Maryland UCC3 Financing Statement Amendment

About this form

The Maryland UCC3 Financing Statement Amendment is a legal document used to amend a previously filed financing statement under the Uniform Commercial Code (UCC) in Maryland. This form is essential for updating information regarding secured transactions, such as changing a party's name or address, adding a new party, or deleting an existing one. It differs from the initial financing statement as it specifically addresses amendments rather than establishing new financing statements.

Main sections of this form

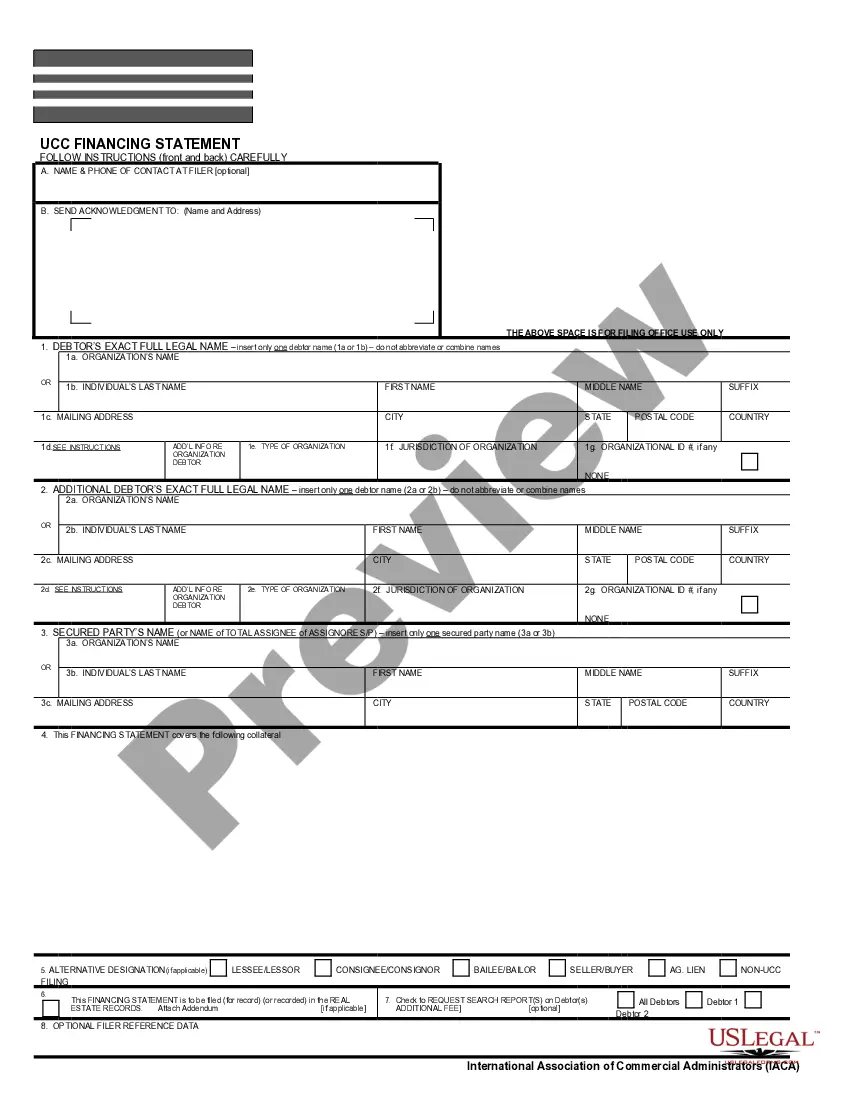

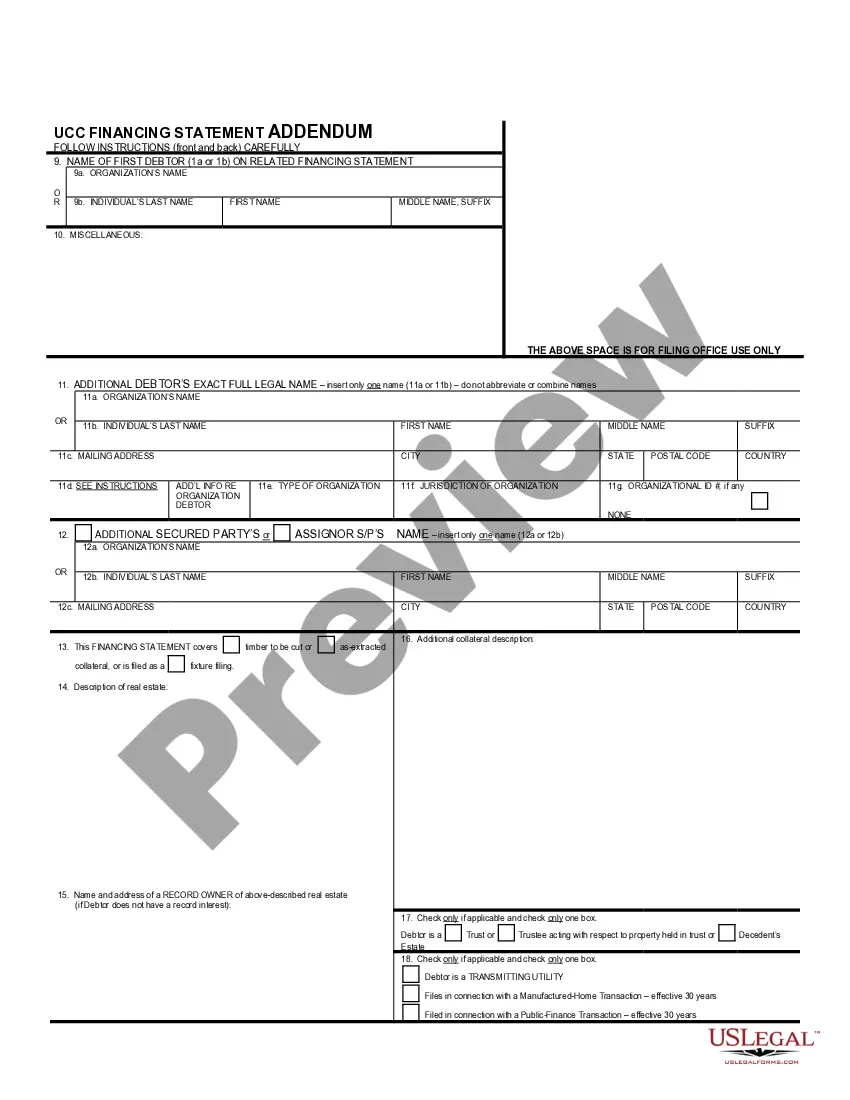

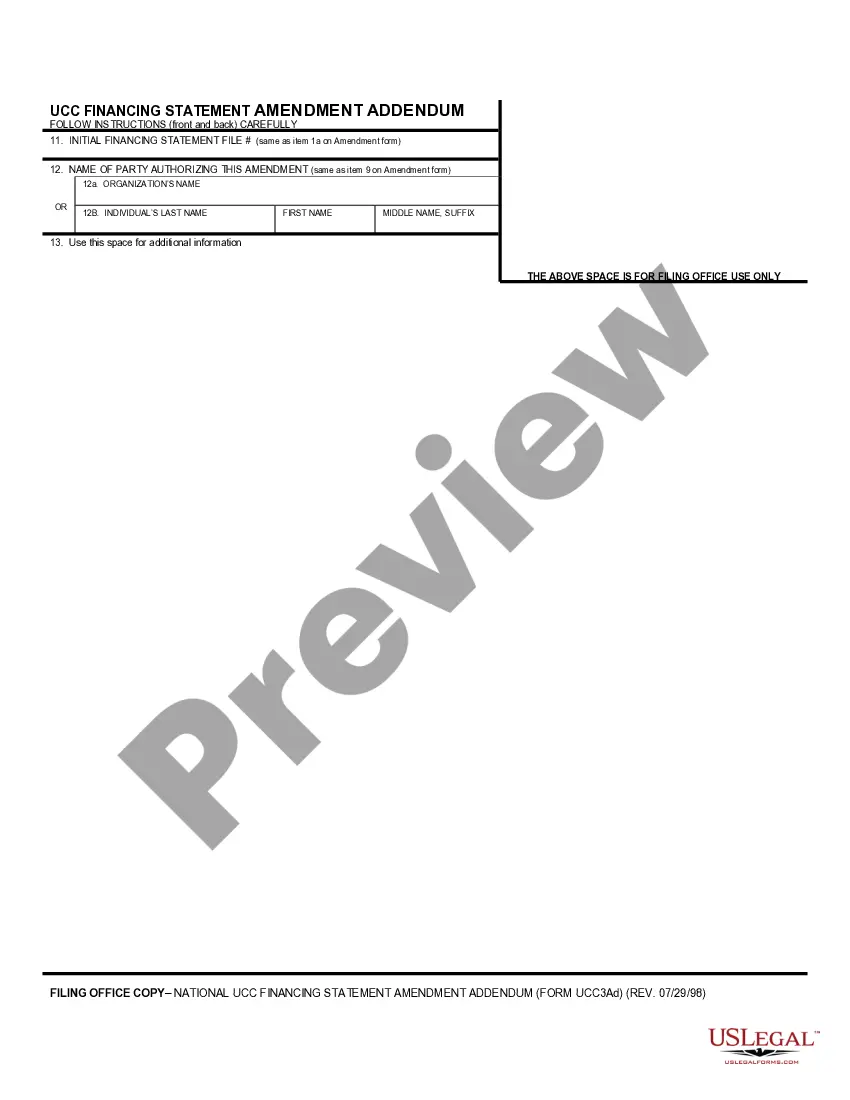

- File number: Required to reference the initial financing statement.

- Purpose checkbox: Indicates the reason for the amendment, such as changing a name or terminating a statement.

- Current record information: Details the existing name or address of the debtor or secured party.

- New information: Sections to provide updated names or addresses for the parties involved.

- Collateral change: Describes any changes to the collateral covered by the financing statement.

- Authorizing party: Identifies the party authorizing the amendment.

Situations where this form applies

This form should be used when there is a need to update or amend details in a previously filed Maryland financing statement. Common scenarios include changing the name or address of the debtor or secured party, adding or deleting parties involved in the secured transaction, or changing the collateral that secures the financing.

Who needs this form

- Debtors: Individuals or organizations whose names or addresses have changed.

- Secured parties: Lenders or creditors needing to update the conditions of a secured transaction.

- Attorneys: Legal professionals representing clients in secured transactions.

- Business owners: Those requiring amendments for business-related financing statements.

Steps to complete this form

- Identify the file number of the initial financing statement you are amending.

- Check the appropriate box to indicate the purpose of the amendment.

- Provide current record information including the name and/or address of the party being amended.

- Enter the new name or address in the designated fields.

- If applicable, describe any changes to the collateral in the prescribed sections.

- Sign and date the amendment to authorize the changes.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, it is advisable to check local regulations to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Incorrectly entering the file number of the initial financing statement.

- Failing to check the correct purpose boxes for the amendment.

- Omitting required signatures from the authorized party.

- Using multiple file numbers on one amendment form.

Why use this form online

- Convenience: Easily complete and submit the form from anywhere.

- Editability: Make corrections or updates in real-time before submission.

- Time-saving: Quick access to the necessary forms without the need to visit a legal office.

Looking for another form?

Form popularity

FAQ

A financing statement is not the same as the UCC. The UCC, or Uniform Commercial Code, is a set of laws governing commercial transactions, while a financing statement is the document used to perfect security interests in collateral. The Maryland UCC3 Financing Statement Amendment is a specific form required to modify an existing statement, ensuring your records are accurate. Understanding the difference helps you manage your legal documents effectively.

Also known as a UCC-3, and, depending on the context, a UCC-3 financing statement amendment, a UCC-3 termination statement, and a UCC-3 continuation statement. Under the Uniform Commercial Code, a UCC-3 is used to continue, assign, terminate, or amend an existing UCC-1 financing statement (UCC-1).

A UCC-1 financing statement (an abbreviation for Uniform Commercial Code-1) is a legal form that a creditor files to give notice that it has or may have an interest in the personal property of a debtor (a person who owes a debt to the creditor as typically specified in the agreement creating the debt).

If you're approved for a small-business loan, a lender might file a UCC financing statement or a UCC-1 filing. This is just a legal form that allows for the lender to announce lien on a secured loan. This allows for the lender to seize, foreclose or even sell the underlying collateral if you fail to repay your loan.

A UCC1 financing statement is effective for a period of five years. A record that is not continued before its lapse date will cease to be effective, costing the secured party their perfected status and perhaps their priority position to collect. Once a financing statement has lapsed, it cannot be revived.

Form UCC3 is used to amend (make changes to) a UCC1 filing.However, it is important to note that for a UCC1 filing a termination is only an amendment and that the UCC1 filing may be amended further, even after a termination has been filed. Box 3 Continuation A UCC1 filing is good for five years.

The secured party has 20 days to either terminate the filing or send a termination statement to the debtor that the debtor can then file. If this does not happen within the 20-day time frame, the debtor may file a UCC-3 termination statement.

Rules vary by State around releasing a UCC lien after a borrower satisfied the debt. Primarily there are two main ways to remove them. One way is by having the lender file a UCC-3 Financing Statement Amendment. Another way to remove a UCC filing is by swearing an oath of full payment at the secretary of state office.

How long does a UCC filing last? A UCC-1 filing is good for five years. After five years, it is considered lapsed and no longer valid.