Maine General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion

Description

How to fill out General Form Of Trust Agreement For Minor Qualifying For Annual Gift Tax Exclusion?

Are you in a situation where you require documents for either an organization or individual use almost every day.

There are numerous legal document templates available online, but locating ones you can trust is challenging.

US Legal Forms provides thousands of document templates, such as the Maine General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion, which can be tailored to meet federal and state requirements.

Select a convenient file format and download your copy.

Access all the document templates you have purchased in the My documents section. You can obtain an additional copy of the Maine General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion at any time if necessary. Just select the desired form to download or print the document template.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- Then, you can download the Maine General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion template.

- If you don't have an account and want to start using US Legal Forms, follow these steps.

- Select the form you need and ensure it is for the correct city/state.

- Utilize the Review button to examine the form.

- Check the details to ensure you have chosen the right form.

- If the form is not what you are looking for, use the Search field to find the form that meets your requirements.

- Once you find the correct form, click on Acquire now.

- Choose the pricing plan you prefer, fill out the necessary information to create your account, and complete your purchase using PayPal or a credit card.

Form popularity

FAQ

A gift in trust is a way to avoid taxes on gifts that exceed the annual gift tax exclusion amount. One type of gift in trust is a Crummey trust, which allows gifts to be given for a specific period, establishing the gifts as a present interest and eligible for the gift tax exclusion.

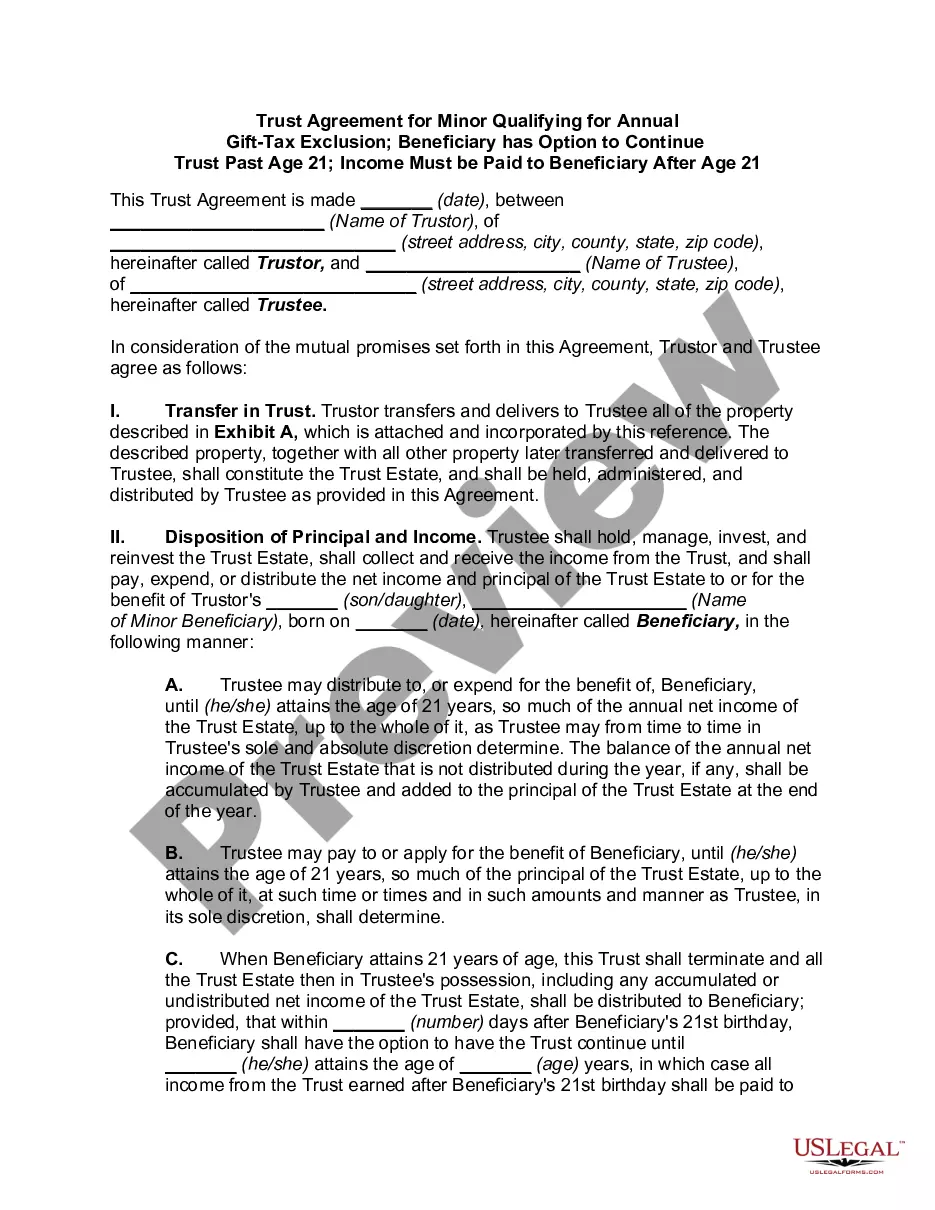

The key difference between a 2503(c) trust and a 2503(b) trust is the distribution requirement. Parents who are concerned about providing a child or other beneficiary with access to trust funds at age 21 might be better off with a 2503(b), since there is no requirement for access at age 21.

A Section 2503(c) trust allows all the principal and income to be used for the child until he reaches the age of 21, unlike the 2503(b) trust that extends beyond age 21 and requires income to be paid to the child annually. The trustee can pay the child's college expenses from the 2503(c) trust.

Section 2503(b) is also known as a Qualifying Minor's Trust or Mandatory Income Trust. This is an irrevocable trust which requires distribution of income on an annual basis. Most often, distributed funds are placed into a custodial bank account until the child reaches legal age.

Gifts in trust do not qualify for the annual exclusion unless the trust either qualifies as a Minor's Trust under Internal Revenue Code Section 2503(c) or has certain temporary withdrawal powers called Crummey powers.

Section 2503(b) is also known as a Qualifying Minor's Trust or Mandatory Income Trust. This is an irrevocable trust which requires distribution of income on an annual basis. Most often, distributed funds are placed into a custodial bank account until the child reaches legal age.

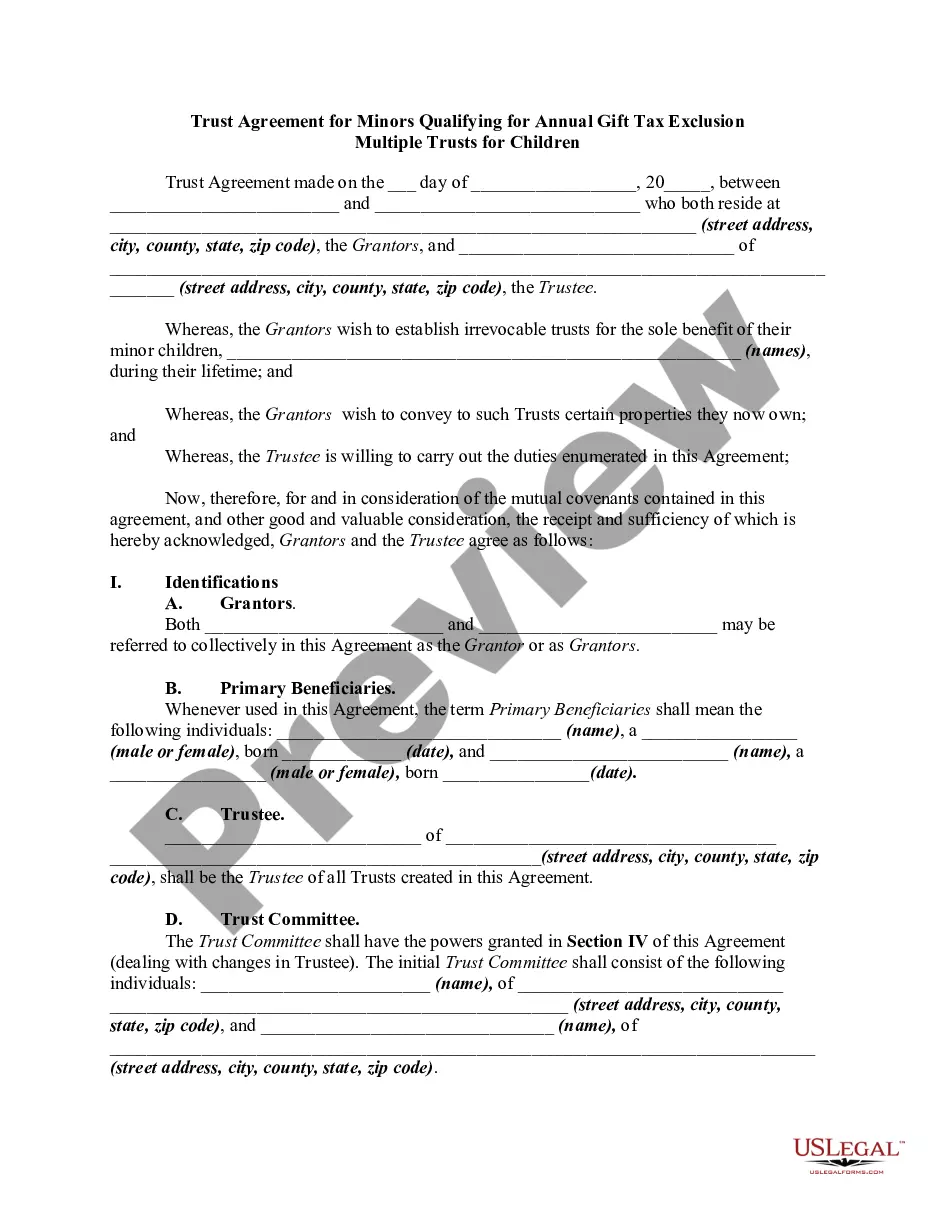

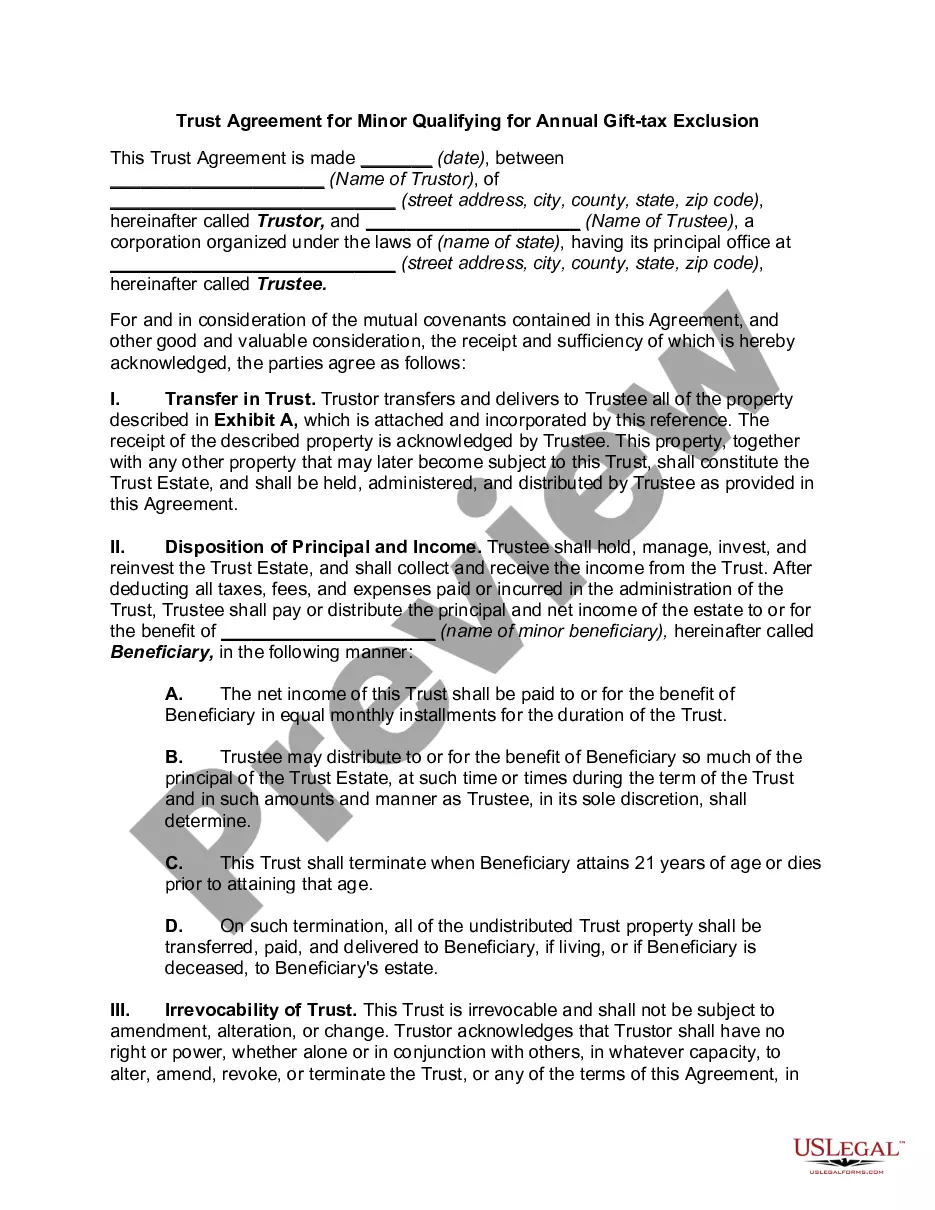

A 2503(c) trust, or minor's trust, is a trust established to hold gifts for one child until he or she attains age 21. A gift to this type of trust qualifies for the annual federal gift tax exclusion.

2503(c) trust has one beneficiary, and the assets in the trust are irrevocably his or hers (i.e., the assets cannot be redirected to another beneficiary); Because the trust is irrevocable, the grantor gives up total control of the assets; The trust income tax rates may penalize those trusts that accumulate income; and.