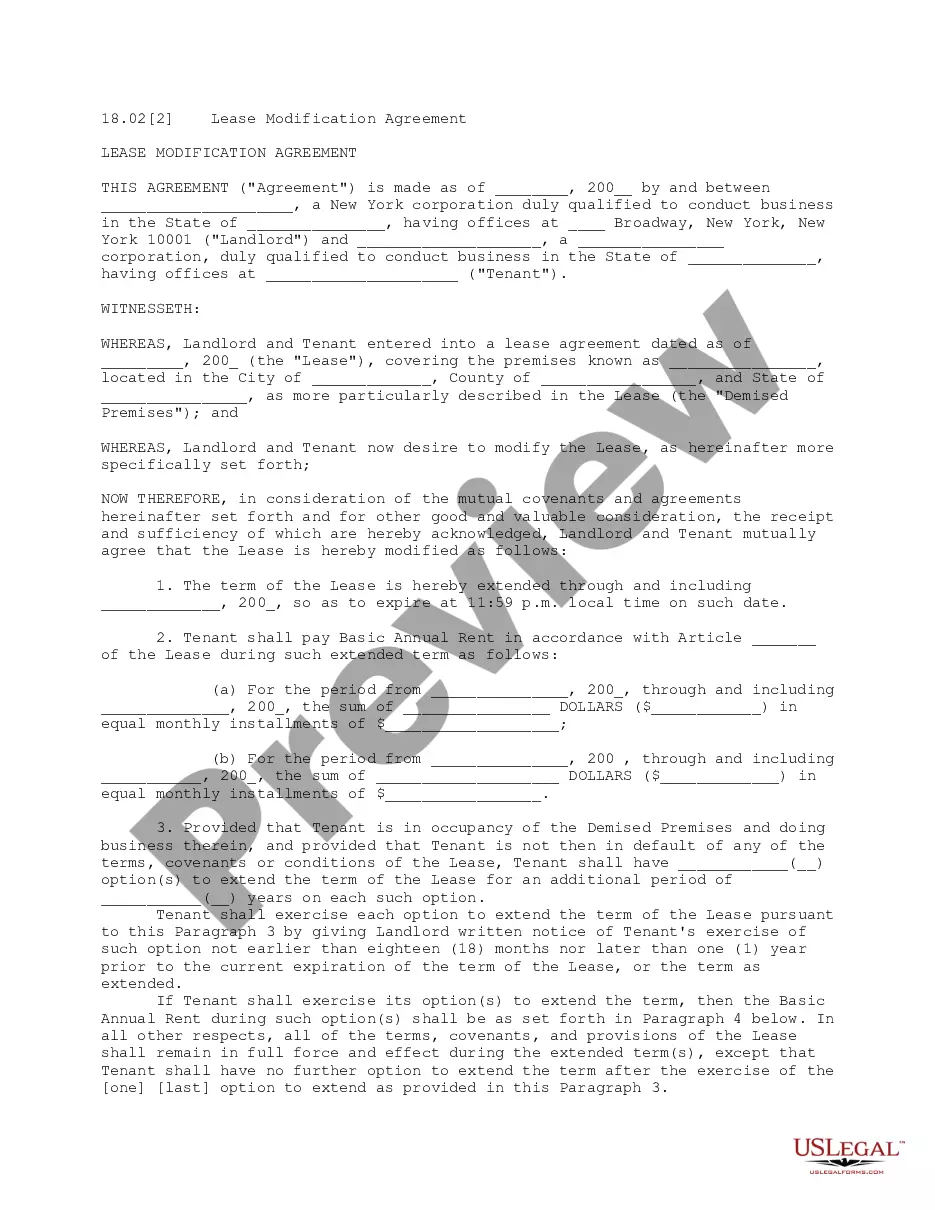

This lease clause states that the landlord and the tenant agree that the lease [sublease] is modified, and illustrates the terms and conditions of the modifications of the lease.

Maine Lease Modification Adding One or More Entities as Tenant Parties

Category:

State:

Multi-State

Control #:

US-OL210110

Format:

Word;

PDF

Instant download

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Lease Modification Adding One Or More Entities As Tenant Parties?

Finding the right legitimate document format can be a have difficulties. Needless to say, there are a variety of web templates accessible on the Internet, but how do you discover the legitimate type you require? Use the US Legal Forms site. The support offers thousands of web templates, like the Maine Lease Modification Adding One or More Entities as Tenant Parties, that can be used for organization and personal requires. All of the varieties are examined by professionals and meet federal and state requirements.

If you are presently authorized, log in to your bank account and then click the Down load switch to get the Maine Lease Modification Adding One or More Entities as Tenant Parties. Utilize your bank account to search through the legitimate varieties you may have purchased formerly. Visit the My Forms tab of your bank account and acquire another duplicate from the document you require.

If you are a whole new consumer of US Legal Forms, here are easy instructions that you should adhere to:

- Initially, ensure you have chosen the proper type for your city/county. You are able to look through the shape making use of the Preview switch and look at the shape information to guarantee this is basically the best for you.

- When the type is not going to meet your expectations, utilize the Seach industry to obtain the correct type.

- When you are sure that the shape is acceptable, go through the Acquire now switch to get the type.

- Pick the rates program you would like and type in the needed details. Design your bank account and buy your order with your PayPal bank account or charge card.

- Pick the data file format and obtain the legitimate document format to your system.

- Full, change and printing and indication the attained Maine Lease Modification Adding One or More Entities as Tenant Parties.

US Legal Forms is definitely the most significant collection of legitimate varieties in which you can discover various document web templates. Use the service to obtain expertly-produced files that adhere to status requirements.

Form popularity

FAQ

Reassessment of the lease after the commencement date is required by a lessee if there is a change in the lease term, or on lessee's assessment of whether it would reasonably be certain to exercise a purchase option.

Ing to the IFRS 16, A re-assessment of the lease liability takes place if the cash flows change based on the original terms and conditions of the lease. Changes that were not part of the original terms and conditions of the lease would be considered as lease modifications.

Common situations where a lease requires reassessment or remeasurement include: The lease terms and conditions change, such as terms being extended. Company leaders reconsider exercising a purchase option. The company determines the amount of a lease incentive that was unknown at adoption.

If a lease is modified and the modification does not result in a separate contract then the lessee will need to subsequently re-measure the lease that was amended. Follow the processes outlined below to subsequently re-measure an operating or finance lease.

The lessee shall remeasure the lease liability to reflect those revised lease payments only when there is a change in the cash flows (ie when the adjustment to the lease payments takes effect).

Ing to the IFRS 16, A re-assessment of the lease liability takes place if the cash flows change based on the original terms and conditions of the lease. Changes that were not part of the original terms and conditions of the lease would be considered as lease modifications.

Account for the lease modification as a termination of the original lease and creation of a new lease from the effective date of the modification. Measure the carrying amount of the underlying asset as the net investment in the original lease immediately before the effective date of the modification.

Lease modification: A change in the scope of a lease, or the consideration for a lease, that was not part of the original terms and conditions of the lease (for example, adding or terminating the right to use one or more underlying assets, or extending or shortening the contractual lease term).