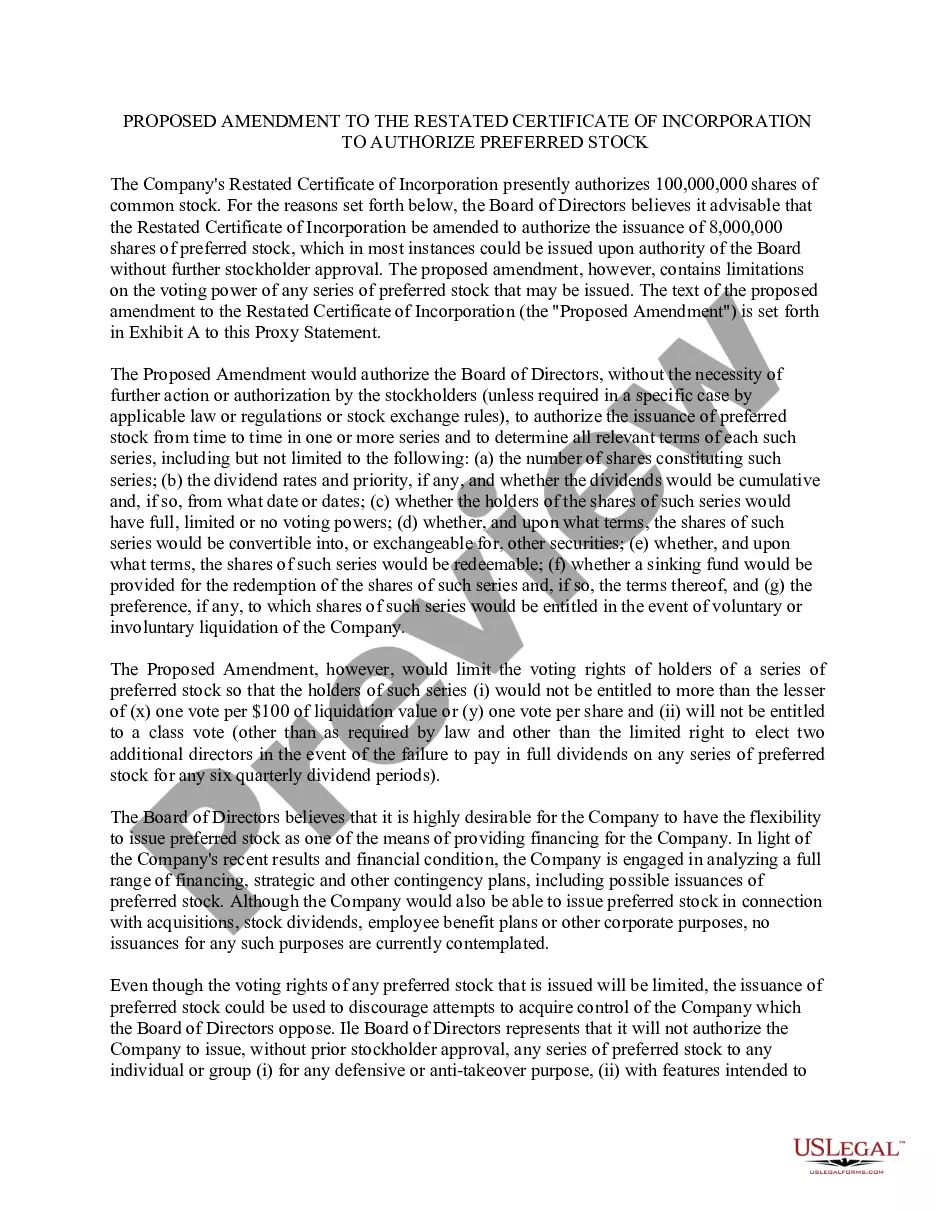

Massachusetts Proposal to decrease authorized common and preferred stock

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Proposal To Decrease Authorized Common And Preferred Stock?

US Legal Forms - among the most significant libraries of lawful types in the States - delivers a wide range of lawful record layouts it is possible to acquire or produce. Using the internet site, you may get a large number of types for business and personal purposes, sorted by types, says, or keywords and phrases.You can get the most recent versions of types just like the Massachusetts Proposal to decrease authorized common and preferred stock in seconds.

If you already have a membership, log in and acquire Massachusetts Proposal to decrease authorized common and preferred stock through the US Legal Forms library. The Download option will appear on every develop you see. You have access to all earlier saved types in the My Forms tab of the bank account.

If you would like use US Legal Forms the first time, allow me to share straightforward recommendations to help you get started:

- Ensure you have selected the right develop to your city/county. Click the Review option to review the form`s content material. See the develop outline to actually have chosen the right develop.

- In case the develop does not satisfy your demands, use the Look for industry towards the top of the display screen to find the one that does.

- When you are pleased with the shape, verify your decision by clicking on the Get now option. Then, pick the costs strategy you prefer and supply your references to register for the bank account.

- Method the transaction. Make use of your bank card or PayPal bank account to perform the transaction.

- Find the formatting and acquire the shape on the gadget.

- Make adjustments. Complete, modify and produce and indication the saved Massachusetts Proposal to decrease authorized common and preferred stock.

Every single web template you put into your account lacks an expiry day and it is your own property eternally. So, if you wish to acquire or produce one more backup, just check out the My Forms portion and then click in the develop you want.

Obtain access to the Massachusetts Proposal to decrease authorized common and preferred stock with US Legal Forms, one of the most considerable library of lawful record layouts. Use a large number of professional and condition-certain layouts that satisfy your business or personal needs and demands.

Form popularity

FAQ

Accounting Principles II If a company has preferred stock, it is listed first in the stockholders' equity section due to its preference in dividends and during liquidation. Book value measures the value of one share of common stock based on amounts used in financial reporting.

Key Steps in Accounting for Equity Issuance Costs under ASC 505-10 Determine the total amount of equity issuance costs. Allocate the equity issuance costs to the related equity accounts. Record the equity issuance costs as a reduction of the related equity accounts.

The journal entry for issuing preferred stock is very similar to the one for common stock. This time Preferred Stock and Paid-in Capital in Excess of Par - Preferred Stock are credited instead of the accounts for common stock.

There two basic ways that issuance fees can be accounted for, namely: As a reduction to paid-in capital. Equity issuance fees may be listed as a reduction of paid-in capital. ... As part of organizational costs. The second way that equity issuance fees can be accounted for is as part of a company's organizational costs.

The cost of preferred stock to a company is effectively the price it pays in return for the income it gets from issuing and selling the stock. In other words, it's the amount of money the company pays out in a year divided by the lump sum they got from issuing the stock.

Upon issuance, common stock is recorded at par value with any amount received above that figure reported in an account such as capital in excess of par value. If issued for an asset or service instead of cash, the recording is based on the fair value of the shares given up.

The issuance of preferred stock is accounted for in the same way as common stock. Par value, though, often serves as the basis for specified dividend payments. Thus, the par value listed for a preferred share frequently approximates fair value.

The main difference between preferred and common stock is that preferred stock gives no voting rights to shareholders while common stock does. Preferred shareholders have priority over a company's income, meaning they are paid dividends before common shareholders.