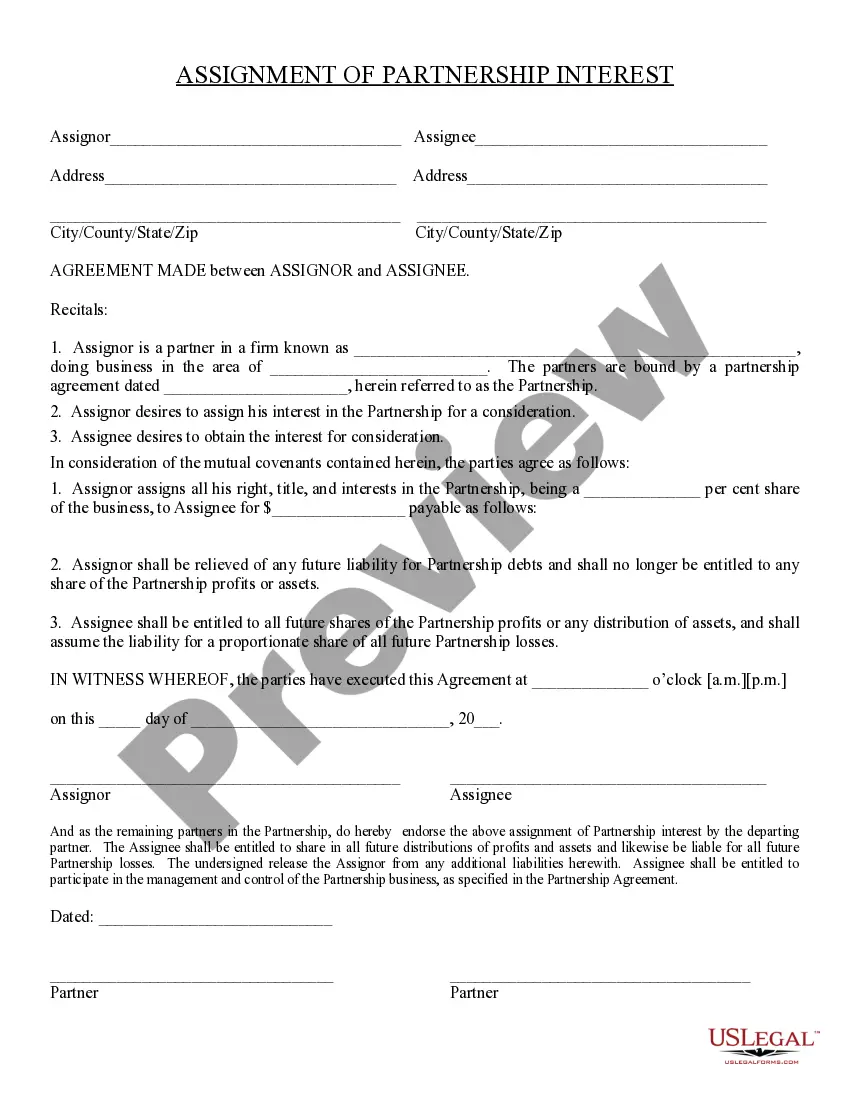

- passing of title;

- made with the intent to pass title;

- without receiving money or value in consideration for the passing of title.

The following form is a gift to a family member of stock in a business owned by the donor.

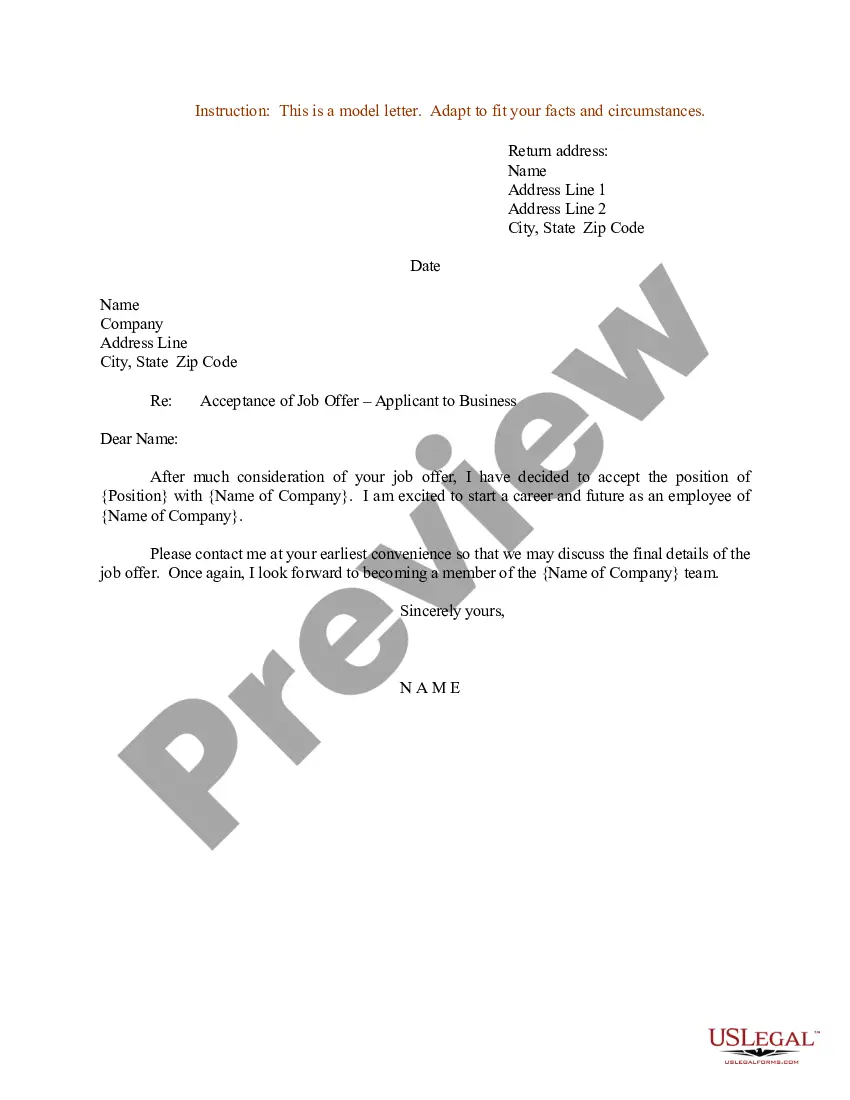

You might devote numerous hours online looking for the legal document template that meets the federal and state criteria you require.

US Legal Forms offers thousands of legal forms that are reviewed by experts.

You can conveniently download or print the Maine Gift of Stock Interest in Business to Family Member from the platform.

If available, use the Preview button to view the document template as well.

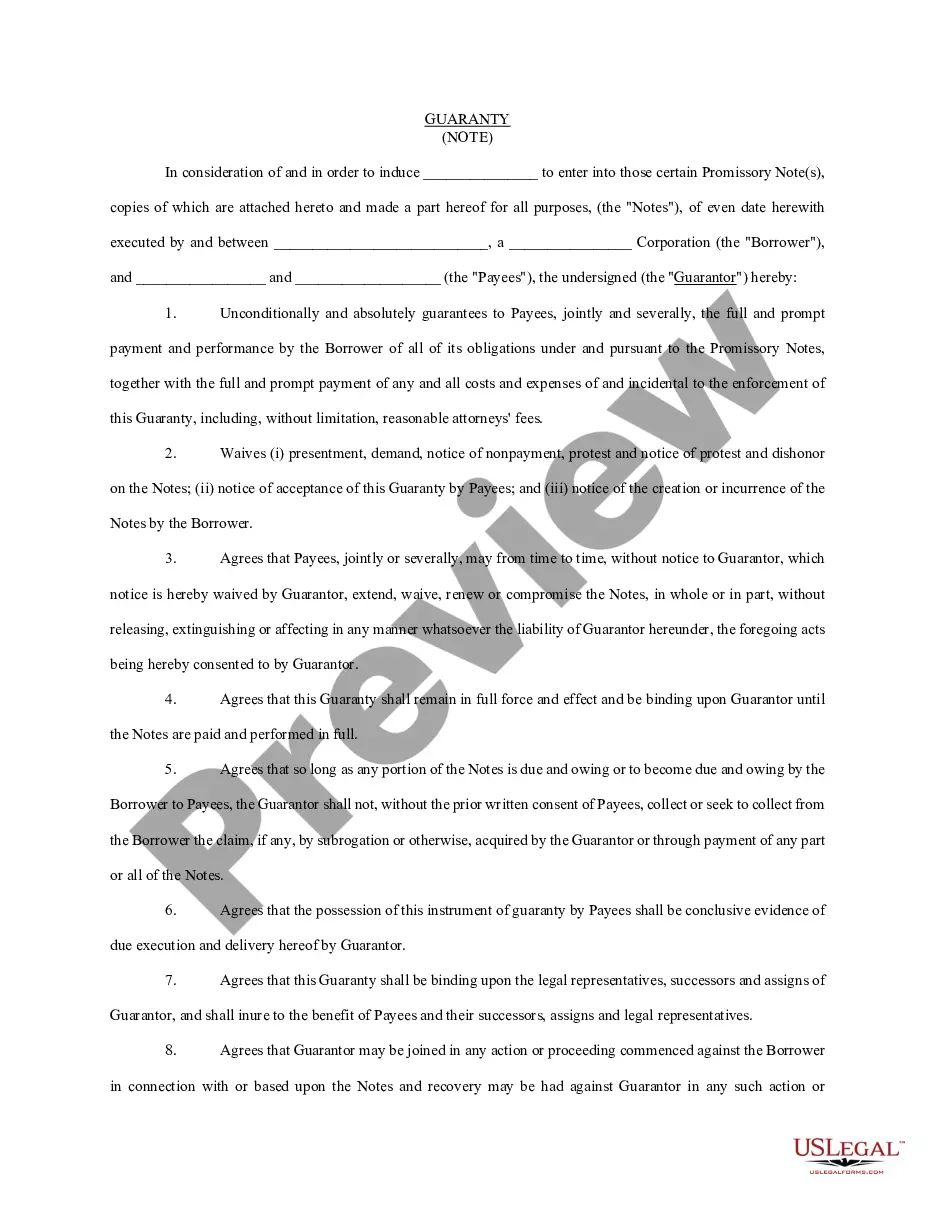

S Corporation Appreciated Gifts A Subchapter S corporation may give appreciated stock or land to charity. Only the basis of the S corporation in the donated asset will be used to reduce the shareholder basis, even though the full fair market value deduction is claimed by the shareholder.

Let's look at the methods of transferring business ownership in detail.Sale of business.Reapportion ownership among multiple owners.Lease-purchase.Transfer via gifts or bequests.Sole proprietorship.Partnerships.LLC.Incorporation.

There are two general ways that an owner can transfer their business's shares to the next generation: gift the shares or sell the shares. Both are treated exactly the same for tax purposes, but their tax outcomes can differ. A gift of shares doesn't require the next generation to pay any funds to acquire the shares.

A gift of an ownership stake in your company is the simplest approach. This could be accomplished with a direct gift or a gift to an irrevocable trust, which would allow you to have more control over the shares after the gift and provide potential liability/divorce protection for the gift recipient.

Transferring Ownership of Stock within an S CorporationFollow the corporation's explicit stock transfer processes.Draft an agreement for the stock transfer.Execute the agreement then attain consideration.Record the transfer in the stock ledger of the corporation.Prepare to consent to an S corporation election.

This article discusses three common options:Sell your business outright. One way to transfer your family business to your children is through selling them your interest in the business, outright.Use a buy-sell agreement.Transfer through a living trust.

How to Transfer Partial Ownership of Your LLCCarefully Follow the Buy-Sell Procedures in Your Operating Agreement or Articles of Organization.Update the Necessary Documents and Notify Relevant Parties.Review your Operating Agreement and Articles of Organization.Establish What Your Buyer Wants to Buy.More items...?

Taking Over the Family Business: The BasicsUse the succession plan.Be patient.Assess your skills.Take care of company culture.Maintain your credibility.Keep the peace.Consider the advice of your peers.

General Rules. Whenever someone purchases shares of stock, that person receives an ownership interest in the particular corporation. In general, there aren't any restrictions to gifting away the stock -- it's treated as the holder's property and the holder is free to do with it as he pleases.

If you're thinking about your legacy, gifting stocks can be a valuable tool, as opposed to liquidating and paying capital gains taxes. The IRS allows you to gift up to $15,000 per year, per person including stock. This $15,000 limit isn't bound by familial or marital ties.