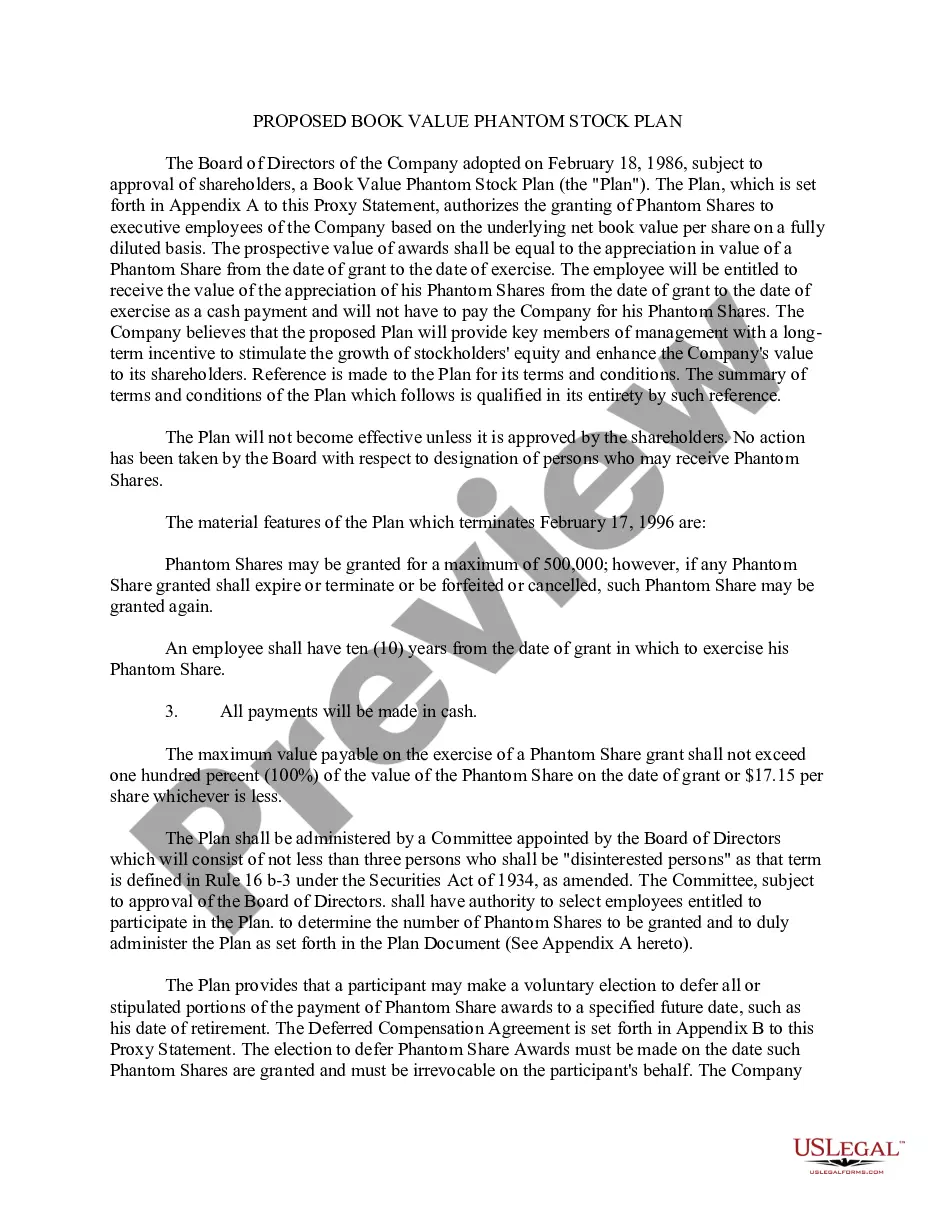

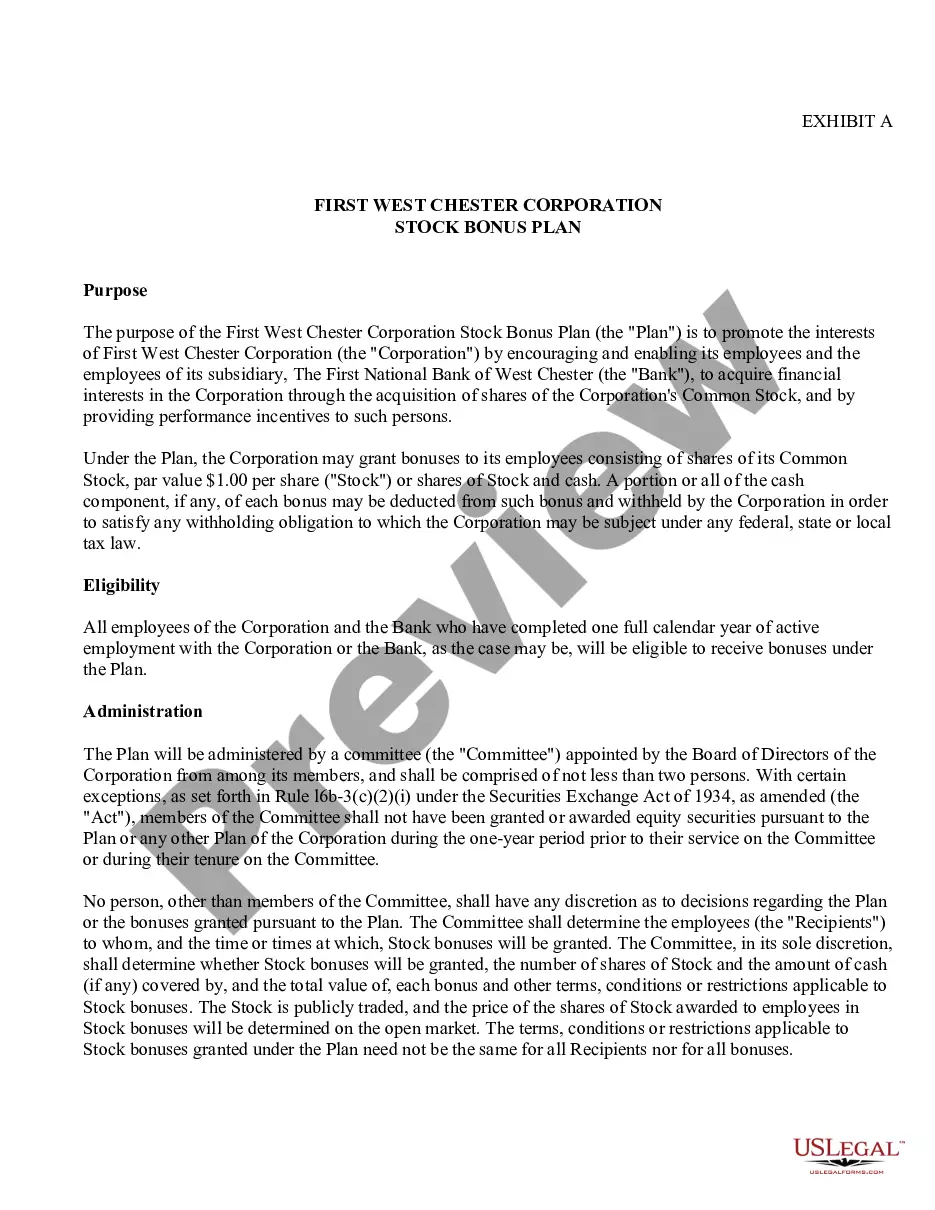

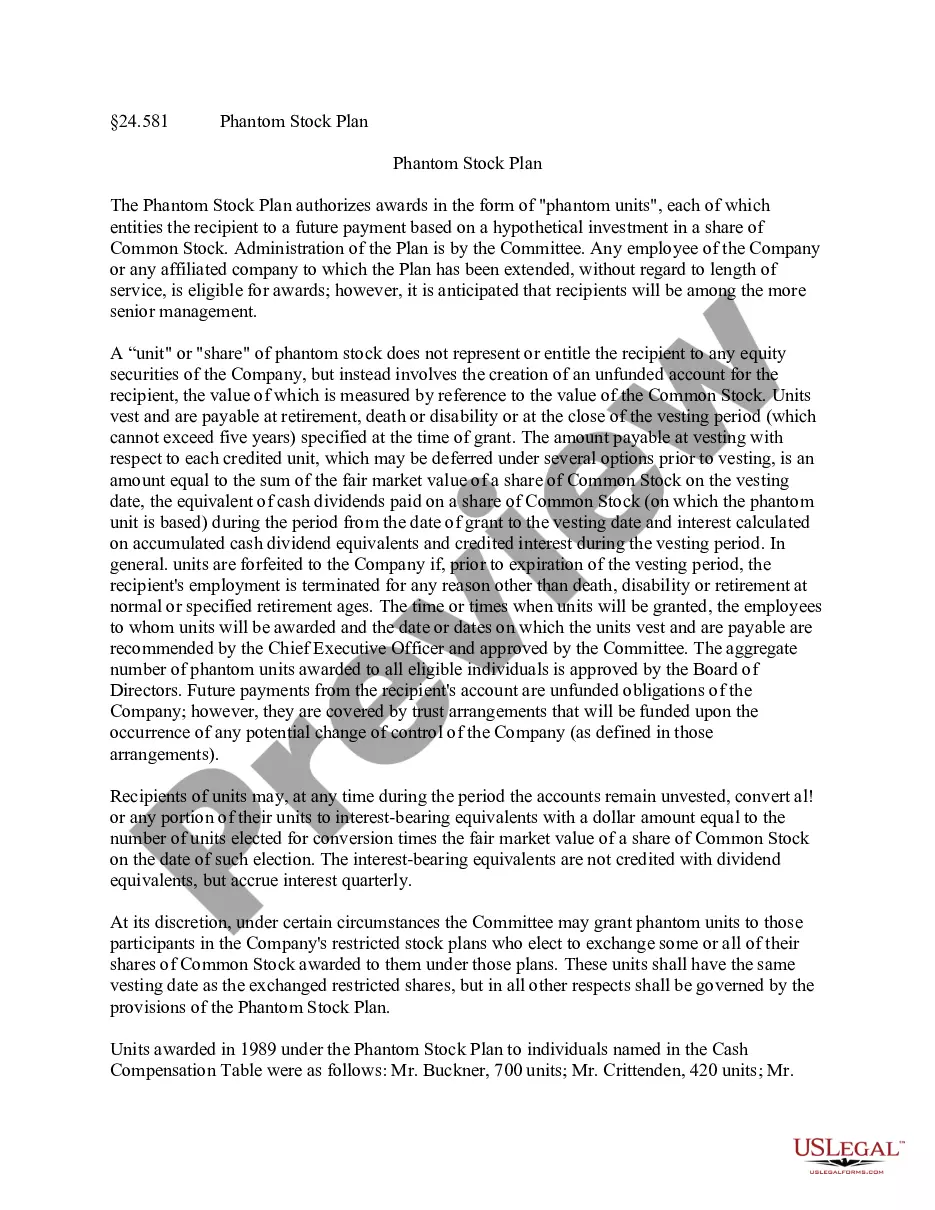

20-162A 20-162A . . . Book Value Phantom Stock Plan under which Committee of Board of Directors may, from time to time, grant quantity of phantom shares to selected employees, each share being equivalent to one share of corporation common stock. Phantom shares may be exercised at any time within ten years of date of grant (subject to certain limitations in event of termination of employment) Upon exercise, employee is paid cash equal to increase in underlying net book value per share on fully diluted basis of shares between date of grant and date of exercise

Maryland Book Value Phantom Stock Plan of First Florida Banks, Inc.

State:

Multi-State

Control #:

US-CC-20-162A

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Book Value Phantom Stock Plan Of First Florida Banks, Inc.?

If you wish to comprehensive, download, or printing lawful document templates, use US Legal Forms, the largest collection of lawful kinds, which can be found on the Internet. Utilize the site`s basic and practical research to get the files you will need. A variety of templates for company and personal functions are sorted by types and states, or keywords. Use US Legal Forms to get the Maryland Book Value Phantom Stock Plan of First Florida Banks, Inc. with a couple of mouse clicks.

Should you be currently a US Legal Forms customer, log in in your profile and click on the Obtain option to have the Maryland Book Value Phantom Stock Plan of First Florida Banks, Inc.. You may also entry kinds you in the past delivered electronically from the My Forms tab of your profile.

If you are using US Legal Forms the first time, refer to the instructions listed below:

- Step 1. Be sure you have chosen the form for that appropriate town/region.

- Step 2. Utilize the Review method to check out the form`s content. Don`t overlook to learn the information.

- Step 3. Should you be unhappy together with the kind, use the Search field at the top of the display to get other types of your lawful kind format.

- Step 4. After you have identified the form you will need, select the Get now option. Choose the prices prepare you favor and add your accreditations to sign up for the profile.

- Step 5. Process the financial transaction. You may use your charge card or PayPal profile to finish the financial transaction.

- Step 6. Select the formatting of your lawful kind and download it in your product.

- Step 7. Comprehensive, edit and printing or indication the Maryland Book Value Phantom Stock Plan of First Florida Banks, Inc..

Each lawful document format you get is your own property forever. You possess acces to each and every kind you delivered electronically inside your acccount. Click on the My Forms area and pick a kind to printing or download again.

Be competitive and download, and printing the Maryland Book Value Phantom Stock Plan of First Florida Banks, Inc. with US Legal Forms. There are thousands of expert and state-specific kinds you may use to your company or personal requirements.

Form popularity

FAQ

The plan may provide for a single payment, or it may provide for installment payments over a period of time after the phantom stock vests. In some cases, the employer may let the employee elect to receive the payout in the form of an equivalent amount of stock.

Phantom stock plans are considered ?liability awards? for accounting purposes (assuming they will be settled in cash rather than stock). As such, the sponsoring company must recognize the plan expense ratably over the vesting period. Varying accrual schedules can be found in the market.

However, phantom stocks come with a considerable amount of disadvantages that can diminish participants' perceived control and influence, strain company liquidity, require extensive administrative efforts, introduce tax complexities, create disagreements, and subject participants to volatility in financial benefits ...

As a default, this form plan provides for forfeiture of all unvested phantom stock units upon a participant's termination of employment (subject to the terms of the award agreement).

The answer involves two variables: (a) the presumed value of the company, and (b) the number of shares to be used in the plan. Once these two answers are known, the phantom share price is calculated as the former (the value) divided by the latter (the number of shares).

Phantom shares are usually paid out when the company gets acquired or IPOes. The phantom shares are paid out in cash for their corresponding value.

It is possible to create a phantom stock plan that avoids the application of 409A rules. The key requirement would be to (a) use cliff vesting (any incremental vesting must trigger immediate payment), and (b) pay benefits within 2½ months of the end of the year in which the awards vest.

Phantom stock plans are considered ?liability awards? for accounting purposes (assuming they will be settled in cash rather than stock).