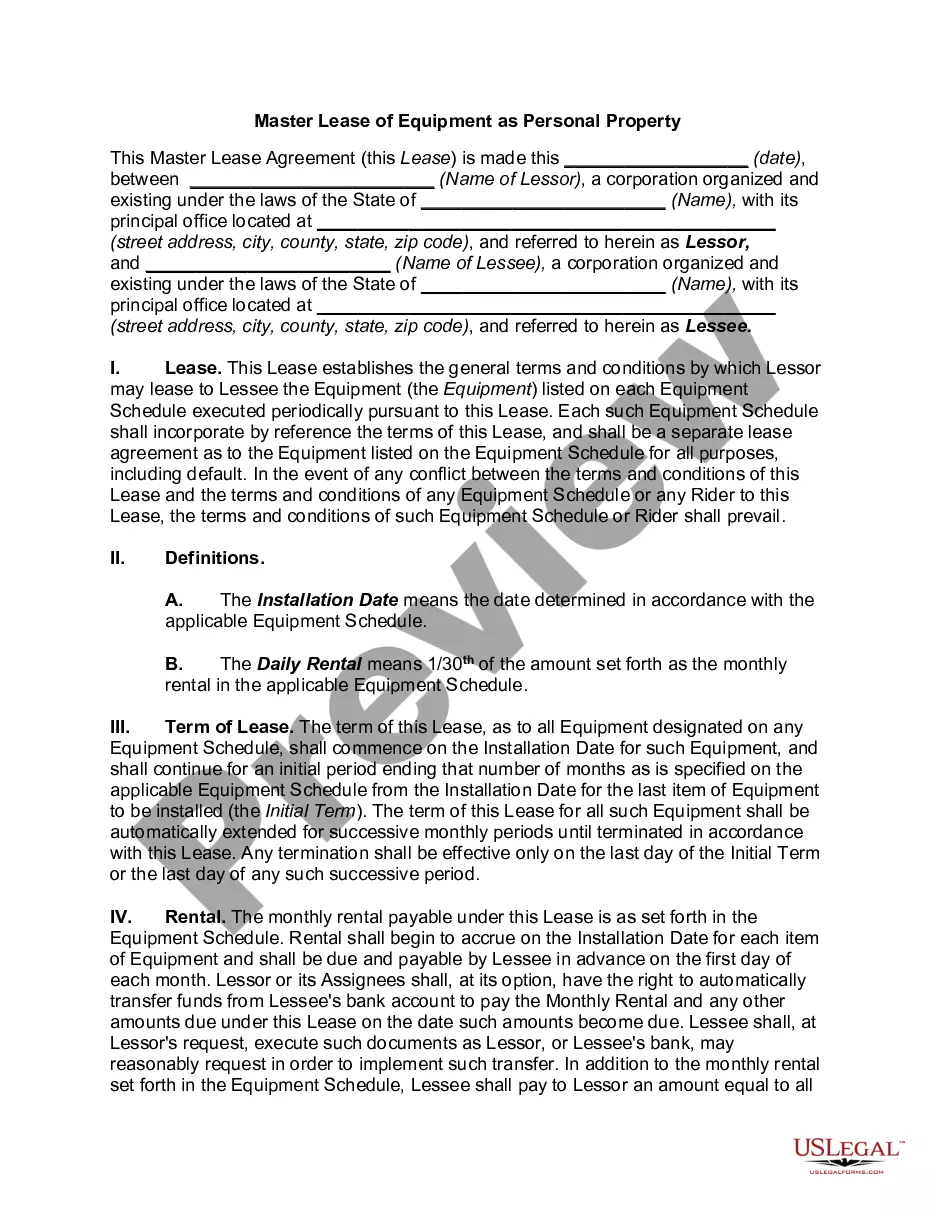

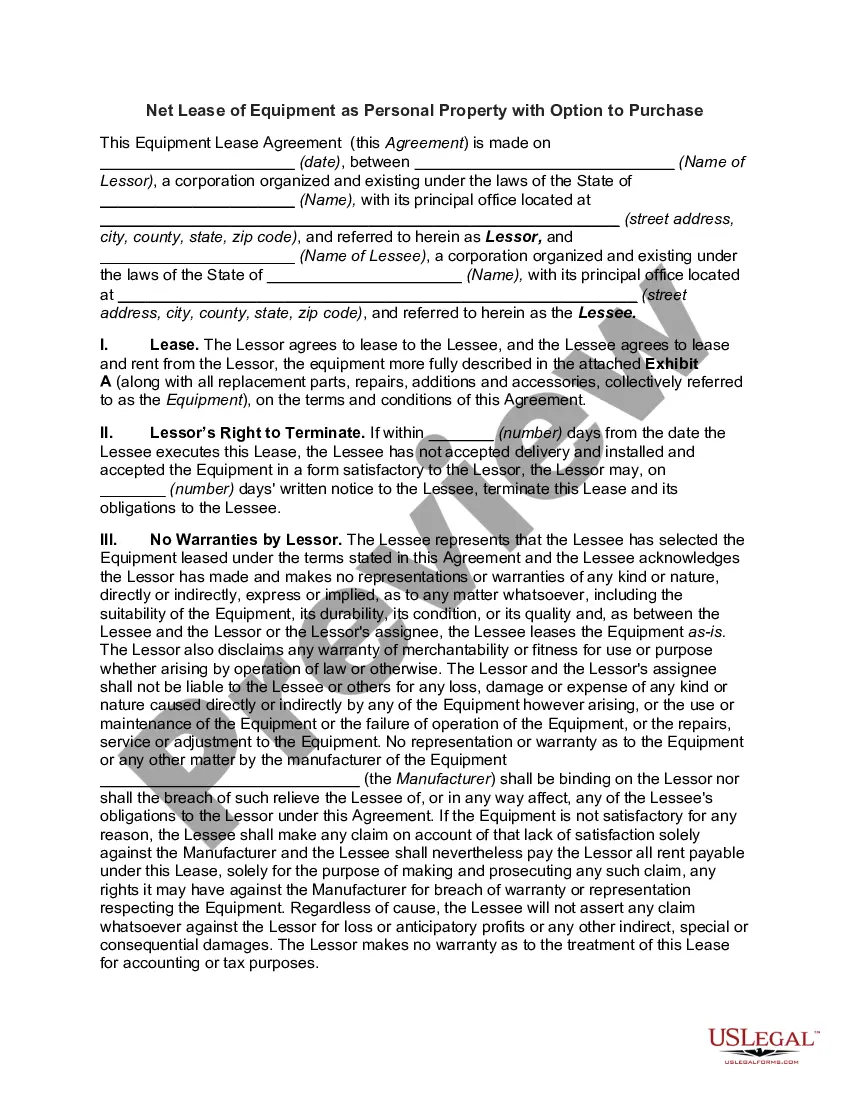

Massachusetts Net Lease of Equipment (personal Propety Net Lease) with no Warranties by Lessor and Option to Purchase

Description

with no Warranties by Lessor and Option to Purchase")

with no Warranties by Lessor and Option to Purchase")

with no Warranties by Lessor and Option to Purchase")

with no Warranties by Lessor and Option to Purchase")

with no Warranties by Lessor and Option to Purchase")

with no Warranties by Lessor and Option to Purchase")

with no Warranties by Lessor and Option to Purchase")

with no Warranties by Lessor and Option to Purchase")

How to fill out Net Lease Of Equipment (personal Propety Net Lease) With No Warranties By Lessor And Option To Purchase?

Have you ever found yourself in a situation where you require documentation for either business or personal activities almost every day.

There are numerous official document templates accessible online, but locating ones you can trust is quite challenging.

US Legal Forms provides a wide array of form templates, including the Massachusetts Net Lease of Equipment (Personal Property Net Lease) without Warranties by Lessor and Option to Purchase, which are designed to comply with federal and state regulations.

Choose a convenient document format and download your copy.

Access all the document templates you have purchased in the My documents list. You can obtain an additional copy of the Massachusetts Net Lease of Equipment (Personal Property Net Lease) without Warranties by Lessor and Option to Purchase anytime by navigating to the needed form to download or print the template.

- If you are already familiar with the US Legal Forms website and possess an account, simply Log In.

- Following that, you can download the Massachusetts Net Lease of Equipment (Personal Property Net Lease) without Warranties by Lessor and Option to Purchase template.

- If you do not have an account and wish to start using US Legal Forms, please follow these steps.

- Locate the form you need and ensure it is for the correct city/county.

- Utilize the Review button to examine the form.

- Review the details to confirm you have selected the correct form.

- If the form is not what you are looking for, use the Search area to find the form that meets your needs.

- Once you find the correct form, click on Get now.

- Select the pricing plan you desire, fill in the required information to create your account, and pay for your order using PayPal or credit card.

Form popularity

FAQ

The 90% lease rule suggests that if a lease term lasts at least 90% of the equipment's useful life, you can consider it a legitimate bundling of finance and leasing. This is particularly relevant to a Massachusetts Net Lease of Equipment (personal Property Net Lease) with no Warranties by Lessor and Option to Purchase. Embracing this rule allows for more favorable accounting treatment and can enhance your business's financial statements, making it an ideal consideration in your leasing strategy.

The formula for leasing can be viewed as a simple equation: total lease payment equals depreciation costs plus interest costs. For a Massachusetts Net Lease of Equipment (personal Property Net Lease) with no Warranties by Lessor and Option to Purchase, you would calculate both depreciation based on the asset's life and interest based on the lease's total value. Knowing this formula can help you determine overall lease affordability and schedule your budgeting more effectively.

The two main types of leases are operating leases and finance leases. In the context of a Massachusetts Net Lease of Equipment (personal Property Net Lease) with no Warranties by Lessor and Option to Purchase, a finance lease often provides more favorable terms for acquiring equipment over time. Conversely, operating leases typically offer lower monthly payments and are used for short-term needs. Understanding the differences helps you choose the right leasing option for your business.

Exiting an equipment lease agreement can be tricky. Typically, with a Massachusetts Net Lease of Equipment (personal Property Net Lease) with no Warranties by Lessor and Option to Purchase, you would need to negotiate with the lessor for an early termination option. You might also consider transferring the lease to another party or buying out the lease if the terms allow. Always thoroughly review your lease agreement to explore the possible exit strategies that best suit your situation.

The 90% rule in leasing pertains to how the economic life of leased equipment is assessed. For a Massachusetts Net Lease of Equipment (personal Property Net Lease) with no Warranties by Lessor and Option to Purchase, this rule states that the lease term should cover at least 90% of the asset's useful life. By adhering to this rule, you ensure that the lease is financially productive and aligns with your business goals, making it a wise choice for long-term planning.

The rule of 78 relates to the method of calculating interest in loans and has implications for a Massachusetts Net Lease of Equipment (personal Property Net Lease) with no Warranties by Lessor and Option to Purchase. This rule favors the lender by allowing them to receive more interest upfront. As such, if you terminate a lease early, early payments will not cover the total interest, leading to potential financial loss. Understanding this rule can help you make informed leasing decisions.

When considering a Massachusetts Net Lease of Equipment (personal Property Net Lease) with no Warranties by Lessor and Option to Purchase, you should be aware of the five key rules. First, the lease must cover the equipment's entire economic life. Second, ownership must transfer to the lessee at the end of the lease term. Third, the lease payments should approximate the equipment's fair market value. Fourth, the lease must not be cancellable, and finally, the lessee must have a strong incentive to purchase the asset at the end of the lease.