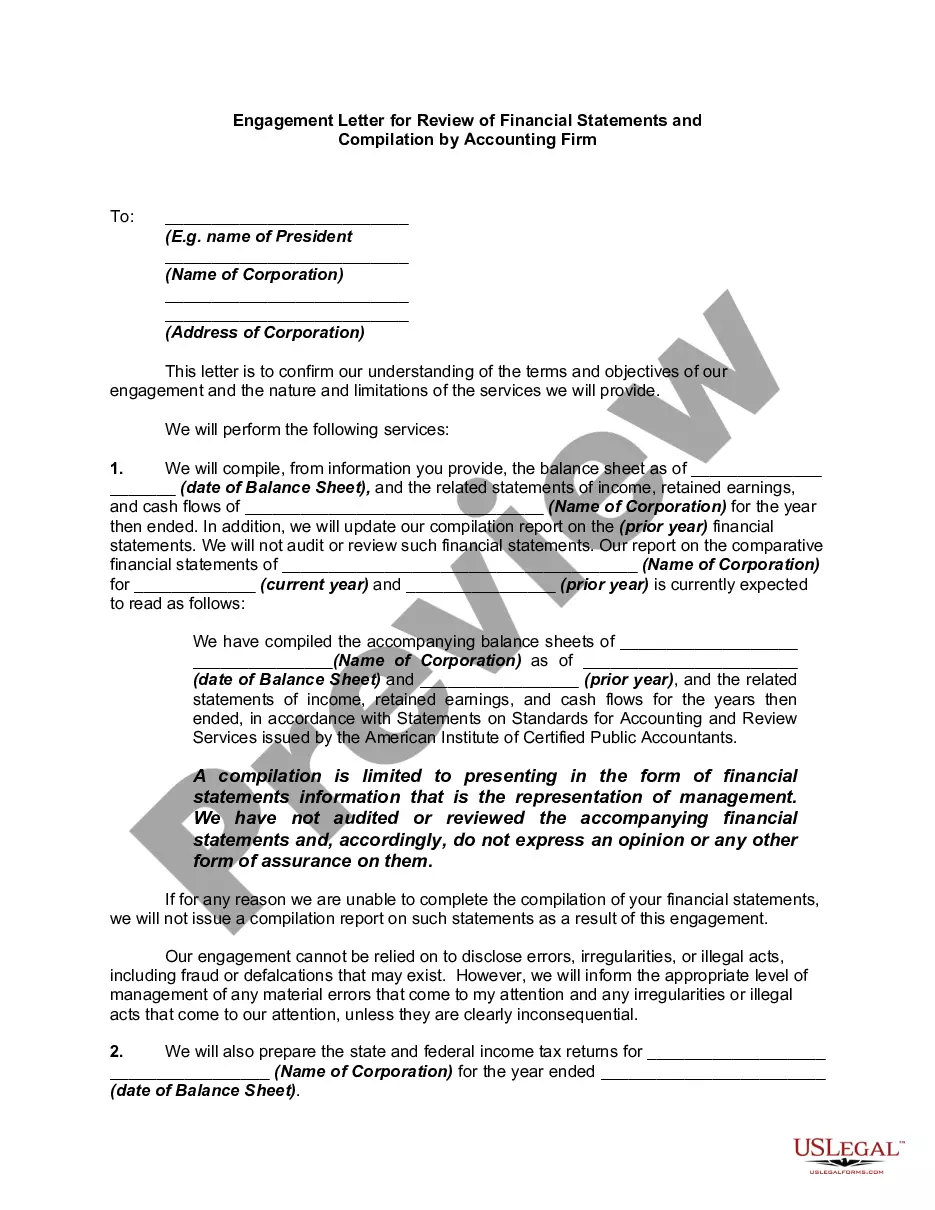

In a compilation engagement, the accountant presents in the form of financial statements information that is the representation of management (owners) without undertaking to express any assurance on the statements. In other words, using management's records, the accountant creates financial statements without gathering evidence or opining about the validity of those underlying records. Because compiled financial statements provide the reader no assurance regarding the statements, they represent the lowest level of financial statement service accountants can provide to their clients. Accordingly, standards governing compilation engagements require that financial statements presented by the accountant to the client or third parties must at least be compiled.

Maryland Report from Review of Financial Statements and Compilation by Accounting Firm

Description

How to fill out Report From Review Of Financial Statements And Compilation By Accounting Firm?

If you want to compile, obtain, or generate official document templates, utilize US Legal Forms, the largest collection of legal forms available online.

Employ the site’s straightforward and user-friendly search to find the documents you require.

A variety of templates for business and personal purposes are organized by categories and states, or keywords. Utilize US Legal Forms to find the Maryland Report from Review of Financial Statements and Compilation by Accounting Firm with just a few clicks.

Every legal document template you acquire is yours permanently. You have access to all forms you downloaded in your account. Go to the My documents section and select a form to print or download again.

Compete and obtain, and print the Maryland Report from Review of Financial Statements and Compilation by Accounting Firm with US Legal Forms. There are thousands of professional and state-specific forms available for your business or personal needs.

- If you are already a US Legal Forms client, Log In to your account and click on the Download button to obtain the Maryland Report from Review of Financial Statements and Compilation by Accounting Firm.

- You can also access forms you have previously downloaded from the My documents section of your account.

- If you are using US Legal Forms for the first time, follow these steps.

- Step 1. Ensure you have chosen the form for your correct region/state.

- Step 2. Use the Preview option to review the content of the form. Don’t forget to read the summary.

- Step 3. If you are not satisfied with the form, use the Search bar at the top of the screen to look for other versions of your legal form template.

- Step 4. Once you’ve located the form you need, click the Purchase now button. Choose your preferred pricing plan and provide your details to register for an account.

- Step 5. Complete the payment. You may use your Visa or Mastercard or PayPal account to finalize the transaction.

- Step 6. Select the format of your legal form and download it onto your device.

- Step 7. Fill out, modify, and print or sign the Maryland Report from Review of Financial Statements and Compilation by Accounting Firm.

Form popularity

FAQ

When an annual report is not filed in Maryland, it leads to several potential consequences, including late fees and administrative penalties. Specifically, your business may be marked as 'not in good standing,' which can hinder future business operations. Moreover, neglecting to file the Maryland Report from Review of Financial Statements and Compilation by Accounting Firm can ultimately result in suspending or dissolving your business entity. Timely filing is key to avoiding these issues.

If an LLC does not file its annual report in Maryland, it can face administrative dissolution by the state. This means that your LLC may lose its legal status, affecting its ability to conduct business. By failing to submit the required Maryland Report from Review of Financial Statements and Compilation by Accounting Firm, you put your business at risk of losing vital rights and privileges. It's critical to stay on top of filing to maintain compliance.

Yes, annual reports are mandatory for all registered business entities in Maryland. This requirement serves to ensure that the state maintains current and accurate records of businesses operating within its jurisdiction. By filing the Maryland Report from Review of Financial Statements and Compilation by Accounting Firm, you can keep your business compliant and avoid issues down the line. Keeping up with this requirement shows that you value transparency and accountability.

Failing to file an Annual Report in Maryland can lead to serious consequences. The state may impose fines and penalties, and your business could face administrative dissolution. Additionally, not filing the Maryland Report from Review of Financial Statements and Compilation by Accounting Firm can affect your ability to operate legally. It's crucial to prioritize timely filings to avoid these repercussions.

To file a Form 1 Annual Report in Maryland, you can complete the form online through the Maryland Department of Assessments and Taxation website. The process is straightforward and user-friendly, allowing you to submit the Maryland Report from Review of Financial Statements and Compilation by Accounting Firm efficiently. It's essential to gather your business information and follow the instructions provided on the platform for a smooth experience.

In Maryland, all business entities including corporations, limited liability companies, and partnerships must file an Annual Report. This requirement ensures that the state has updated information about your business. If you fail to file the Maryland Report from Review of Financial Statements and Compilation by Accounting Firm, penalties may apply. Staying compliant with filing keeps your business in good standing.

A financial review offers a moderate level of assurance by performing analytical procedures and inquiring with management, while a compilation simply presents financial data without any assurance. If you need a proactive approach to understand your financial health, a Maryland Report from Review of Financial Statements and Compilation by Accounting Firm can guide you toward informed decisions while simplifying your financial reporting.

A CPA compilation involves the collection and organization of financial information by a Certified Public Accountant without verification. It summarizes financial statements based on data provided by the business, ensuring the information is presented clearly. If you require a straightforward understanding of your financial data, consider a Maryland Report from Review of Financial Statements and Compilation by Accounting Firm as a practical solution.

A compilation report is a financial statement compilation that presents information in a format suitable for external users. Unlike an audit, it does not provide any assurance about the reliability or integrity of the data. For anyone needing clarity on their financial standing, utilizing a Maryland Report from Review of Financial Statements and Compilation by Accounting Firm can help simplify this process.

A CPA compilation report is a document generated by a Certified Public Accountant after compiling financial statements. This report assembles financial data but does not verify its accuracy or offer assurance. If you need a clear overview, a Maryland Report from Review of Financial Statements and Compilation by Accounting Firm will detail the financial position without the exhaustive process of an audit.