Massachusetts Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself

Description

How to fill out Notice Of Violation Of Fair Debt Act - Creditor Misrepresented Himself?

Have you found yourself in a scenario where you require documents for either business or specific purposes almost all the time.

There are numerous legal document templates available online, but locating versions you can trust is not straightforward.

US Legal Forms offers a vast collection of form templates, such as the Massachusetts Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself, designed to comply with state and federal regulations.

Choose the payment plan you prefer, fill in the required information to create your account, and pay for the transaction using your PayPal or credit card.

Select a convenient file format and download your copy.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- Then, you can download the Massachusetts Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself template.

- If you do not have an account and wish to start using US Legal Forms, follow these instructions.

- Obtain the form you require and ensure it is for the correct city/region.

- Use the Preview button to review the form.

- Check the details to confirm that you have selected the appropriate form.

- If the form is not what you are looking for, use the Lookup field to find the form that fits your requirements.

- Once you find the right form, click Acquire now.

Form popularity

FAQ

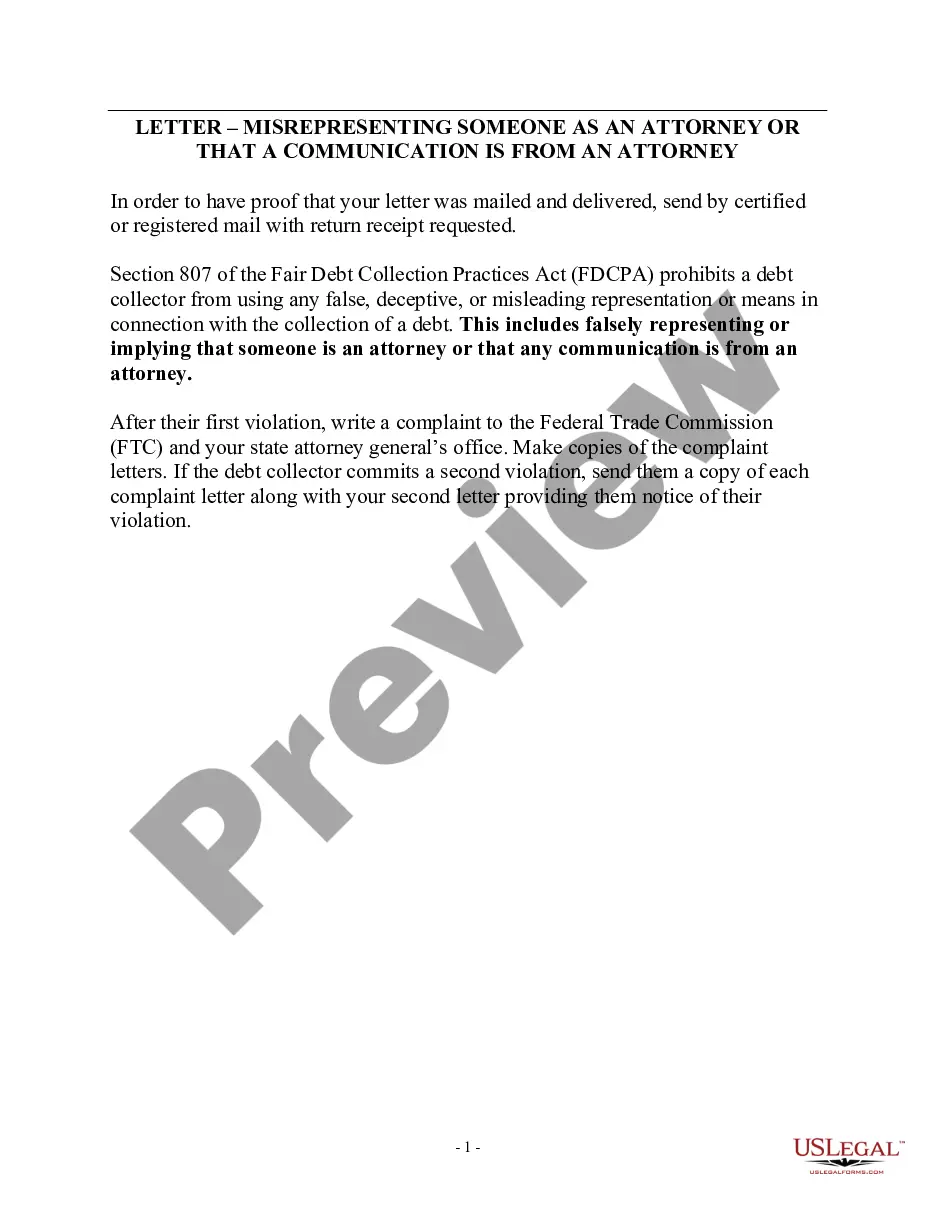

The FDCPA applies only to the collection of debt incurred by a consumer primarily for personal, family, or household purposes. It does not apply to the collection of corporate debt or debt owed for business or agricultural purposes.

The law makes it illegal for debt collectors to harass debtors in other ways, including threats of bodily harm or arrest. They also cannot lie or use profane or obscene language. Additionally, debt collectors cannot threaten to sue a debtor unless they truly intend to take that debtor to court.

They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

The FDCPA defines a "creditor" as the person or entity that extended you the credit in the first place (in other words, your original lender). Because the FDCPA is designed to protect debtors against third-party debt collectors, it doesn't apply to your original creditor or its employees.

Unless your state law provides otherwise, the FDCPA only requires debt collectors, not original creditors, to verify debts in certain circumstances. This requirement includes law firms that are routinely engaged in collecting debts.

The FDCPA defines a "creditor" as the person or entity that extended you the credit in the first place (in other words, your original lender). Because the FDCPA is designed to protect debtors against third-party debt collectors, it doesn't apply to your original creditor or its employees.

Who does regulation F apply to? Regulation F applies to collection agencies, debt collectors, debt buyers, collection law firms, and loan servicers. Creditors collecting on debts they originally owned do not qualify as debt collectors unless they enlist the aid of a debt collector or use a name other than their own.

Massachusetts laws "The statute of limitations for consumer-related debt is six years. This period applies to credit card debt and oral and written contracts. However, if the debt collector has obtained a judgment against the debtor, the statute of limitations extends to 20 years."

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.

The Fair Debt Collection Practices Act (FDCPA) The FDCPA prohibits debt collection companies from using abusive, unfair or deceptive practices to collect debts from you.